Accounting Approaches for Incomplete Records

120 likes | 450 Vues

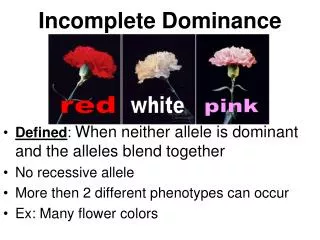

Learn about Net Assets Approach and Balancing Figure Approach to prepare financial statements from incomplete records. Understand Mark Up and Margin concepts in the process.

Accounting Approaches for Incomplete Records

E N D

Presentation Transcript

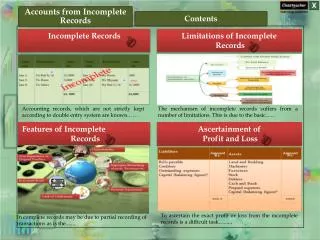

Where the accountant has to create a set of Financial Statements from Incomplete Records • 3 situations giving rise to Incomplete Records • No Accounting records kept at all for the Year in Question (Net Assets approach will be used – Accounting Equation!!) • Some Accounting information is Missing (Balancing Figure Approach will be used – T Account) • Records have been lost due to fire or flood – Accountant to prepare FS from whatever is left

2 Main Approaches • Net Assets Approach (i.e. Accounting Equation Approach) • Balancing Figure Approach (T Account Approach) – This is the method that students should be most familiar with for exam questions

Net Assets Approach • Use of Accounting Equation to Determine figure for Opening/Closing Capital; Drawings; Profit/Loss for the Year • Assets = Capital + Liabilities

The Balancing Figure (Double Entry/T A/c ) Approach • The Balancing figure approach uses ledger accounts to determine the incomplete information as detailed below • Receivables T Account – Credit Sales; Money Received • Payables T Account – Credit Purchases; Money Paid • Cash at Bank T A/C – Drawings, Money Stolen • Cash in Hand T A/c – Cash Sales, Cash Stolen • The process involves setting up a T Account and inserting the information that we have in the question to determine the missing figures

Mark Up & Margin Summary Both Mark Up & Margin involve expressing profit against • “Cost” for Mark Up • “Selling Price” for Margin So a product that sells for €20, costs €16 to produce and makes a profit of €4….the mark up is 25% (€4/€16) and the margin is 20% (€4/€20)

Margin & Mark Up Concepts • A margin is calculated on Selling Price (i.e. Selling Price is 100%) – • A Mark up is calculated on Cost (i.e. Cost is 100%) -

To Find Margin when Mark up is Known and Vice Versa, • Mark Up is Known – How to Find the Margin? • Add One to the Denominator (number beneath the Line) • Margin is Known – How to find the Mark Up? • Subtract One from the Denominator (number beneath the line)