Download

1 / 21

210 likes | 478 Vues

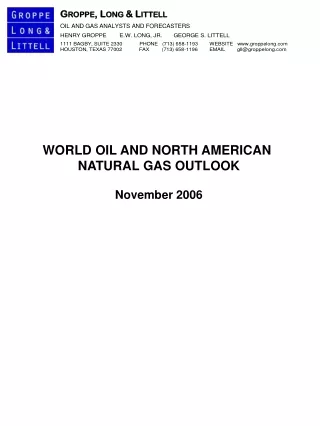

WORLD OIL AND NORTH AMERICAN NATURAL GAS OUTLOOK November 2006. 1. PETROLEUM INDUSTRY FUNDAMENTALS. Depletion is relentless. Explorationists seek largest and most profitable deposits first. Production rises initially, peaks and irreversibly declines.

E N D

WORLD OIL AND NORTH AMERICAN NATURAL GAS OUTLOOK November 2006

1 PETROLEUM INDUSTRY FUNDAMENTALS • Depletion is relentless. • Explorationists seek largest and most profitable deposits first. • Production rises initially, peaks and irreversibly declines. • United States crude oil production rose 50 percent from 1945 to 1970, peaked and declined almost 50 percent since.

2 OIL SUMMARY CONCLUSIONS • World crude oil production is peaking and will decline irreversibly. • Security and stability concerns are growing in exporting countries – Saudi Arabia, Russia, Venezuela, Iraq, Iran, Nigeria – which account for over 40 percent of world crude oil supply. • Liquids from the growing international natural gas industry will supplement crude oil supplies. • High prices are required to constrain consumption. There is no such thing as scarcity and no such thing as surplus. There is only price. • 100,000 barrel per day supply change moves the price $1 per barrel. • Transportation is the dominant growing use for oil. • High cost oil will be replaced with cheaper natural gas and other substitutes in stationary fuel use in developing economies as occurred in OECD countries in the last oil crisis. • The world oil industry will continue to operate essentially at capacity with permanent major price volatility.

3 GAS SUMMARY CONCLUSIONS • North American natural gas production has already peaked. • LNG imports will grow. • Canadian imports will decline. • Total supply will decline. • High prices will drive substitution of lower cost fuels in industrial and power generation use. • Nuclear power expansion is the logical long-term solution.

Petroleum Natural Gas Coal Renewables Nuclear 25% 23% 21% 18% 31% Petroleum Petroleum 38% 41% United States % of World Population 6% Natural Gas Natural Gas 23% 24% Coal Coal 22% 24% Renewables Renewables 8% 6% Nuclear Nuclear 8% 6% 4 WORLD AND UNITED STATES ENERGY CONSUMPTION 2003 Million Barrels Per Day Oil Equivalent United States % of World Energy Consumption World United States

Billion Barrels Annual Discovery Annual Production 5 WORLD CRUDE OIL DISCOVERY RATES

UNITED STATES CRUDE OIL DISCOVERY RATE Lower 48 States Onshore Billion Barrels Annual Discovery Annual Production Oil fields larger than 100 million barrels 6

2004 $ Per Barrel Era of Plenty & U.S. Control Era of Transition & OPEC Control Era of Scarcity & Price Rationing Price? U.S. Production Peaked World Production Peaking $36 Average $13 Average 1870 1970 2004 2030 7 CRUDE OIL PRICE WTI Or Equivalent

Million Barrels Per Day $/Barrel Actual Forecast Production (Left Scale) Arabian Light Price (Right Scale) 8 WORLD CRUDE OIL PRODUCTION

Million Barrels Per Day Actual Forecast EIA Forecast 80.2 78.0 Other * 75.6 68.7 NGL ** 62.7 OPEC Crude Oil 39.9 36.0 Eastern Europe Crude Oil 25.5 28.9 Other Non-OPEC Crude Oil * alcohols, coal liquefaction, and gas to liquids ** condensate, natural gasoline, butanes, propane, and ethane 9 WORLD PETROLEUM PRODUCTION

Percent of Global Gross Domestic Product OIL EXPENDITURES Crises of 1970’s & 1980’s Current at $60 per Barrel Oil 10 OIL EXPENDITURES RELATIVE TO GLOBAL ECONOMIC ACTIVITY

Million Barrels Per Day United States World Transportation 51% Residential & Commercial 10% Raw Material 12% Transportation 67% Industrial & Power 27% Residential & Commercial 7% Raw Material 16% Industrial & Power 10% 11 WORLD PETROLEUM USE BY SECTOR

Consumption Production 12 UNITED STATES PETROLEUM PRODUCTION AND CONSUMPTION Million Barrels Per Day

13 OIL AND GAS IMPORT COST Billions of Dollars

14 CHINA & INDIA PROJECTED ECONOMIC GROWTH Cumulative Percent 8% per yr

15 ENERGY COST ENERGY CONSUMED FOR ENERGY PRODUCTION Energy Consumed Percent Of Gross Energy Input Ethanol From Corn Gas to Liquids Oil From Oil Sands Oil 1985 LNG Oil 1970

Billion Cubic Feet Per Day $/MMBTU Actual Forecast Consumption Imports & Other Production LNG Average Wellhead Price (Right Scale) 16 U.S. NATURAL GAS CONSUMPTION, PRODUCTION AND PRICE

Actual Forecast Price Controls Section 29 Tax Credits 17 UNITED STATES NATURAL GAS PRODUCTION Bcfd Onshore Lower 48 Conventional (Non-Associated) Offshore Tight Associated Coalbed Canadian Imports LNG

18 UNITED STATES NATURAL GAS DRILLING AND PRODUCTION Average Wellhead Price $/MMBTU Gas Production Bcfd Gas Well Completions Total Production Well Completions Average Wellhead Price

Average First Year Production Per New Well - Mcfd 19 UNITED STATES NATURAL GAS DRILLING PRODUCTIVITY

Bcf/d $/MMBTU Actual Forecast 60.8 59.6 Boiler Fuel & Other 46.9 42.0 Fuel Use Act 21.7 Residential & Commercial 24.3 Average Wellhead Price (Right Scale) 20 UNITED STATES NATURAL GAS CONSUMPTION Billion Cubic Feet Per Day