The Demand for Goods

Learn about the demand for goods, consumption, investment, government spending, and equilibrium output in economics. Explore exogenous and endogenous variables, equation types, and steps to solving economic models.

The Demand for Goods

E N D

Presentation Transcript

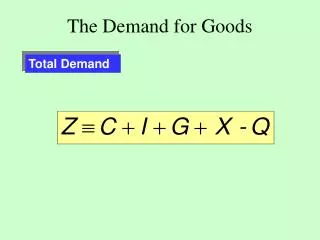

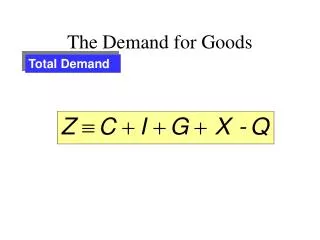

The Demand for Goods Total Demand

The Demand for Goods Consumption (C) • C = C0 +C1YD • C1 = propensity to consume • Change in C from a dollar change in income • 0 < C1< 1

The Demand for Goods Consumption (C) • C = C0 + C1YD

The Demand for Goods Investment (I) Investment is an exogenous variable • Exogenous variables • Variables that are assumed to be given and are not explained within the model

The Demand for Goods • Endogenous Variables • Variables that depend on other variables in the model • C is endogenous because it responds to production (Y) C = C0 – C1 (Y – T)

The Demand for Goods Government Spending (G) • G & T are exogenous • no reliable behavioral role for G & T • G & T are determined outside the model

The Determination ofEquilibrium Output Demand for Goods (Z)

The Determination ofEquilibrium Output The Model and Equation Types • Identity Equations • Behavioral Equations • Equilibrium Equations

The Determination ofEquilibrium Output Three Steps to Solving a Model 1) Algebra to confirm the logic 2) Graphs to build the intuition (but we’ll skip the 45° - line diagram) 3) Words to explain the results

The Determination ofEquilibrium Output Finding Equilibrium • Y = supply • Z = Demand = • Y = Z @ equilibrium

The Determination ofEquilibrium Output The Algebra • Dividing both sides by (1 - C1) gives

The Determination ofEquilibrium Output The Algebra: Y=Z

The Determination ofEquilibrium Output Answers • The larger the propensity to consume, C1, the larger the multiplier • A change in autonomous spending will change output more than the direct change in autonomous spending