Leverage and Capital Structure: Maximizing Stockholder Wealth and Risk Mitigation

E N D

Presentation Transcript

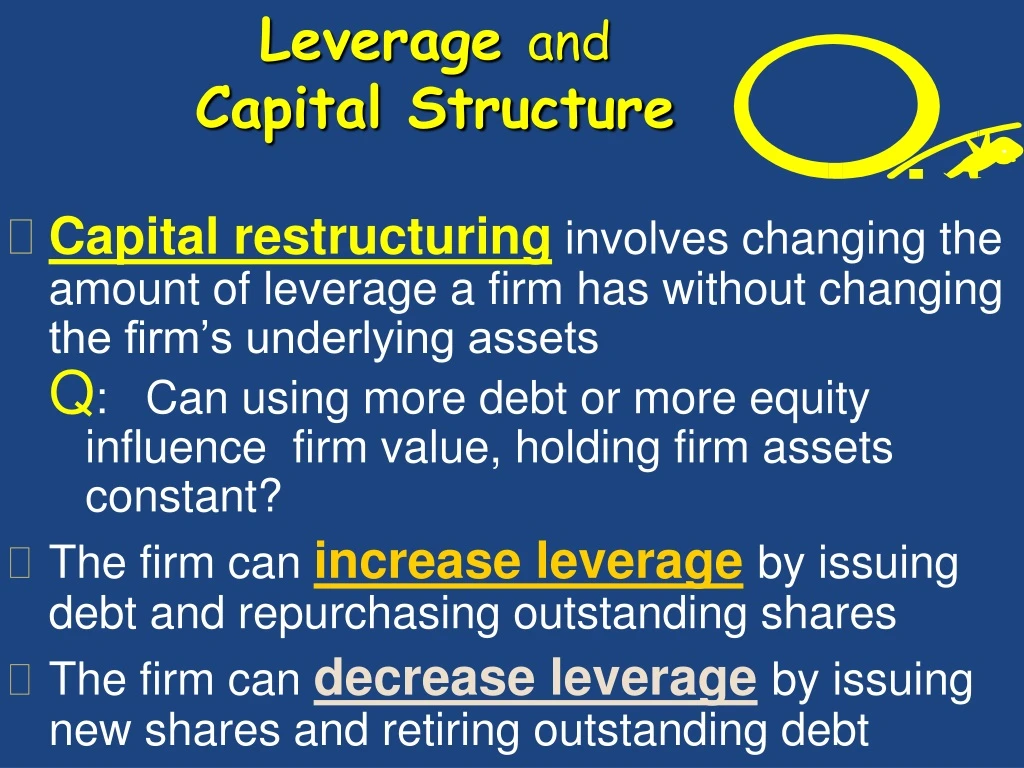

Leverage andCapital Structure • Capital restructuring involves changing the amount of leverage a firm has without changing the firm’s underlying assets • : Can using more debt or more equity influence firm value, holding firm assets constant? • The firm can increase leverageby issuing debt and repurchasing outstanding shares • The firm can decrease leverageby issuing new shares and retiring outstanding debt

Choosing a Capital Structure • What is the primary goal of financial managers? • To maximize stockholder wealth • We want to choose the capital structure that will maximize stockholder wealth • We can maximize stockholder wealth by: • maximizing the value of the firm, or • by minimizing the WACC

The Effect of Leverage • How does leverage affect the EPS and ROE of a firm? • When we increase the amount of debt financing, we increase the fixed interest expense • If we have a really good year, then we pay our fixed cost and we have more left over for our stockholders • If we have a really bad year, we still have to pay our fixed costs and we have less left over for our stockholders • Leverage amplifies the variation in both EPS and ROE

Leverage Effects Variability in ROE • Current: ROE ranges from 6.25% to 18.75% • Proposed: ROE ranges from 2.50% to 27.50% Variability in EPS • Current: EPS ranges from $1.25 to $3.75 • Proposed: EPS ranges from $0.50 to $5.50 The variability in both ROE and EPS increases when financial leverage is increased

If we expect EBIT to be greaterthan the break-even point, then leverage is beneficial to our stockholders • If we expect EBIT to be less than the break-even point, then leverage is detrimental to our stockholders Break-Even EBIT

Trans Am Corp Conclusions • The effect of leverage depends on EBIT When EBIT is higher, leverage is beneficial • Under the “Expected” scenario, leverage increases ROE and EPS • Shareholders are exposed to more risk with more leverage ROE and EPS more sensitive to changes in EBIT

Any stockholder who prefers leverage can create their own “homemade” and replicate the payoffs Accordingly, Trans Am’s capital structure should be irrelevant to shareholders HOMEMADE LEVERAGE

Capital Structure Theory Modigliani and Miller’s Theory of Capital Structure • Proposition I – firm value • Proposition II – WACC • The value of the firm is determined by the cash flows to the firm and the risk of the assets • Changing firm value • Change the risk of the cash flows • Change the cash flows Franco Modigliani

Capital Structure Theory Three Special Cases Case I – Assumptions No corporate or personal taxes No bankruptcy costs Case II – Assumptions Corporate taxes, but no personal taxes and no bankruptcy costs Case III – Assumptions Corporate taxes, but no personal taxes & Bankruptcy costs

M&M Case I – Propositions I and II Proposition I on firm Value • The value of the firm is NOT affected by changes in the capital structure • The cash flows of the firm do not change; therefore, value doesn’t change Proposition II on WACC • The WACC of the firm is NOT affected by capital structure It doesn’t matter how we divide our cash flows between our stockholders and bondholders, the cash flow of the firm doesn’t change.

