Understanding Linear Price-Quantity Demand Functions and Optimal Pricing Strategies

This guide explores the concept of linear price-quantity demand functions, demonstrating how to determine the optimal price by analyzing consumer willingness to pay and variable costs. Key insights from Paul Farris on pricing principles reveal the importance of balancing cost, value, and competition throughout the product life cycle. By using the methodology outlined, businesses can better understand pricing strategies and adapt to market demands, ensuring that pricing decisions align with overall strategic goals.

Understanding Linear Price-Quantity Demand Functions and Optimal Pricing Strategies

E N D

Presentation Transcript

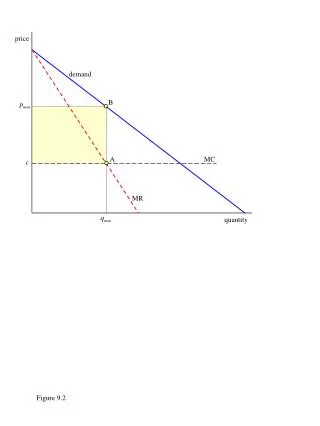

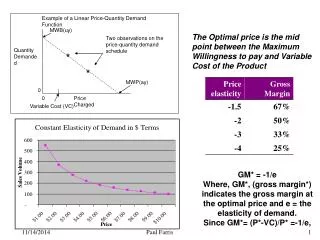

Example of a Linear Price-Quantity Demand Function MWB(uy) Two observations on the price-quantity demand schedule Quantity Demanded * * MWP(ay) 0 0 Price Charged Variable Cost (VC) The Optimal price is the mid point between the Maximum Willingness to pay and Variable Cost of the Product GM* = -1/e Where, GM*, (gross margin*) indicates the gross margin at the optimal price and e = the elasticity of demand. Since GM*= (P*-VC)/P* =-1/e, Paul Farris

Pricing Principles • Cost • Value • Competition Paul Farris

Product Life Cycle Clay Christensen • Features, technologies • Quality, reliability • Ease of use, convenience • Price Paul Farris

Summary • Cost, value, competition and sense of strategy over the product life cycle • One price will rarely do the job • Segmentation • Bundling • Selling through distributors • Pricing is a process that can be improved and innovated Paul Farris