Download

1 / 32

320 likes | 447 Vues

Capital Market Reinsurance Solutions July 9, 2001 Philip Kane, ACAS Tel: +1 212 723 5851 Philippe Joly Tel: +1 212 723-6461. Derivatives are any financial instrument which “derives” its value from some “underlying” asset or another derivative

E N D

Capital Market Reinsurance Solutions July 9, 2001 Philip Kane, ACAS Tel: +1 212 723 5851 Philippe Joly Tel: +1 212 723-6461

Derivatives are any financial instrument which “derives” its value from some “underlying” asset or another derivative The increase in the sophistication of the reinsurance market has paralleled the development of the derivatives market. Insurance Derivatives relate to those derivatives which are concerned with insurance risks, placed with insurers, or use insurance techniques and structures. Insurance Derivatives are used as an alternative to reinsurance transactions and as a new source of risk taking opportunities. But often they involve the blending of insurance and derivative structures. Insurance Derivative groups have been formed at all the major Investment Banks. At Citigroup, we are a 10 year old group with 8 professionals directly attached to insurance derivatives and handling transactions in excess of over $20 billion notional a year. Insurance Derivatives and Reinsurance Page 2

Risk Classes: Credit Risk Future Flows Project Finance Private Equity Basis Risks Residual Value Capital Market Risk Transfer Opportunities for the Reinsurance Market • Sovereign/Political Risk • Plant Outage • Volatility Risks • Correlation Risks • Weather Risks Page 3

Reasons for Reinsurance Risk Transfer Relationships Unique Risk Appetites (Class and level) Analytical Expertise Flexible Mandates RAT (Regulatory, Accounting, Tax) Risk Transfer Opportunities for the Reinsurance Market Page 4

CDO= Collateralized Debt Obligation CDO’s represent a class of financial instruments each composed of a portfolio of loans, bonds, or other debt form representing the obligations of underlying third parties to pay. These third parties are referred to as “names” and are pooled for diversity: there can be as many as 150 or more in a single CDO CDO’s are tranched in layers of risk: The first tranche or layer represents the first set of default losses between 0-5% of the notional and therefore is the riskiest. It is often referred to as the equity layer. The next tranche is the mezzanine tranche which represents the next losses between 5-10% of the notional. The remaining obligations are the last to default, and this layer is considered the least risky, and therefore named the senior tranche. Synthetic CDO Example Page 5

The Synthetic qualifier represents the use of derivatives transfer the risk of the losses to third parties without the debt notionals changing hands. This is done through Credit Default Swaps. Credit Default Swap: Two parties enter into an agreement whereby one party pays the other a fixed periodic coupon (premium) for the specified life of the agreement. The other party makes no payments unless a specified credit event occurs (floating payer). Credit events are typically defined to include a material default, bankruptcy, or debt restructuring for a specified reference asset. Upon a credit event the floating payer either pays the market value of the asset (physical settlement) or the difference between par and such market value (cash settlement). Credit Default Swap Page 6

CDO: Sample Capital Structure AAA+ Senior: 90% of notional BBB Mezzanine: 7% of notional Equity: 3% of notional B/BB Page 7

Moody’s is leading ratings provider for tranches Basic Rating model divides names into industry/country groups and reduces the total number of names to an index based on the notional in each group: this index is termed a diversity score This diversity score is used as the n for a binomial model Given the average rating, and historical defaults, a frequency can be determined for default. Assuming a recovery rate under each obligation one can determine the number of defaults necessary to provide losses to a tranche. This can be used to determine the expected loss within a tranche by assigning probability to each number of defaults Probability of a specific number (x) of defaults = n! / [x! (n-x)!] * (p)x(1-p) n-x Binomial Model of CDO’s Page 8

Historical Recovery Rates Page 10

From previous slides we assume a diversity score of 20, a 5 year average life, and an average Baa rating, producing a default frequency of 1.71%. We also assume a Recovery Rate of 50%. We are interested in determining the Expected Loss (and the rating) of Tranche, say, [4% , 8%] Using the binomial model we can produce the following distribution of defaults: Synthetic CDO Expected Loss Calculation using Binomial Model Page 11

CDOs: Note on Correlation An intuitive way of understanding the concept of Loss to a tranche is to realize that the E(Loss) to a small tranche dx is equal to the Probability of Attachment at x. This explains why the E(Loss) to a bottom tranche is essentially determined by the probability of attachment at the portfolio level. And the E(Loss) to a top tranche is essentially determined by the probability of Exhaustion at the portfolio Level. Probabilityof Exceedence 100% b E ( L[a,b] ) a a 0% b 100% 0% Page 12

Market was originally driven by Bank Regulatory Capital Relief Banks’ capital charge of 8% of notional on non-OECD bank debt; but only 1.6% for OECD banks and VAR (economic) charges for trading book. Therefore, banks with trading books can provide capital relief to non-trading book banks, and buy protection in the form of derivatives. Additional volume provided by non-bank Credit Derivative Trading volume Synthetic CDO Market has traded in excess of $400,000,000,000 of notional. Reinsurance Market has been attracted to the risk and structure of synthetic CDO’s due to actuarial pricing methodology and regulatory needs of end-buyers Credit-Default Swaps are also be treated as insurance policies for insurance regulatory purposes in certain jurisdictions (eg, Bermuda), allowing insurance entities to be providers of protection and the booking of insurance premiums Synthetic CDO Market Page 13

