Download

1 / 24

240 likes | 416 Vues

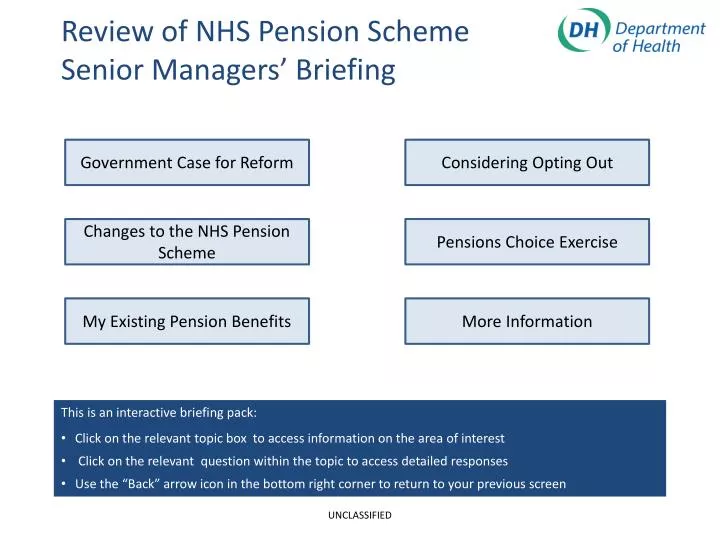

Review of NHS Pension Scheme Senior Managers’ Briefing. Government Case for Reform. Considering Opting Out. Changes to the NHS Pension Scheme. Pensions Choice Exercise. My Existing Pension Benefits. More Information. This is an interactive briefing pack:

E N D

Review of NHS Pension Scheme Senior Managers’ Briefing Government Case for Reform Considering Opting Out Changes to the NHS Pension Scheme Pensions Choice Exercise My Existing Pension Benefits More Information • This is an interactive briefing pack: • Click on the relevant topic box to access information on the area of interest • Click on the relevant question within the topic to access detailed responses • Use the “Back” arrow icon in the bottom right corner to return to your previous screen UNCLASSIFIED

Government Case for Reform The Benefits of an NHS Pension Why does the NHS Pension Scheme need to change? What about the NHS Pension Scheme’s surplus? Are the changes fair across the generation of scheme members? Is it fair to replace a Final Salary scheme with a Career Average Earnings Scheme? Back UNCLASSIFIED

Government Case for Reform The Benefits of an NHS Pension • Remains a very effective way to save for your retirement. • Will continue to be a defined benefit scheme i.e. based on your salary rather than on investment returns. • A significant employer contribution (currently 14%). • Provides additional benefits for your family including: • A death in service benefit • Survivors benefits • An Ill health pension Back UNCLASSIFIED

Government Case for Reform Why does the NHS Pension Scheme need to change? • The costs of providing public service pension schemes continue to rise. The current arrangements are not sustainable and affordable in the long term (Hutton review of public sector pensions). • The NHS Pension Scheme was modernised in 2008 with a view to striking a better balance of how costs were met by both scheme members and the tax payer. These changes did not however go far enough. The average contribution by NHS Pension Scheme members only increased by 0.5% in 2008. • People are living longer. The average 60 year old is now living 10 years longer than they did in the 1970s. This increases the cost to the tax payer as pensions are generally being paid for longer periods of time. • There is a need to ensure intergenerational fairness i.e. that those benefiting from the NHS Pension Scheme pay for it, as opposed to future members needing to subsidise current members. Back UNCLASSIFIED

Government Case for Reform What about the NHS Pension Scheme’s ‘surplus’? • The NHS Pension Scheme is unfunded (i.e. there is no ‘pot’ of money set aside from which to pay pensions) and the Government pays pensions from public finances. • There is a positive balance in the current year as the contributions made by scheme members and employers are more than the cost of the benefits being paid out to retired members. • The scheme does however need to account for pension promises that current members are currently building, to be paid when they retire. • The NHS employs significantly more staff that it did in the 1990s and therefore more pension promises are being built. With the existing contribution structure, the current ‘surplus’ is set to shortly disappear. • A ‘surplus’ at any given point in time does therefore not guarantee the long term affordability of the scheme. This is similar to having a positive balance on your current account at the start of the month whilst knowing that you have bills to pay during the month. Back UNCLASSIFIED

