Download

1 / 14

140 likes | 368 Vues

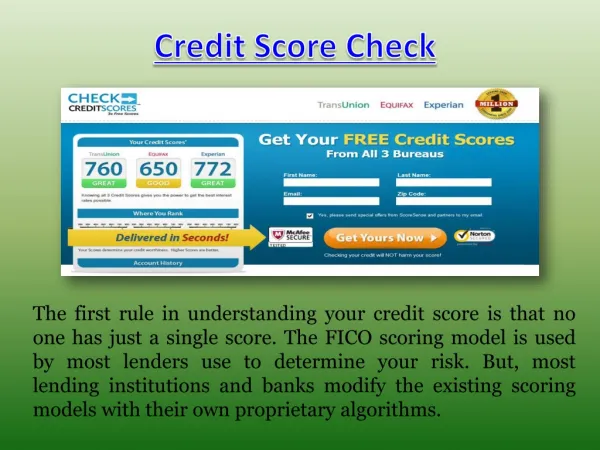

There can always be a high number of different people that when it comes time to ever borrow money, they just might not know exactly what they have available as borrowing options.

E N D

Not only this but also a huge number of complaints were received where the customers did not get a loan and still their bank accounts were charged with heavy fees. number of complaints

The interest rates charged on payday loans cannot exceed 0.8% per day. This brings down the overall APR and limits the ability of payday lenders to overcharge their borrowers. Interest rate

Historically many lenders, like the famed Wonga, charged interest rates exceeding 5,000% APR on these payday loan lenders. At no point in our country’s history such heavy interest rates were seen. charged interest

Many borrowers who could not pay the loans on the requisite date ended up ratcheting up huge default charges which would take the repayable amount to astronomical size. Total repayment

When the payday loans were available in the mass market their strongest point touted to prospective customers was their ease of processing and repayment. prospective customers

On 2nd January, 2015 new regulations regarding the payday industry came into effect. They have put a ceiling on the interest, default charges and maximum repayable amount for payday loans. regulations regarding

The biggest setback from these regulations would be to direct payday lenders. Such a regulation was inevitable given the huge number of people affected by payday loans and the increasing pressure on the government to rein this sector of the financial markets. The biggest setback

This led to some borrowers getting burdened with thousands of pounds of debt when they had borrowed £100 or £200. Many influential sections of society came out in open opposition to the payday lending. thousands of pounds

However within the payday industry the borrowers overlooked this factor as the initial principal loan was small and the primary driving factor was securing the finance. securing the finance

There are several firms in the market, like True Blue Loans, which not only give the borrowers adequate advice but provide them with the option to repay in 3 to 6 months. True Blue Loans

This is true for almost all the remaining direct lenders. Many have even closed their shops knowing that they cannot work with lower margins. cannot work with lower margins

It also ensured that this problem was tackled head on before it became too big and lead to any loss of the taxpayer’s money. The heydays of payday lending are definitely past us and we should see a new beginning of prudent and responsible lending from short term lending businesses. the taxpayer’s money

Thanks for watching More Information:- http://www.bfwggrants.co.uk/