Download

1 / 4

40 likes | 201 Vues

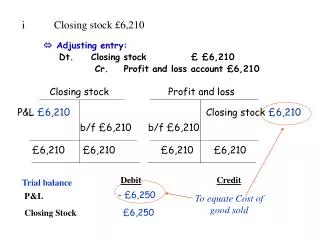

This entry details the adjustment process for closing stock and prepaid insurance as part of the financial accounting cycle. The closing stock is recorded at £6,210, impacting the profit and loss statement. Additionally, an entry for prepaid insurance is made to adjust for a £60 prepaid policy, affecting cash and insurance accounts. Both adjustments ensure the accuracy of the trial balance and provide a clearer financial picture for Family Health Care following its patient fee earnings of RM5,500 during the month.

E N D

i Closing stock £6,210 • Adjusting entry: • Dt. Closing stock £ £6,210 • Cr. Profit and loss account £6,210 Closing stock Profit and loss P&L£6,210 Closing stock £6,210 b/f £6,210 b/f £6,210 £6,210 £6,210 £6,210 £6,210 DebitCredit P&L Trial balance - £6,250 To equate Cost of good sold Closing Stock £6,250

ii £60 of insurance is prepaid Adjusting entry: Dt Prepaid Insurance xx Cr Insurance xx Insurance Prepaid Insurance Cash/Bank £860 Prepaid Ins £60 Insurance £60 b/f £60 b/f £800 £60 £860 £860 £60 DebitCredit Insurance£860 Trial balance £60 New Balance Prepaid Insurance - £60 = £800

e. During the first month Family Health Care earns patient fees of RM5,500 in cash. Assets = liability + Owner equity Cash Land Equipt. = Note + Capital earning Payable stock Bal. 9,000 12,000 5,000 = 20,000 6,000 e. 5,500 5,500 fees Bal. 14,500 12,000 5,000 = 20,000 6,000 5,500