Government Case for Reform Are the changes fair across the generation of scheme members? • 2008 scheme changes enabled NHS staff to retain their current pension arrangements. • Cost of people living longer would however be passed to current scheme members and would be re-assessed at scheme valuations (every 4 years). Whilst this started to address the affordability of public sector pensions the reform was considered insufficient. • Hutton stated that "allowing current members to accrue further benefits in the present schemes for many decades would be unfair and inequitable to the new members coming in behind them“. • Current proposals therefore allow for a greater proportion of the cost of longevity to be borne by those who benefit from the improvements. • Pensions accrued to date are however protected (accrued rights). Back UNCLASSIFIED

The Case for Reform Is it fair to replace a Final Salary scheme with a Career Average Earnings Scheme? • Hutton highlighted the need for fairness in the value of the benefits received by all scheme members. • With a Final Salary scheme, 'high flyers' receive a greater pension in relation to their contribution than 'low flyers‘. • The introduction of tiered contributions made little impact on this. • Moving to Career Average based pensions addresses this balance. Back UNCLASSIFIED

Changes to the NHS Pensions Scheme Changes to Pensions from April 2011 Changes to Pensions from April 2012 Potential Changes for 2015 Employer Contributions Back UNCLASSIFIED

Considering Opting Out I can’t afford to pay more. Can I opt out of the pension scheme? Opting out with less than 2 year’s membership. Opting out with more than 2 year’s membership. Would I be better making alternative pension arrangements? Back UNCLASSIFIED

My Existing Pension Benefits Protecting your accrued rights. An example of accrued rights. Back Back UNCLASSIFIED

Pensions Choice Exercise What is the Pensions Choice Exercise? How is the Pensions Choice Exercise linked to other reforms of the NHS Pension Scheme? Back Back UNCLASSIFIED

My Existing Pension Benefits Protecting your accrued rights • You will keep any pension and lump sum earned to date. • Often referred to as 'Accrued Rights‘. • All active NHS Pension Scheme members who as of 1st April 2012 have 10 years of less to their current pension age will see no change in when they can retire, nor any decrease in the amount of pension they receive at their Normal Pension Age. • Members who are within a further 3.5 years of their normal pension age will have limited protection with linear tapering so that for every month of age that they are beyond 10 years of their normal pension age, they lose 2 months of protection. Back Back UNCLASSIFIED

My Existing Pension Benefits An example of accrued rights • John joined the NHS on 1st April 1988 and has been a member of the NHS Pension Scheme ever since. He plans to retire on 1st April 2028. • John's benefits will be calculated as follows: • He will receive 27 years worth of service based on his final salary when he retires (using the existing rules to calculate pensionable pay e.g. best of the last 3 years). This part of John's pension remains a Final Salary pension and is referred to as his Accrued Rights. • His pension benefits earned from 1st April 2015 will be based on John's salary for each year that he then works i.e. a year of pension benefit is earned based on his pay per year between 2015 and 2028. This is known as a Career Average earnings based pension. • Each year’s salary will be indexed by CPI + 1.5% when calculating John’s Career Average pension to address the effect of inflation between when John earned the money and when his pension will be paid. This method of indexation allows for the fact that over time, wages generally increase by more than the standard rate of inflation. Back Back UNCLASSIFIED

Changes to the all Public Service Pension Schemes Changes to Pensions from 1st April 2011 The following changes came into effect for all pension schemes from 1st April 2011: • The annual allowance (the maximum amount that pension benefits can grow each year and still receive tax relief) is reduced from £255,000 to £50,000. • The rate by which public sector pensions will be increased annually was linked to the Consumer Price Index (CPI) rather than the Retail Price Index (RPI). Back UNCLASSIFIED

Changes to the NHS Pensions Scheme Changes to Pensions from 1st April 2012 • The lifetime allowance is reduced from £1,800,000 to £1,500,000. • Employee contributions will increase for some members from 1st April 2012: • Those earning less than £26,558 will not see a rise in their contributions. • Those earning £26,558 to £48,982 will see a rise of 1.5% in their contributions. • Those earning £48,983 or more will see a rise if 2.4% in their contributions. • Members will receive tax relief on an increases, thus making the maximum net increase 1.44%. • There are plans to consult on further contribution rises for 2013-14 and 2014-15. Back UNCLASSIFIED