CDO: Actual Deal Page 14

Capital Relief Seeking Bank Synthetic CDO Market Premium Premium Reinsurance and Bank Market Counterparty Bank’s Trading Book Losses Losses Credit Default Swap Market Page 15

Market traded risks, even if in insurance form, should be marked to market based on US GAAP If blended with insurance or other risks, bifurcation should take place Insurance, weather, and other natural risks are specifically excluded from FASB 133 Credit risk is marked to market as a derivative but not as insurance. Insurers who choose to take credit risk in insurance form do not have to mark portfolio if the form meets GAAP criteria as a financial guarantee (identifiable failure to pay) but default swap providers do, regardless of jurisdiction . Currently, banks haven’t accepted insurance policies in trading books. The use of Transformers has been common to address this problem. Synthetic CDO Accounting Page 16

In order to qualify for the scope exception in paragraph 10(d), a financial guarantee contract must require, as a precondition for payment of a claim, that the guaranteed party be exposed to a loss on the referenced asset due to the debtor's failure to pay when payment is due both at inception of the contract and over its life. If the terms of a financial guarantee contract require payment to the guaranteed party when the debtor fails to pay when payment is due, irrespective of whether the guaranteed party is exposed to a loss on the referenced asset, the contract does not qualify for the scope exception in paragraph 10(d). Even if, at the inception of the contract, the guaranteed party actually owns the referenced asset, the scope exception in paragraph 10(d) does not apply if the contract does not require exposure to and incurrence of a loss as a precondition for payment. Furthermore, to qualify for the scope exception in paragraph 10(d), the compensation paid under the contract cannot exceed the amount of the loss incurred by the guaranteed party. Accounting: Statement 133 Implementation Issue No. C7 Page 17

The guaranteed party's exposure to and incurrence of a loss on the referenced asset can arise from owning the referenced asset or from other contractual commitments, such as in a back-to-back guarantee arrangement. The application of the scope exception to financial guarantee contracts under which the guaranteed party incurs a loss resulting from the debtor's failure to pay either because it owns the referenced asset or because of other contractual commitments is consistent with the reasoning for Statement 133's scope exception for certain insurance contracts. Paragraph 281, which relates to the exclusion of certain insurance contracts from the scope of Statement 133, indicates that those contracts are excluded from the scope because they entitle the holder to compensation only if, as a result of an identifiable insurable event (other than a change in price), the holder incurs a liability or there is an adverse change in the value of a specific asset or liability for which the holder is at risk. Accounting: Statement 133 Implementation Issue No. C7(Continued) Page 18

Reinsurance Transactions often address financial issues that can also be addressed by the capital markets Property Catastrophe risk linked notes Life Reinsurance may transfer interest rate risks which can be addressed by the interest rate swap market Life and P/C Surplus Relief could be structured with an SPV supported by a securitization of the profits Contingent Capital can be securitized in form of a note with different spreads pre- and post- contingency/exercise. Dual Risk Covers: Cat Protection contingent on equity index move Aggregate Stop Losses can include financial risks such as interest rate risks Capital Market Alternatives to Reinsurance Page 19

Stop Loss which combines both losses on asset and liability side By converting asset risk into a formula using duration, notional, and interest rates, can generate losses on asset side derived from interest rate movements Covered losses under reinsurance would include indexed interest rate losses as above When these losses and insurance losses exceeded attachment point, reinsurer pays, up to limit. Usual duration is one year, covering all lines of insurance business as well. Catastrophe losses are usually capped as well. Combined Aggregate Stop Loss Example Page 20

Aggregate Loss Models are available for insurance risks and are usually based on stochastic models of losses Insurance risks are generally modeled with statistical models and insurance risk only stop losses are generally priced using Monte Carlo simulation Issues are generally correlations, event losses (catastrophe), trended and untrended expected loss ratios, growth rates, etc…. Transaction models combining asset risk with insurance risks have generally added these risks as another stochastic variable. For liquid risks such as short interest rates there can be great divergence between insurance pricing and Capital Markets pricing. For illiquid risks, the pricing results tend to converge due to the lack of liquid markets for these risks. These risks get treated as event risks in the capital markets much like insurance pricing rather than continuous risks. Combined Aggregate Stop Loss Pricing Page 21

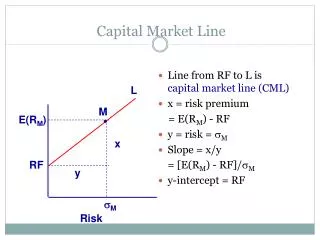

Insurance Pricing vs. Derivatives Pricing Typical Insurance Pricing: ‘Call Contract’ S=110 Probability: p = 55% Option Value = 10 S=100 Interest Rate: r = 5% Probability: 1-p = 45% S=90 Option Value = 0 Option Price: S= [ p.10 + (1-p).0 ]/ (1+r) = 10p / (1+r) = 5.24 Page 22

