Download

1 / 9

90 likes | 115 Vues

This paper explores liquidity provision and use in electronic markets through a laboratory environment, shedding light on informed trading strategies, liquidity traders, and measuring liquidity. Major results include the role of informed traders, impact on trading volatility, and liquidity trader behaviors.

E N D

The Make or Take Decision in an Electronic Market Discussion: Jaime F. Zender 2003 MTS Conference on Financial Markets

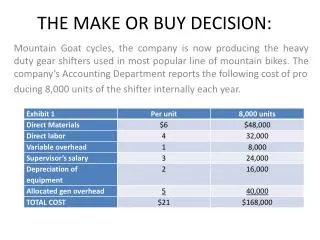

The Basics • A big issue in microstructure is that the models one would build to examine certain issues are intractable. • The approach taken in this paper is instead to use a laboratory environment to examine the provision and use of liquidity in an electronic market. • The strength of this approach is that there is no model to solve. • Its biggest problem is that no model is solved. • “Levels” don’t tell us much. • “Changes” or comparative static exercise give useful intuitions.

Major Results • Informed trader’s role in the provision of liquidity to a relatively uninformed market. • Informed traders submit more limit orders than liquidity traders. • Trading strategies and the book. • Crowding out: Consistent with theory, when there is a lot of depth on the “other side of the book” all traders are more likely to submit limit orders. • Trading and volatility. • Informed use market orders when the value of their information is high. • There is no significant difference in the use of limit orders across high and low volatility markets.

Measuring Liquidity • The authors define the provision of liquidity as the posting of a limit order and the use of liquidity as the taking of a limit order. • Seems standard but I don’t think its that simple. • Why is an extreme limit order posted far from the current best bid or ask given the same weight as the best bid or ask? • Provide instead an indication of how many limit orders are submitted within a few ticks of current trading. • Measure of the probability of being “hit”.

Informed Traders • Very nice intuition built for this behavior. • Information is useful to reduce the risk of providing liquidity. • Since the payoff is the same, the agent who provides liquidity is the one who can do so with the least risk. • At first I got very excited, then I thought, what else can they do? Another case of its obvious once you see it. • Suggest a check with one informed trader. • Figure 3 suggests most of their limit orders are “out of the money”. • Suggest a version of the game where the number of informed is not common knowledge.

Liquidity Traders • “Small” liquidity traders take an active role in providing liquidity. • What is the profit of small liquidity traders after they reach their quota? • Can they provide liquidity as well as the informed in this experiment? • “Large” liquidity traders are predictably the consumers of liquidity.

Trading Environment • Two minutes is not a lot of time. • Impact of discretionary liquidity trading can’t be effectively examined. • Suggest a robustness check using a setting in which you have cohorts trade securities for 10 minutes each. • May impact the behavior of the informed. • The opening: • Any evaluation of signaling behavior?

Subjects • Guaranteed $10 for participating. • Does this induce risk averse and/or risk seeking behavior? • Does the negative adjustment for informed cause risk seeking behavior?

Summary • A well executed and thought provoking study. • New role for information: reducing the risk of providing liquidity. • What is the benchmark? • Lots of things I’d like to see done. • The curse of writing something that makes you think.