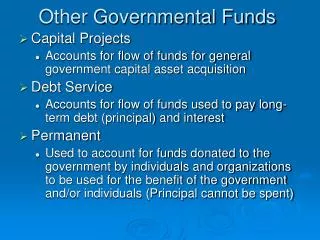

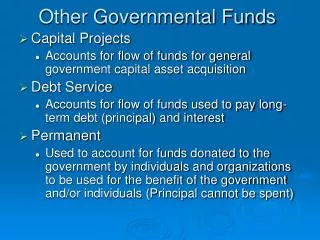

Other Governmental Funds

70 likes | 213 Vues

Other Governmental Funds. Capital Projects Accounts for flow of funds for general government capital asset acquisition Debt Service Accounts for flow of funds used to pay long-term debt (principal) and interest Permanent

Other Governmental Funds

E N D

Presentation Transcript

Other Governmental Funds • Capital Projects • Accounts for flow of funds for general government capital asset acquisition • Debt Service • Accounts for flow of funds used to pay long-term debt (principal) and interest • Permanent • Used to account for funds donated to the government by individuals and organizations to be used for the benefit of the government and/or individuals (Principal cannot be spent)

Capital Projects Fund • Exists for duration of the project • Modified Accrual basis of accounting • Flow of current financial resources • Revenues (Few, maybe grants, miscellaneous) • Bond and note proceeds are Other Financing Sources • Also, transfers-in (i.e., general fund) are OFS • Expenditures are for the capital project • Budget not used but encumbrances are

*Acquisition of general fixed assets by lease agreements is treated similar to businesses. Expenditures are debited for the present value of future lease payments and other financing sourcescredited. *Subsequent rental payments are recorded as expenditures for principal and interest *Special Assessments accounting depends on whether or not the government is primarily or secondarily liable for repayment of the debt. If so, reported on G-W financial statements; If not, reported as an Agency (Fiduciary) Fund event.

Debt Service Fund • Used to accumulate funds for repayment of general long-term debt and interest • Adjusted modified accrual basis of accounting (Interest expenditures as interest comes due, unless within 30 days and balance in DS Fund to pay) • Budgets are used but not encumbrances • Premiums or discounts on issuance of bonds are entered as OFS or OFU in debt service fund

Debt Service, Continued • Revenues • Taxes imposed for repayment of debt • Grants and restricted donations • Other Financing Sources • Transfers-in from other funds • Expenditures • Bond Interest in period due (except, 30 day rule) • Bond Principal in period due

Permanent Funds • Accounts for funds that are legally restricted (principal cannot be expended) • Earnings are to be used for benefit of government and citizens at-large • Modified Accrual basis of accounting and current flow of financial resources measurement focus • Revenues are contributions, investment income, and grants • Expenditures are disbursements on basis of restriction

Financial Statements • Balance Sheet • Disaggregated (Column for each major fund and summary of all non-major funds) • Current Financial Resources and Liabilities • Fund Balances (Reserved and Unreserved) • Statement of Revenues, Expenditures, and Changes in Fund Balances • Disaggregated • Modified Accrual Basis of Accounting • Expenditures are current, debt service and capital outlay • Bottom line is Ending Fund Balances