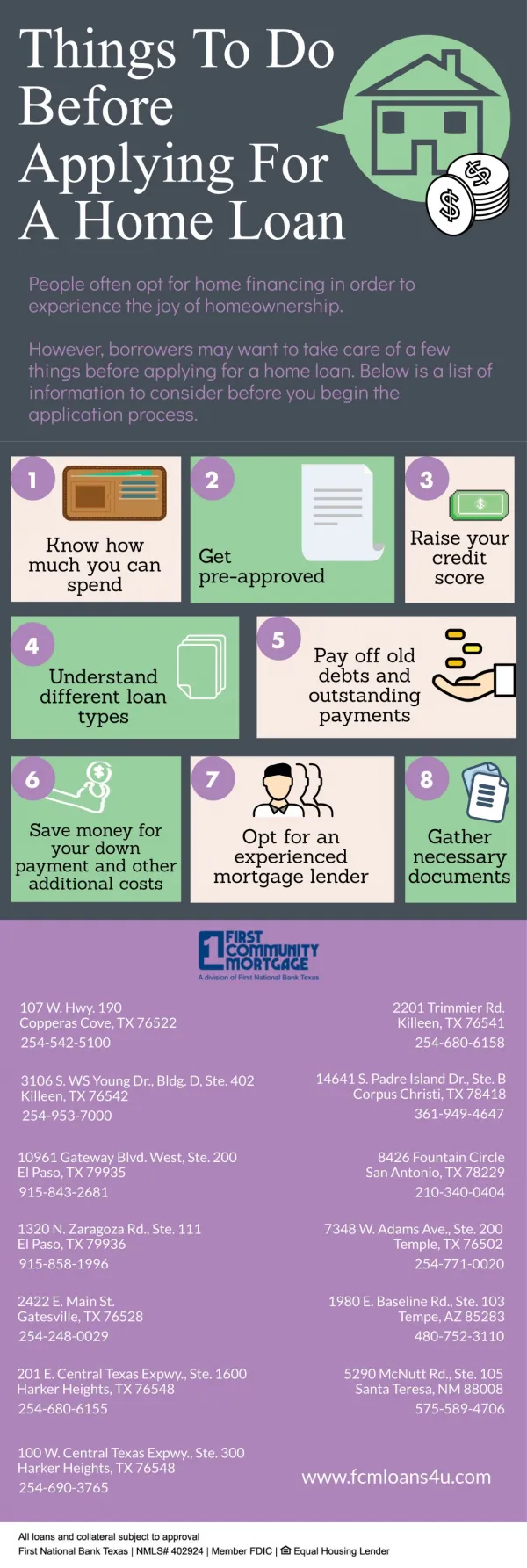

Know These Terms Before Applying For A Home Loan

20 likes | 64 Vues

When you are making an important financial decision in life like, buying a home, take it after a due diligence, backed by research and planning. Check the must to know terms before applying for a home loan.

Know These Terms Before Applying For A Home Loan

E N D

Presentation Transcript

KnowTheseTermsBeforeApplyingForAHomeLoan KnowTheseTermsBeforeApplyingForAHomeLoan When you are making an important financial decision in life like, buying a home, take it after a due diligence, backed by research and planning. Check the must to know termsbeforeapplyingforahomeloan. Downpayment: If the amount that the buyer has to pay from his or her pocket, which will not be sanctioned by the bank. Bank sanctions only 80% of the property value and the rest 20%shouldbepaidbythebuyer. Rateofinterest,types: Two types of interest rates are fixed rate or floating rate. In fixed rate type, your interest remains fixed for the entire loan-period, whereas the floating rate varies according to the market conditions. So one pays an unchanged rate of interest with thefixedrate.Floatingrateallowsyoutopaylessattimeswheremarketsfluctuate. Sanctionletter: It is the confirmation for the eligibility of the home loan, but does not guarantee disbursement. The letter will have loan amount, loan period, interest rate, EMI (equatedmonthlyincome)amount,etc.

Disbursementmodes: After the verification of the legal documents, the loan amount would be released in three ways or modes: full, partial and advance. When the total loan amount is released, it is called full disbursement. In case of the partial disbursement, the loan amountisreleasedinpartsaccordingtotheprogressinconstruction. EMI: Repayment of the loan to the bank on monthly-basis is called EMI. It depends on the principal amount, interest rate, compounding interest, etc. EMIs begin after the loan disbursal.Itisinverselyproportionaltotheloantenure. Post-datedcheques(PDC): The borrower has to issue PDCs for a stipulated period for the EMI payments at the time of final disbursement. These are collected as one may need to pay extra EMI withtheextensionoftheproject. If you are applying for a home loan for the first time chances are that you may encounter a few problems. Get a thorough knowledge about the terms, policies, procedures, etc. before applying for a home loan to take well-informed decisions. For more information and expert advice on personal finance, approach ArthaYantra - World’sfull-serviceRobo-advisory.