Download

1 / 28

280 likes | 413 Vues

Making your plan for life. P-ENROLL-PRES-all 1-11 RPS 102535. We’re here to help. William Curtis (404) 231-7103 William_Curtis@ml.com Jay Geaslen (404) 264-7267 Jay_Geaslen@ml.com. Transition Details. Transition Details.

E N D

Making your plan for life. P-ENROLL-PRES-all 1-11 RPS 102535

We’re here to help. William Curtis (404) 231-7103 William_Curtis@ml.com Jay Geaslen (404) 264-7267 Jay_Geaslen@ml.com

Transition Details • The blackout period for your plan is: December 15, 2011 – January 20, 2012 • During this time, you will temporarily be unable to: • Direct or diversify investments • Obtain a distribution

Transition Details • During the blackout period, your account balances will be invested in • the investment options that have • been determined to be similar to the investments you are currently • invested in. • Your future contributions will be invested based on the same instructions.

Transition Details • Last Day to Request a distribution or withdrawal: December 15, 2011 • Last Day to Change Investment Elections: December 23, 2011 • Last Day to Transfer Investment Options: December 23, 2011 • Last Day for Balance Inquiries: December 23, 2011 • First Payroll Contribution to Hartford: December 30, 2011 • Date of Plan Asset Liquidation: January 03, 2012 • Plan Assets are wired to Hartford and invested into like funds: January 04, 2012 • Blackout period ends: January 20, 2012

SAVING FOR RETIREMENT IS MORE IMPORTANT THAN EVER.

Don’t forget inflation. “The biggest financial concern for people facing retirement is meeting everyday expenses.” Source: The Hartford Investments and Retirement Survey, November 2009

Social Security Less than 40% of retirement income typically comes from Social Security benefits. Source: Social Security Administration Online, 2009, ssa.gov/planners/morecalculators.htm

We’re living longer than ever. • 80,000 Americans will turn 100 in 2010. • By the year 2030, that number willclimb to more than 200,000 • – and that may include you. Source: www.census.gov, 2009

Four great reasons to participate: • It’s simple and convenient. • It’s flexible. • You may save on taxes. • It goes where you go.

Smart saving starts early. Smart savings starts early. Assumes hypothetical weekly contributions of about $29 with a 6% annual rate of return, compounded weekly. Rates of return will vary over time, particularly for long-term investments. There is no guarantee that the selected rate of return can be achieved. Hypothetical results are for illustrative purposes only and are not intended to predict the future performance of any investment option. The principal value and return of an investment will fluctuate with changes in market conditions. Your account may be worth more or less than your original investment.

Plan Highlights • Eligibility age 21; 1 month of service • Entry dates monthly • Change contribution monthly

Consider the Roth option. Traditional before-tax contributions • Possible tax savings on your • take-home pay now • Tax-deferred earnings Roth after-tax contributions • Federal tax-exempt withdrawals when you retire* *A distribution is not subject to income tax if the Roth account has been in place for at least five tax years and the distribution is made on or after the attainment of age 59½,or is due to disability or death.

TRADITIONAL Pre-tax contributions Grow Tax-deferred Taxed as ordinary income when withdrawn ROTH 401 After-tax contrib. Grow Tax-deferred 2 rules: 5 Years Age 59 ½ Withdraw qualified earnings income tax-free Traditional and Roth 401(k) Compared

Contribute to your max. • Decide how much you can save. Even small contributions can make a difference. • Periodically increase the amount to boost your savings potential. The maximum annual contribution for 2012 is $17,000, or $22,500 if you’re age 50 or older.

