Hazard Risk

Hazard Risk. Chapter 3. Hazard Risk Defined. No universal definition, but typically described as Pure Risk The type of risk that may result in only a negative outcome Three categories: Personnel risk – uncertainty related to losses to a firm due to death or incapacity of key employee;

Hazard Risk

E N D

Presentation Transcript

Hazard Risk Chapter 3

Hazard Risk Defined • No universal definition, but typically described as Pure Risk • The type of risk that may result in only a negative outcome • Three categories: • Personnel risk – uncertainty related to losses to a firm due to death or incapacity of key employee; • Property risk – uncertainty related to loss of wealth due to damage to property; • Liability risk – uncertainty related to the financial responsibility from injury or damages to third party

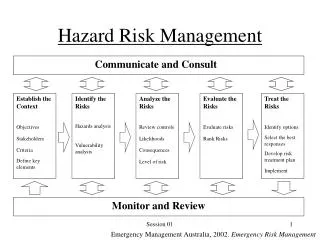

Measuring Hazard Risk • It is very important to categorize risks to analyze them accurately. • Measuring the Frequency and the severity of the potential loss • Loss Prevention reduces the frequency of losses • Loss reduction reduces the severity of a loss

Risk Management Techniques • Avoidance – Reduce the probability of loss to zero • Separation – disperse a particular activities over several locations • Duplication – involves relying on backup copies, etc., if primary asset is lost • Diversification – involves providing a range of products to be used by a variety of customers • Risk Control • Hazard Reduction • Loss Reduction • Transferring of Risk • Insurance, hedging or other transfer mechanism

How is Insurance Involved with RM? • Insurance is only one of several risk management techniques; • Insurance is a device for sharing, transferring, and reducing risk that combines a sufficient number of exposure units to make individual losses collectively predictable.

Insurance Terminology • Peril – the cause of a loss • Hazard – a condition that causes a peril; • A condition that increases the frequency or severity of a loss; • Four types: • Physical – a tangible characteristic that impacts the frequency or severity • Morale – carelessness or indifference to a loss • Moral – intentionally causing or exaggerating a loss • Legal – a condition in the legal environment that impacts the frequency or severity of a loss • Liability – a legally enforceable obligation to pay damages to a third party

Types of Loss Exposures • Property Loss Exposures • Liability Loss Exposures • Personnel Loss Exposures • Net Income Loss Exposures • Must also consider (not listed in this chapter) • Management Liability Exposures • Corporate Governance Liability Exposures

Three Ways to Examine Losses:Elements of Loss Exposures • Asset Exposes to Loss • Cause of Loss • Financial Consequences of Loss

Property Assets Exposed to Loss • Tangible property • Real Property • Personal Property • Intangible Property

Property Causes of Loss • Physical Perils • Natural • Human • Economic

Financial Consequences of loss • Loss of Use • Loss of income derived from the property • Extra expenses incurred to continue operations • Example in personal scenario: Extra living expenses • May be total or partial • May be temporary or permanent

Liability Exposures • Asset exposed - the financial payment that must be made including: • Economic and Non-economic damages • Settlement costs • Litigation costs • Legal fees • Cause of loss – filing of claim or notice of lawsuit • Financial Consequences of Loss • Potentially unlimited or limited to the assets or earnings potential of the organization or person

Personnel Loss Exposures • Asset Exposed to Loss – the value a person adds to a organization • Cause of Loss – the loss of the person’s contribution through • Death • Disability • Retirement • Voluntary separation including resignation • Involuntary separation, including firing or layoff • Financial consequences of Loss • Contingent on wither permanent or temporary, total or partial (death or disability)

Net Income Loss Exposures • Asset Exposed – the future cash flows into the entity • Cause of loss – the outcome that may cause a decline in the potential future cash inflows: • Damage to property • Liability losses • Personnel Losses • Business risk such as losing market share, loss of good will, failure to anticipate growth potential or failure of product to perform or failure of contractor to perform as scheduled. • Financial Consequences of Loss – degree of loss varies by cause of loss but may involve • A decline in revenues • An increase in expenses • Both a decline in revenues and an increases in expenses