Capital Structure in Case IProposition I Bottom line for CASE I:The size of the pie stays constant. =

Case I – Proposition IIBusiness & Financial Risk WACC = RA = (E/V) x RE + (D/V) x RD notice: no taxes here Rearrange to be: RE = RA + (RA – RD) x (D/E) RA = the “cost” of the firm’s business risk (i.e., the risk of the firm’s assets) (RA – RD)(D/E) = the “cost” of the firm’s financial risk (i.e., the additional return required by stockholders to compensate for the risk of leverage)

Graphical Demonstration of M&M Proposition II The change in the capital structure weights (E/V and D/V) is exactly offset by the change in the cost of equity (RE), so the WACC stays the same.

Capital Structure in Case I • Alternatively, in CASE I:Capital Structure Just Doesn’t Matter! https://www.youtube.com/watch?v=6UZvIZAHjlY Bill Murray in Meatballs – “It Just Doesn’t Matter” epic motivational speech.

Review Questions for Case I Data Required return on assets = 16%, cost of debt = 10%; percent of debt = 45% • What is the cost of equity? • RE = 16 + (16 - 10)(.45/.55) = 20.91% • Suppose instead that the cost of equity is 25%, what is the debt-to-equity ratio? • 25 = 16 + (16 - 10)(D/E) • D/E = (25 - 16) / (16 - 10) = 1.5 • Based on this information, what is the percent of equity in the firm? • E/V = 40%

Finding the Percentage of Equity • If D/E = 1.5, then D = 1.5 E. We know that V = D + E, so substituting for D, V = 1.5E + E = 2.5 E • When V = 2.5 E, then dividing both sides by V gives 1 = 2.5 E/V, or 1/2.5 = E/V = .40 or 40%. So Debt is 60%. NOTE ALSO: D / E = .60 / .40 = 1.5. ALTERNATIVE WAY: D/E = 1.5 = 3/2, so D is 3/(2+3) = 3/5 = 60% and E = 2/(2+3) = 2/5 = 40%.

An Optimal Capital Structure? • Case I – Assumes • No corporate or personal taxes • No bankruptcy costs • Case II – Assumes • Corporate taxes, but no personal taxes • No bankruptcy costs • Case III – Assumes • Corporate taxes, but no personal taxes • Bankruptcy costs

Case II – Corporate Taxes • Interest on debt is tax deductible • When a firm adds debt, it reduces taxes, all else equal • The reduction in taxes increases the cash flow of the firm where CFFA = EBIT + DEP - TAX Interest Tax Shield = $24 per year

Interest Tax Shield • Annual interest tax shield • Tax rate times interest expense • $1,000 in 8% debt = $80 in interest expense • Annual tax shield = .30($80) = $24 • Present value of annual interest tax shield • Assume perpetual debt, where D is Debt & TC is tax: PV = $24 / .08 = $300 • PV = D(RD)(TC) / RD = D*TC = $1,000(.30) = $300

Case II Value of the Firm Rises Figure 13.4

Bankruptcy Costs Direct costs • Legal and administrative costs • Enron = $1 billion; WorldCom = $600 million • Bondholders incur additional losses • Disincentive to use debt financing Financial distress • Significant problems meeting debt obligations • Most firms that experience financial distress do not ultimately file for bankruptcy Indirect bankruptcy costs • Assets lose value as management tries to avoid bankruptcy • HUGE COSTS: Lost sales, interrupted operations, loss of valuable employees, low morale, inability to purchase goods on credit • Stockholders wish to avoid a formal bankruptcy • Bondholders want to keep existing assets intact for collateral.

Case IIIWith Bankruptcy Costs D/E ratio → probability of bankruptcy probability → expected bankruptcy costs • At some point, the additional value of the interest tax shield will be offset by higher expected bankruptcy costs • At this point, the value of the firm will start to decrease and the WACC will start to increase as more debt is added

Figure 13.5 Optimal Capital Structure

Figure 13.6 Highest Value is also at the Lowest WACC.

Conclusions Case I – no taxes or bankruptcy costs • No optimal capital structure Case II – corporate taxes but no bankruptcy costs • Optimal capital structure = 100% debt • Each additional dollar of debt increases the cash flow of the firm Case III – corporate taxes and bankruptcy costs • Optimal capital structure is part debt and part equity • Occurs where the benefit from an additional dollar of debt is just offset by the increase in expected bankruptcy costs

Additional Managerial Recommendations Taxes • The tax benefit is only important if the firm has a large tax liability • The higher tax rate → the greater incentive there is to use debt Risk of financial distress • The greater the risk of financial distress, the less debt will be optimal for the firm • The cost of financial distress varies across firms and industries • Oriental rug dealers versusfinancial institutions are impacted differentially by bankruptcy or financial distress

Problem • Assuming perpetual cash flows in Case II Proposition I, what is the value of equityfor a firm with EBIT = $50 million, Tax rate = 40%, Debt = $100 million, cost of debt = 9%, and unlevered cost of capital = 12%? • VU = $50 million (1 - .4) / .12 = $250 million • VL = $250 million + $100 million (.4) = $290 million • E = VL – Debt = $290 million - $100 million = $190 million

Results from this problemrelating to capital structure • If you owned the whole firm with no debt, it is worth $250 million. • If you ask your firm to borrow $100 million, the firm is worth $290 million. • You just made a cool $40 million!