Changes to the NHS Pension Scheme Potential Changes for 2015 NHS officials and Trade Unions are discussing how the NHS Pension scheme will look from 2015. Key elements of the proposed scheme design include: • Full protection of your benefits earned to date (your ‘accrued rights’). • Protection for staff with less than 10 years to their pension age (with partial protection for those within a further 3.5 years of this). • A move to a career average earnings scheme rather than final salary for pension benefits earned from 2015. • An improved accrual rate of 1/54ths for this scheme. Back UNCLASSIFIED

Changes to the NHS Pension Scheme Employer Contributions Employer Contributions Until 2015 • Employers currently contribute 14% of a member’s salary to their pension. • This level of contribution will continue until 2015. Employer Contributions Post 2015 • Employers will continue to make a significant contribution to members’ pensions from 2015. • The level of future employer contributions will be determined by a scheme valuation exercise prior to 2015. Employers will be required to contribute the difference between what the emloyees pay and the total cost of the scheme. Back UNCLASSIFIED

Considering Opting Out I can’t afford to pay more. Can I opt out of the pension scheme? • Nobody has to stay in the NHS Pension Scheme. • Members should obtain all the facts before opting out. • Leaving the scheme will mean you lose your employer’s contribution to your pension (effectively a 14% “pay cut”). • Your accrued pension benefits will be based on your salary when you leave the scheme rather than when you leave the NHS. • You will be required to pay a higher rate of National Insurance (meaning that your take-home pay doesn’t increase by as much as you had anticipated by opting out). • You will naturally no longer receive tax relief on your contributions. • You will give up your Death in Service benefits (a payment of twice your salary if you die). Back UNCLASSIFIED

Considering Opting Out Opting out with less than 2 year’s membership • Your contributions will be refunded. • Any savings made on tax and National Insurance (as a result of you receiving tax relief on contributions and paying a lower rate of National Insurance) during your period as a scheme member will be deducted from this refund. Back UNCLASSIFIED

Considering Opting Out Opting out with more than 2 year’s membership • You will not receive a refund of contributions. • Your pension benefits will be preserved and paid at your Normal Pension Age. • These benefits will be up-rated by the Consumer Price Index but are based on your final pensionable pay and length of service when you leave the scheme (not when you leave the NHS). Back UNCLASSIFIED

Considering Opting Out Would I be better making alternative pension arrangements? • The NHS Pension Scheme continues to offer excellent value to staff. • The Government Actuary’s Department estimates that for each £1 you contribute you can expect to receive pension benefits of between £3 and £6. • The Government is committed to ensuring that Public Service Pensions continue to be amongst the best available. • The pensions that individuals will receive at normal pension age will be broadly as generous for low and middle earners as they are now. Back UNCLASSIFIED

More Information • For the latest updates on the reform of the NHS Pension Scheme, and a calculator to work out your benefits, visit: www.dh.gov.uk/pensions • For member and employer based guidance on the existing NHS Pension Scheme: www.nhsbsa.nhs.uk/pensions • For details of the workforce implications of changes to the NHS Pension Scheme: www.nhsemployers.org/PAYANDCONTRACTS/NHSPENSIONSCHEMEREVIEW/Pages/NHSPensionScheme.aspx • For full details of the government's reform of public service pensions: www.hm-treasury.gov.uk/tax_pensions_index.htm Back UNCLASSIFIED

Pensions Choice Exercise What is the Pensions Choice Exercise? • The NHS Pension Choice exercise aims to provide all eligible members of the NHS Pension Scheme a one-off option to transfer all of their membership from the 1995 Section into the 2008 Section if they wish. • Eligible members are each receiving a Choice Pack which includes an Explanatory Booklet, a Choice Statement (showing a comparison of benefits in the 1995 and 2008 Section) and a DVD. • Given the logistical size of the exercise was scheduled to last from 1 October 2009 to March 2012. It is on schedule to be completed by March 2012. Choice packs have been delivered to employers in a number of phases based on a national timetable. • The Choice Exercise is now complete for the vast majority of NHS staff. Back UNCLASSIFIED

Pensions Choice Exercise How is the Pensions Choice Exercise linked to other reforms of the NHS Pension Scheme? • The Choice exercise commenced prior to the review of public sector pensions. • The exercise continues to run in parallel with detailed scheme discussions that aim to finalise new pension arrangements. • Any Choice made by a scheme member remains valid. • An assessment will be undertaken once the new pension scheme arrangements are finalised to ensure that members have not been potentially disadvantaged by making an inappropriate Choice in light of the new arrangements. Back UNCLASSIFIED