Download

1 / 13

130 likes | 420 Vues

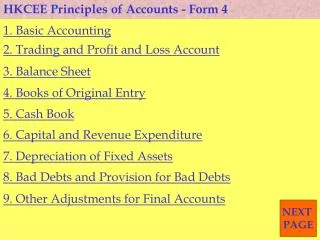

HKCEE Principles of Accounts - Form 4. 1. Basic Accounting. 2. Trading and Profit and Loss Account. 3. Balance Sheet. 4. Books of Original Entry. 5. Cash Book. 6. Capital and Revenue Expenditure. 7. Depreciation of Fixed Assets. 8. Bad Debts and Provision for Bad Debts.

E N D

HKCEE Principles of Accounts - Form 4 1. Basic Accounting 2. Trading and Profit and Loss Account 3. Balance Sheet 4. Books of Original Entry 5. Cash Book 6. Capital and Revenue Expenditure 7. Depreciation of Fixed Assets 8. Bad Debts and Provision for Bad Debts 9. Other Adjustments for Final Accounts NEXT PAGE

HKCEE Principles of Accounts - Form 4 10. Bank Reconciliation Statements 11. Errors and Suspense Accounts 12. Control Accounts 13. Incomplete Records - Final Accounts 14. Incomplete Records - Stock Valuation 15. Income and Expenditure Accounts 16. Manufacturing Accounts EXIT

HKCEE Principles of Accounts - Form 5 1. Accounting Ratios 2. Accounting Concepts and Conventions 3. Partnership Accounts - Final Accounts 4. Partnership Accounts - Goodwill 5. Partnership Accounts - Revaluation 6. Partnership Accounts - Realization/Dissolution 7. Company Accounts - Final Accounts 8. Company Accounts - Issue of Shares 9. Incomplete Records - Cash Shortage EXIT

I. Why? The bank balance as per cash book may not be equal to the bank balance as per bank statement at the month end because of time lag in depositing receipts or autopay service from the bank. A Bank Reconciliation statement (BRS) can provide an arithmetical proof to show the reasons for the difference.

II. How? 1. No adjustments are made in bank balance in cash book