Download

1 / 1

10 likes | 173 Vues

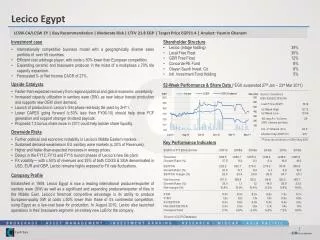

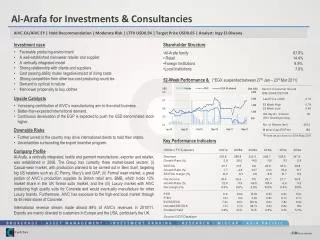

Al- Arafa for Investments & Consultancies. AIVC.CA/AIVC EY | Hold Recommendation | Moderate Risk | LTFV USD0.94 | Target Price USD0.65 | Analyst: Ingy El- Diwany. Investment case Favorable producing environment A well-established menswear retailer and supplier A vertically integrated model

E N D

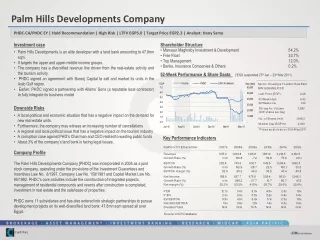

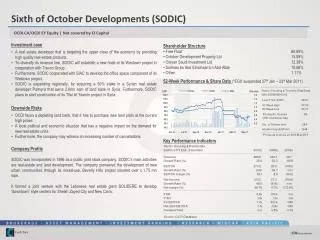

Al-Arafa for Investments & Consultancies AIVC.CA/AIVC EY | Hold Recommendation | Moderate Risk | LTFV USD0.94 | Target Price USD0.65 | Analyst: Ingy El-Diwany • Investment case • Favorable producing environment • A well-established menswear retailer and supplier • A vertically integrated model • Strong relationship with clients and suppliers • Cost passing ability mutes negative impact of rising costs • Strong competition from other low-cost producing countries • Demand is cyclical in nature • Men lower propensity to buy clothes • Upside Catalysts • Increasing contribution of AIVC’s manufacturing arm to the retail business. • Better-than-expected international demand. • Continuous devaluation of the EGP is expected to push the USD denominated stock higher. • Downside Risks • Further unrest in the country may drive international clients to hold their orders. • Uncertainties surrounding the export incentive program. • Shareholder Structure • Al-Arafa family 67.9% • Retail 14.4% • Foreign Institutions 9.9% • Local Institutions 7.8% • 52-Week Performance & (*EGX suspended between 27th Jan – 23rd Mar 2011) Key Performance Indicators Company Profile Al-Arafa, a vertically integrated, textile and garment manufacturer, exporter and retailer, was established in 2006. The Group has currently three market-based sectors: (i) Casual-wear market, with production planned to be carried out in BeniSuef, targeting big US retailers such as JC Penny, Macy’s and GAP, (ii) Formal wear market, a great portion of AIVC’s production supplies its British retail arm, BMB, which holds 12% market share in the UK formal suits market, and the (iii) Luxury market with AIVC producing high quality suits for Concrete and would eventually manufacture for other Luxury brands. Furthermore, AIVC has exposure to the high-end local market through its 45 retail stores of Concrete. International revenue stream made almost 89% of AIVC’s revenues in 2010/11. Exports are mainly directed to customers in Europe and the USA, particularly the UK.