Download

1 / 9

90 likes | 250 Vues

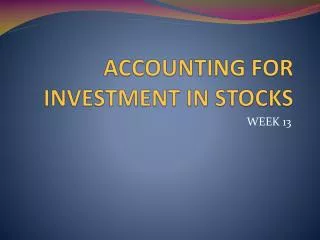

ACCOUNTING FOR INVESTMENT IN STOCKS. WEEK 13. Long-Term Stock Investments. Ownership %. 100%. Controlling Interest. Equity Method. 50%. Significant influence. 20%. Cost Method. Not significant influence. 0%. Long-Term Stock Investments. Ownership %. 100%.

E N D

Long-Term Stock Investments Ownership % 100% Controlling Interest Equity Method 50% Significant influence 20% Cost Method Not significant influence 0%

Long-Term Stock Investments Ownership % 100% Controlling Interest With less than 20% ownership the buyer does not usually have significant influence. The buyer uses the cost method to account for the investment. Equity Method 50% Significant influence 20% Cost Method Not significant influence 0%

Long-Term Stock Investments Ownership % 100% Ownership over 20% usually indicates significant influence. The buyer uses the equity method to account for the investment. Controlling Interest Equity Method 50% Significant influence 20% Cost Method Not significant influence 0%

Long-Term Stock Investments Ownership % 100% Controlling Interest Equity Method 50% The corporation owning all or a majority of the voting stock is called the parent company. The controlled corporation is the subsidiary company. Consolidated financial statements are prepared which combinine the operating results of the two entities. Significant influence 20% Cost Method Not significant influence 0%

Long-Term Stock Investments Ownership % 100% Controlling Interest Equity Method 50% Significant influence 20% Cost Method Not significant influence 0%

Cost Method The cost methodis used when the buyer does not have significant influence over the operating and financing activities of the investee. Investment in Stock 5,940 Cash 5,940 Cash 200 Dividend Revenue 200 Date Description Debit Credit Mar. 1 Purchased 100 shares of Compton Corp. stock at 59 plus brokerage fee of $40. Dec. 31 Received $2 cash dividend from Compton Corp.

Equity Method Date Description Debit Credit Jan. 2 Investment in Brock Corp. Stock 350,000 Cash 350,000 Investment in Brock Corp. Stock 42,000 Income of Brock Corp. 42,000 Cash 18,000 Investment in Brock Corp. Stock 18,000 Purchased 40% of Brock Corporation for $350,000. Dec. 31 Brock Corporation reports net income of $105,000. Dec. 31 Brock Corporation reports total dividends of $45,000.

Sale of Long-Term Stock Investment When shares of stock are sold, the investment account is credited for the carrying value (book value) of the shares sold. Cash 17,500 Investment in Stock 15,700 Gain on Sale of Investments 1,800 Date Description Debit Credit Mar. 1 Sold stock of Drey Inc. for $17,500. Stock has a carrying value of $15,700.