Download

1 / 29

290 likes | 470 Vues

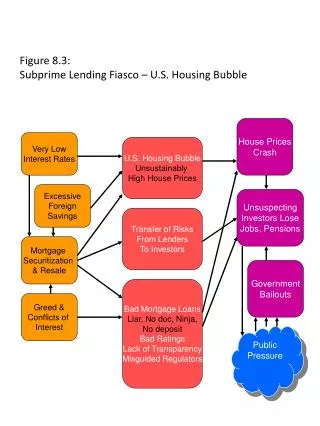

Subprime Lending Litigation: Insurance Recoveries. David P. Schack Partner, Los Angeles . What is the Subprime Crisis? . Increased delinquencies, defaults and foreclosures Inability to make new loans to “subprime borrowers” Contraction of mortgage finance industry Margin Calls

E N D

Subprime Lending Litigation: Insurance Recoveries David P. Schack Partner, Los Angeles

What is the Subprime Crisis? • Increased delinquencies, defaults and foreclosures • Inability to make new loans to “subprime borrowers” • Contraction of mortgage finance industry • Margin Calls • Change in price for loans or no secondary market for loans • Bankruptcy of lenders and conduits • Credit crunch • Losses for all participants

Who are the Participants? • Borrowers • Mortgage brokers • Mortgage lenders • Conduits

Who are the Participants? (continued) • Servicers • Issuers • Rating agencies • