Download

1 / 13

130 likes | 446 Vues

Chapter 6 Moving from Day Books through the Ledgers to the Trial Balance. The Subsidiary Ledgers and the General Ledger. Every transaction must end up in the ledgers There are three we will focus on: Sales ledger Purchases ledger General ledger . Sales Ledger .

E N D

Chapter 6Moving from Day Books through the Ledgers to the Trial Balance

The Subsidiary Ledgers and the General Ledger Every transaction must end up in the ledgers There are three we will focus on: • Sales ledger • Purchases ledger • General ledger

Sales Ledger This contains the "T" accounts of all the credit customers. Each "T" account here will tell the firm the exact amount due from each credit customer.

Sales Ledger Look at the sales ledger accounts shown on the next slide so you can determine how much each customer owes

Sales Ledger You should have determined the amounts owed by each debtor as: • Customer C $ 10,000 • Customer D $ 12,000

Purchases Ledger This contains all the "T" accounts of all the credit suppliers. Each "T" account here will give the firm the exact amount payable to each supplier

Subsidiary ledgers The sales ledger and the purchases ledger are examples of subsidiary ledgers. Other examples of subsidiary ledgers are a fixed asset ledger and a payroll ledger. The purpose of subsidiary ledgers is to reduce the amount of detail found in the general ledger.

The General Ledger This contains real accounts (assets, liabilities, and capital) and nominal accounts (revenue and expenses). Real accounts are maintained over several accounting periods, but nominal accounts are closed each period. There will be no personal "T" accounts for customers or suppliers in the general ledger.

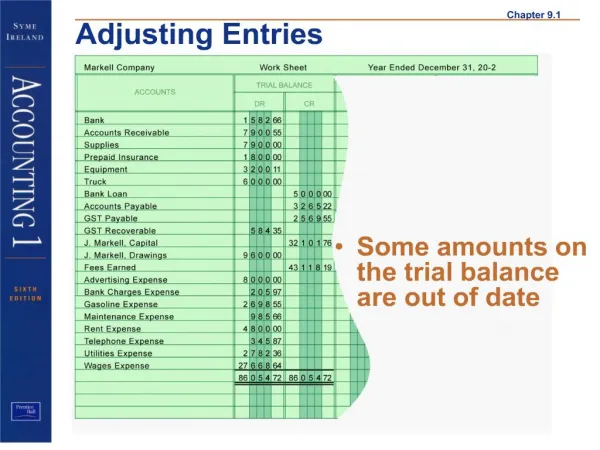

The Trial Balance The trial balance is a listing of all the general ledger account balances at a particular date. Its main purpose is to ensure that all the debit and credit entries we made in the ledgers are the same. Remember that every time we put a debit entry in an account, we also put a credit entry, of an equal amount, into another account.