You can add assets from another plan. • Consolidated balances • Single statement • Increased accumulation potential • Possible lower investment expenses • Transfers among plan’s investment options • Diversification

We’re here to help. In person William Curtis & Jay Geaslen Hartford Toll-free access: 800-854-0647 In print Online thehartford.com/retirementplans/access

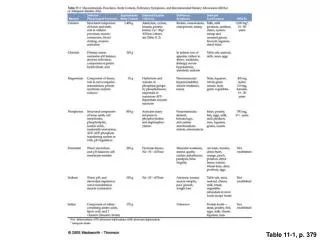

The case for allocation and diversification. Annual Returns (%) of Asset Classes (12/31/96 - 12/31/10) Neither asset allocation nor diversification guarantee a profit or protect against a loss.

About the previous chart. INDEX PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. Indices are unmanaged, not available for direct investment, and do not represent the performance of a specific fund. You cannot invest directly in the indices. The historical performance of each index cited in this material is provided to illustrate market trends; it does not represent the performance of any particular investment product. Indices do not include payment of any expenses, fees, or sales charges which would lower performance results. Large-Cap stocks are represented by the S&P 500 Index, which is a market-capitalization weighted price index composed of 500 widely held U.S. common stocks, frequently used as a measure of U.S. stock market performance.. Mid-Cap stocks are represented by the S&P 400 Index, which is an index measuring the performance of the mid-size company segment of the U.S. market. Small-Cap stocks are represented by the Russell 2000 Index, which includes the smallest 2000 securities in the Russell 3000. Small-cap stocks involve greater risks due to their smaller size and lesser liquidity.

About the previous chart. International stocks are represented by the MSCI Europe, Australasia, Far East Index which measures the performance of the leading stocks in 20 developed countries outside of North America. Investing in foreign securities may involve different and additional risks associated with foreign currencies, investment disclosure, accounting, securities regulation, commissions, taxes, political or social instability, war, or expropriation. Bonds are represented by the Barclays Capital Aggregate Bond Index, which includes U.S. government, corporate, and mortgage-backed securities with maturities up to 30 years. Bonds, if held to maturity, provide a fixed rate of return and a fixed principal value. Bond funds will fluctuate, and when redeemed, may be worth more or less than their original cost. Cash Investments are represented by the Merrill Lynch U.S. Treasury Bill Index (0-3 Months). Three-month Treasury Bills are short-term securities issued by the U.S. government that are generally considered to be risk-free. Diversified Portfolio is represented by an equal portion (20% each) of the previously listed indices, excluding cash investments. Data source: Morningstar, 1/11.

Important information Many tax planning strategies emphasize the deferral of current income taxes, on the basis that your federal income tax rate may be lower at retirement. Please keep in mind that federal income tax rates are unpredictable and may be higher when you take a distribution than at the time of deferral. Other factors, including state tax rates and your income, may also affect your overall tax rate upon distribution. Please consult with your tax advisor for individual tax planning strategy and advice. The Hartford does not predict or in any way guarantee favorable tax results.

Important information This information is written in connection with the promotion or marketing of the matter(s) addressed in this material. This information cannot be used or relied upon for the purpose of avoiding IRS penalties. These materials are not intended to provide tax, accounting or legal advice. As with all matters of a tax or legal nature, you should consult your own tax or legal counsel for advice.

Important information Before investing, you should carefully consider the investment objectives, risks, charges and expenses of the mutual funds or The Hartford's group variable annuity products and funding agreements, and their underlying funds. For fund and product prospectuses and/or a disclosure document containing this and other information, contact your financial professional or visit our website. Read them carefully.

Important information "The Hartford" is The Hartford Financial Services Group, Inc. and its subsidiaries, including Hartford Life Insurance Company, Hartford Retirement Services, LLC (“HRS”), and Hartford Securities Distribution Company, Inc. ("HSD"). HSD (member FINRA and SIPC) is a registered broker/dealer affiliate of The Hartford. Retirement programs can be funded by group fixed or variable annuity products and funding agreements issued by Hartford Life Insurance Company (Simsbury, CT). Group variable contracts are underwritten and distributed by HSD, where applicable. HRS and HSD offer certain service programs for retirement plans through which a sponsor or administrator of a plan may also invest in mutual funds on behalf of plan participants.