Insurance Pricing vs. Derivatives Pricing Derivatives Pricing: Call Option S=110 Probability: p = 55% Option Value = 10 S=100 Interest Rate: r = 5% Probability: 1-p = 45% S=90 Option Value = 0 Pricing is determined by the construction of a replicating portfolio, not by actual probabilities Page 23

Insurance Pricing vs. Derivatives Pricing Derivatives Pricing: Building a Replicating Portfolio made of x bonds and y underlying securities S=110 Portfolio = ( -0.42 Bonds , 0.5 securities)Portfolio Value = -0.42*105 + 0.5 * 110 = 110 Probability: p = 55% Option Value = 10 Interest Rate: r = 5% S=100 Portfolio = ( -0.42 Bonds , 0.5 securities)Portfolio Value = -0.42*105 + 0.5 * 90 = 0 Probability: 1-p = 45% S=90 Option Value = 0 The option and the Porfolio have the same final value in all cases, therefore they should have the same price at time 0 Option Price = -0.42 * 100 + 0.5 * 100 = 7.14 Page 24

Insurance Pricing vs. Derivatives Pricing Derivatives Pricing: Using Risk-Neutral Probabilities S=110 Probability: p = 55% Option Value = 10 S=100 Interest Rate: r = 5% Probability: 1-p = 45% S=90 Option Value = 0 If we calculate the probability p* satisfying 100 * (1.05) = 110 p* + 90 (1- p*) p* = 0.75, then we can check that [ 10 p* + 0 (1- p*) ] / (1+r) = 7.14 = Call Price Page 25

Combined Aggregate Stop Loss Pricing • We will assume for each .005% change in interest rates, the bond portfolio moves a value equal to 1% of premium. • We will also assume no correlation between a move in interest rates during the year and the resulting accident year loss ratio. • The cover will be 20% in excess of 70%, with a sublimit of 10% on asset losses due to interest rate moves Page 26

Combined Aggregate Stop Loss Pricing • The interest rate option payoff is based on the cumulative change in the required premium from the pure loss (no interest rate moves) premium. • The Premium changes as the effective loss ratio attachment drops due to interest rate losses. • Assuming this option cost 1.5% and the pure stop loss cost 4%, the total upfront premium would be 5.5%. • With this payoff we can arrange an interest rate only option for a reinsurer to be able to bind a combined aggregate stop loss delivering the necessary premium to underwrite the loss risk. • This could also be done for “finite” stop loss covers and multi-year stop loss covers. Page 28

Combined Aggregate Stop Loss Accounting • There is no explicit accounting pronouncements on Combined Aggregate Stop Loss Covers. • There have been FAS clarifications of combined insurance and financial risks. • There would be merit to NOT bifurcating the interest rate option embedded in the trade. • This is because a pure loss ratio in excess of 60% is required for any interest rate losses to be covered, and this is not certain. • The insured must also actually experience the interest rate losses, much like the actual loss requirement of industry loss covers. Page 29

Only those contracts for which payment of a claim is triggered only by a bona fide insurable exposure (that is, contracts comprising either solely insurance or both an insurance component and a derivative instrument) may qualify for the exception under paragraph 10(c). In order to qualify, the contract must provide for a legitimate transfer of risk, not simply constitute a deposit or form of self-insurance. A property and casualty contract that provides for the payment of benefits/claims as a result of both an identifiable insurable event and changes in a variable would in its entirety qualify for the insurance exclusion in paragraph 10(c)(2) of Statement 133 (and thus not contain an embedded derivative instrument that is required to be separately accounted for as a derivative instrument) provided all of the following conditions are met: 1.Benefits/claims are paid only if an identifiable insurable event occurs (for example, theft or fire) pursuant to the requirements of paragraph 10(c)(2) of Statement 133. Accounting: Statement 133 Implementation Issue No. B26 Page 30

2.The amount of the payment is limited to the amount of the policyholder’s incurred insured loss. 3.The contract does not involve essentially assured amounts of cash flows (regardless of the timing of those cash flows) based on insurable events highly probable of occurrence because the insured would nearly always receive the benefits (or suffer the detriment) of changes in the variable. If there is an actuarially determined minimum amount of expected claim payments (and those cash flows are indexed to or altered by changes in a variable) that are the result of insurable events that are highly probable of occurring under the contract and those minimum payment amounts are expected to be paid each policy year (or on another predictable basis), that "portion" of the contract does not qualify for the insurance exception. Accounting: Statement 133 Implementation Issue No. B26 (Continued) Page 31

Conclusions • Convergence is here!! • Capital Markets are sourcing risks for the Reinsurance market as well providing solutions to insurance problems • Be cautious when underwriting liquid risks, but look for structural exploitations. • In illiquid risk markets there are many opportunities for savvy players and Reinsurers are a major player. • Re/insurance has unique regulatory, accounting, and tax implications that can work to the advantage or disadvantage of transactions. Page 32