Three important dates

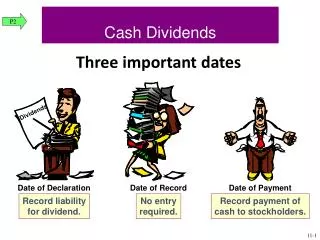

Cash Dividends. P2. Three important dates. Dividends. Date of Declaration. Date of Record. Date of Payment. Record liability for dividend. No entry required. Record payment of cash to stockholders. 11- 1. 100 shares. HotAir, Inc. Common Stock. $1 par. Stock Dividends. P2.

Three important dates

E N D

Presentation Transcript

Cash Dividends P2 Three important dates Dividends Date of Declaration Date of Record Date of Payment Record liability for dividend. No entry required. Record payment of cash to stockholders. 11-1

100 shares HotAir, Inc. Common Stock $1 par Stock Dividends P2 The corporation distributes additional shares of its own stock to its stockholders without receiving any payment in return. • Why a stock dividend? • Can be used to keep the market • price of the stock affordable. • Can provide evidence of • management’s confidence that • the company is doing well. 11-2

Stock Dividends P2 Small Stock Dividend • Distribution is £ 25% of the previously outstanding shares. • Capitalize retained earnings for the market value of the shares to be distributed. Large Stock Dividend • Distribution is > 25% of the previously outstanding shares. • Capitalize retained earnings for the minimum amount required by state law, usually par or stated value of the shares. 11-3

Recording a Small Stock Dividend P2 On December 31, 2013, Quest declared a 2% stock dividend, when the stock was selling for $10 per share. The stock will be distributed to stockholders on January 20, 2014. Let’s make the December 31 entry. Temporary equity account 100,000 × 2% = 2,000 × $10 = $20,000 2,000 × $1 par = $2,000 11-4

P2 Before the stock dividend. Same amount After the stock dividend. 11-5

Recording a Large Stock Dividend (greater than 25%) P2 Router, Inc. shows the following stockholders’ equity section just prior to issuing alargestock dividend. 11-6

Recording a Large Stock Dividend (greater than 25%) P2 On December 31, 2013, Router declared a 40% stock dividend, when the stock was selling for $8 per share. State law requires that large stock dividends be capitalized at par value per share. 50,000 × 40% = 20,000 shares × $1 par value = $20,000 11-7

New Shares Stock Splits(Example of a 2 for 1 Stock Split) P2 A distribution of additional shares of stock to stockholders according to their percent ownership. $10 par value Old Shares Common Stock 100 shares $5 par value Common Stock 200 shares 11-8

Before and After the 2-for-1 split, the stockholders’ equity section of the balance sheet looks like this: Stock Splits P2 No accounting entry is made. 11-9

Statement of Retained Earnings C3 Retained earnings is the cumulative amount of reported net income less any net losses and dividends declared since the company started operating. 11-10

Basicearnings per share Net income - Preferred dividends Weighted-average common shares outstanding = Earnings per Share A1 Earnings per share is one of the most widely cited items of accounting information. 11-11

Price- earnings ratio Market value (price) per share Earnings per share = Price-Earnings Ratio A2 This ratio reveals information about the stock market’s expectations for a company’s future growth in earnings, dividends, and opportunities. If earnings go up, will the market price of my stock follow? 11-12

Dividend yield Annual cash dividends per share Market value per share = Dividend Yield A3 Tells us the annual amount of cash dividends distributed to common stockholders relative to the stock’s market price. 11-13

Stockholders’ equity applicable to common shares Number of common shares outstanding Book value per common share = Book Value per Share—Common A4 Reflects amount of stockholders’ equity applicable to common shares on a per share basis. 11-14

Stockholders’ equity applicabletopreferredshares Number ofpreferred shares outstanding Book value perpreferredshare = Book Value per Share—Preferred A4 Reflects amount of stockholders’ equity applicable to preferred shares on a per share basis. 11-15