Classification of Commercial Insurance (Table on p. 3.17) • Property Coverage • Commercial Property – Building and Personal Property (BPP) • Business Income - called Consequential Loss insurance, also called time element coverage and business interruption coverage; covers loss of income and extra expenses. • Key Terms • Monoline vs.. package policy (e.g., fire vs. package commercial package policy) • Named perils vs. all-risks (now called direct physical loss coverage) • Replacement cost vs. actual cash value • Insurance-to-value provisions with coinsurance provision • E.g.., 80% coinsurance clause on homeowners policy • Industrial All-risk (Special Risk) policies – perils and coverages are tailored to individual needs

Commercial Coverage (cont.) • Builders’ Risk coverage – unique risk of buildings under construction • Limits increase as project progresses • Addresses the myriad of different insurable interests involved in buildings under construction such as • Building owner • Contractor • Subcontractor • Provides additional coverage for unique perils such as increased likelihood of theft, windstorm and fire to materials left in the open • E.g., copper wiring - http://articles.latimes.com/2013/aug/18/local/la-me-0819-copper-thefts-20130819 • Equipment Breakdown coverage, including Boiler and Machinery, electrical and mechanical equipment • Fidelity and Crime Insurance – for perils such as employee dishonesty, computer fraud, extortion, forgery, theft and robbery

Commercial Coverage (cont.) • Surety Bonds – guarantees to one party (the obligee) that the principal will fulfill an obligation or promise to perform • Different from insurance in that surety bonds are three-party agreements involving a principal, surety, and an obligee; • Surety is answerable to the obligee if the principal defaults; surety does not expect a loss. • Insurer is responsible to the insured; insurer expects losses in aggregate

General Liability Insurance • Provides coverage when the insured becomes legally obligated to pay damages • The insured may become legally obligated to pay damages due to a legal wrong for which the civil law provides a remedy in the form of damages. • Key terms: • Tort – a wrong or wrongful act or an omission, other than a crime or a breach of contract, that invades a legally protected right; • Indemnify – to return someone to a pre-loss condition • Occurrence (vs. accident) – a continuous or repeated exposure to harmful conditions; liability policies also include an accident which is a sudden, unexpected event; • Claims-made Form – coverage for damages that are claimed during the policy period • http://www.irmi.com/online/insurance-glossary/terms/c/claims-made-policy.aspx • Asbestos • http://www.asbestos.com/legislation/history.php

Commercial Coverage (cont.) • Commercial Auto – may provide liability and property coverage for business-owned vehicles • Workers Compensation – provides for the cost of medical care and rehabilitation for injured workers and lost wages and death benefits for dependents of persons killed in work-related accidents (III Fact Book 2013) • WC systems and benefits vary by state • History of Workers Compensation - http://www.ncbi.nlm.nih.gov/pmc/articles/PMC1888620/ • Employers Liability – provides coverage when employees are allowed to sue employers for a situation that is outside the scope of WC or in a dual role as employer as well as manufacturer of product that caused damage, then employee may seek damages under employers liability • Professional Liability or E and O – coverage for failure to perform a professional duty or to conform to appropriate standards (typically excluded under GL policies)

Management Liability Policies • Directors and Officers Liability – covers directors and officers of a company for negligent acts or omissions and for misleading statements that result in suits against the company • There are numerous forms of D and O coverage (see III Fact Book, p. 185) • Timeline of D and O coverage - http://www.mynewmarkets.com/articles/181645/do-timeline • Employment Practices Liability (EPL) – losses from laws that protect employees against discrimination, sexual harassment, unfair wage practices, and other prohibited employer practices • May be purchased either as a stand-alone EPL policy or endorsed onto the D and O policy; (III FACT book, p. 187) • Fiduciary Liability - covers fiduciaries of an employee benefit plan against liability claims alleging breach of their fiduciary duties involving discretionary judgment

Miscellaneous Commercial Coverage • Aircraft Insurance – specialized coverage that requires expertise to underwrite; somewhat unique in that it may be: • Potentially catastrophic – if high concentration of key employees in one plane or if plane crashes into highly concentrated area http://news.google.com/newspapers?nid=1842&dat=19911212&id=4U4gAAAAIBAJ&sjid=0McEAAAAIBAJ&pg=5903,1773128 • Limited spread of risk – most companies who have Commercial Insurance do not have their own plane • Ocean marine – to cover the vessel, liability and cargo • Environmental Insurance – the need is obvious after several oil spills in recent history; • Was Exxon Valdez the largest? • http://www.mnn.com/earth-matters/wilderness-resources/stories/the-13-largest-oil-spills-in-history