Download

1 / 7

70 likes | 167 Vues

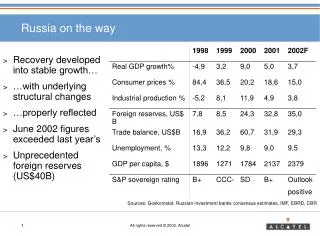

The telecom market in Russia has shown stable growth with structural changes, reflecting in the 2002 figures surpassing the previous year. Foreign reserves hit a record high of US$40B. Key players, both Russian and foreign, have made significant investments in mobile, internet, and emerging technologies. Despite global economic challenges, Russia remains an attractive market with potential for long-term growth. Private and foreign investors are eyeing the telecom sector as a lucrative opportunity for expansion and development.

E N D

Russia on the way • Recovery developed into stable growth… • …with underlying structural changes • …properly reflected • June 2002 figures exceeded last year’s • Unprecedented foreign reserves (US$40B) Sources: Goskomstat, Russian investment banks consensus estimates, IMF, EBRD, CBR

Telecom Services: General Sources: Ministry of Telecommunications, Alcatel Russia Market Research estimations, J’son & Partners, IDC

Telecom Services: Segments • Mobile and Internet are the main growth sources, however the latter is still very small in absolute terms, limited by PC (or other terminals) density

Coming Technologies • Newest technologies are coming to the Russian market • ADSL – 7Klines already installed (6KLines in Moscow) • DWDM line already installed: Moscow – St.P • UMTS successful trials conducted by all three major GSM operators • BPON network is deployed in the Moscow region • But progress is limited by lack of demand: • ADSL is too expensive and copper is not unbundled • Transnational capacity is still available • UMTS demand and license policy are unclear • FTTx technologies are probably currently too expensive

Key Russian players: mostly private • Svyazinvest (75%-1 Russian State, 25%+1 George Soros led consortium) • Controlling stakes in the absolute majority of fixed regional incumbents • Sistema (privately owned, diversified investments in finance, insurance, retail, manufacturing, oil, telecoms, etc.) • Investments in largest Russian mobile operator MTS (42% ownership) • Investment in Moscow incumbent (51% ownership) • Alfa Group (privately owned, diversified investments in finance, insurance, retail, manufacturing, oil, telecoms, etc.) • Investments in the second largest Russian mobile operator VimpleCom • Investment in the Russia’s largest CLEC – Golden Telecom • Telecominvest (privately owned) • Investment in the third largest Russian mobile operator Megafon • Number of CLECs in St.P

Key foreign players: playing second roles • Deutsche Telekom – 40% shareholder (2nd largest) in MTS • Telenor – major investor in VimpelCom • Telia + Sonera – major investor in Megafon

Conclusion • Despite of worldwide economic and telecom turmoil, Russia for three last years is one of the most attractive markets • Telecommunications for both businesses and public are one of the basic needs for the success in current worldwide competition • Appearance of large and financially viable operators allowed to start sizeable long-term investments and projects • Russian private capital see telecom market as major source of cash and also as a vehicle for international ambitions • Foreign companies are cautious investors, playing secondary role and busy with their own problems at home