Warm up Problem

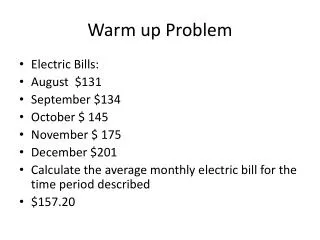

Warm up Problem. Electric Bills: August $131 September $134 October $ 145 November $ 175 December $201 Calculate the average monthly electric bill for the time period described $157.20. 3.1 , page 159 Homework review. 11 -$675 Mortgage

Warm up Problem

E N D

Presentation Transcript

Warm up Problem • Electric Bills: • August $131 • September $134 • October $ 145 • November $ 175 • December $201 • Calculate the average monthly electric bill for the time period described • $157.20

3.1 , page 159 Homework review • 11 -$675 Mortgage • 12- No, do not know monthly net income and no savings information is available • 13- $41 telephone • 14- $443.52 for transportation costs

Budgeting -Identify and examine current spending habits and identify the various expenses (difference between needs and wants) associated with living independently

Balance is essential for proper financial stability • Balance:

Key Terms Budget- a financial plan that compiles and compares a person’s income against all of his/her expenses in order to analyze spending and meet personal goals. Income- money coming into a budget (activity 1) Directions: Paper, pencil – fold hotdog style Income and expenses on either side. Examples- part-time job, stipends, allowances, gifts, interest, etc.

Where does your money go? • Expenses: Give me examples of each…. • Categories: Est. of US household expenses

Needs versus Wants • Needs are essential, wants are not • Expenses: Fixed versus Flexible • Fixed- rent, loan payment, insurance, etc. • Flexible – utility bill, groceries, clothing, etc. • Discretionary Spending (just flexible, not fixed)- spending money on things you want versus what you need to survive- candy, pop, snacks, movie tickets, late night pizzas, etc. • Too much (DS) can be a bad thing, control your excessive spending for a positive cash flow.

Cash Flow worksheet • A: Monthly Net Income= • B: Monthly Flexible Expenses = • C: Monthly Fixed Expenses= • Add B and C together = • A minus B = Total for saving and investing • When to save at the end of month or the beginning? • What if the bottom number is negative? Living beyond your means.

Net Worth • Net Worth = Assets – Liabilities • Assets = something you own that has positive economic value. Growing your assets has a positive net worth • Examples: savings, stocks, antiques, real estate, houses, etc. • Liabilities = something you owe, negative economic value, excessive liabilities can detract from your overall financial plan • Examples: loans, mortgages, auto and credit cards

Guide Practice • YOU Choose Fixed expense (FE), Variable expense (VE), Discretionary Spending (DS) • Magazine or cup of coffee • This Months rent • Dinner out • Cell Phone bill • School Books • Motorcycle Insurance payment • Monthly bus pass • Heating Bill

Continued • Frozen Pizza at grocery store • New pair of running shoes • Oil change for car • New mobile phone (old one still works) • New mobile phone (old isn’t working) • Personal Loan payment • Monthly deposit into savings

Written Assessment Exercise • Module 2 Handout • Groups of 6-7 people • List ideas and be prepared to present your budget to the class

Closure • What do you need to understand to help control excessive spending? • Quiz date- _____________