Download

1 / 17

180 likes | 404 Vues

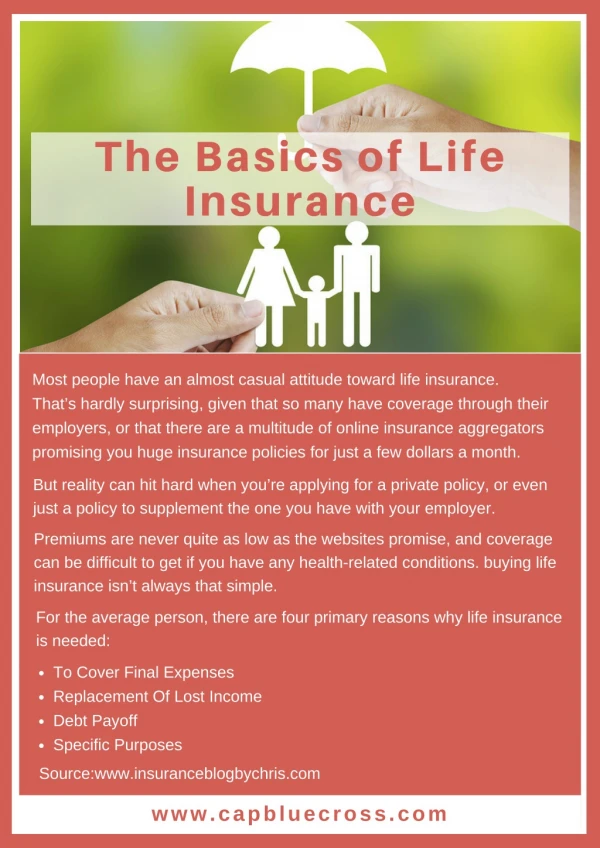

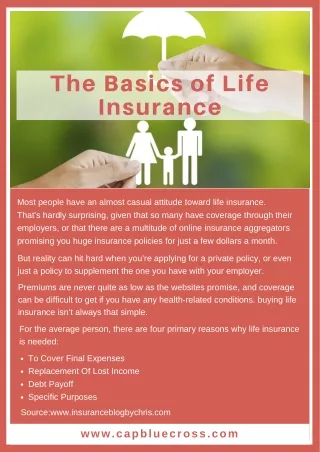

Basics of Health Insurance. The Purpose:. To help offset the cost of medical care Protection against financial losses resulting from illness or injury Covers services and procedures that are considered medically necessary Covers preventive care. DOES NOT COVER. Elective Procedures such as:

E N D

The Purpose: • To help offset the cost of medical care • Protection against financial losses resulting from illness or injury • Covers services and procedures that are considered medically necessary • Covers preventive care

DOES NOT COVER • Elective Procedures such as: • Breast Augmentation • Abdominoplasty • Blepharoplasty • Rhinoplasty • Botox • Other elective, non-medically necessary procedures

Different types of Insurance • Health Insurance for sickness or injury • Coverage for accidents • Disability • Hospitalization • Accidental death • Dismemberment

Here’s the lowdown- • The insuredis also known as the policy- holder • Can be an individual, group or employer • A set amount is paid monthly to the Insurance company, this is called a premium • The insured receives benefits, (payments for medical coverage) and is known as the beneficiary • A dependent is the spouse or child of the insured who is covered under the policy

And More… • Or to obtain an Authorization for an upcoming medical procedure • The Medical Assistant may need to call the Patient’s Insurance Compnay to verify the Eligibility of the patient’s coverage

Insurance Companies • This is called a • -Deductible • Many plans now require a co-payment from the patient at the time of their appointment. $10-$25.00 • A carrier is the Insurance Company who “carries” the coverage • According to the policy the patient pays a portion of the amount owed-

Government Plans • MEDICARE part B • Is for patients 65 and over. • Military dependents are covered by TRICARE • CHAMPVA is coverage for surviving spouses, children • Many large groups of people are covered by government plans.

Other: • Medical Savings Accounts (MSA’s) • A type of self insurance where the insured can buy health insurance and make tax free deposits to an MSA • MEDICAID is coverage for individuals who cannot pay for medical coverage themselves • Estab. 1965

Types of Plan Benefits • Hospitalization • Basic/Major Medical Vision • Dental • Long term care • -Covers all or part of the room, medicines, care, surgery, etc., -Inpatient/Outpatient Radiology, laboratory,

Disability- weekly or monthly cash payments are provided to employee/policy holders who become unable to work as a result of accident or illness • Long term care- chronically ill, disabled or mentally ill Disability Insurance

Who decides how much to pay? • Usual • Customary • Reasonable • Some Insurance companies agree to pay on the basis of all or a part of the physician’s UCR fee.

Managed Care • Managed care is an umbrella term for all healthcare plans that provide healthcare in return for preset, scheduled payments, • To coordinate healthcare through a group of physicians & hospitals

HMO’s • Advantages: • 1. costs are contained • 2. fees are set • 3. covers most preventive care • 4. less out of pocket for patients • Health • Maintenance • Organization- • Provide comprehensive healthcare to an enrolled group for a fixed periodic payment

HMO’s • All healthcare may be managed at one facility • Disadvantages: • 1. Medical care access is limited • 2. choice of physician is limited • 3. more paperwork • 4. Pre-Auth required

Other types of companies… • EPO • Exclusive Provider • Organization • “Exclusive” because employers agree to one plan • PPO • Preferred • Provider • Organization • “Preferred” because it is based on fee for service, with preferred physicians • Co-pay/80-20% EPO PPO

Insurance Companies • Blue Cross/Blue Shield • Cigna • Aetna • Kaiser Permanente • Humana • United Healthcare • Coventry • Assurant • Medicare • Medicaid • Tricare • ChampVa Private plans Government plans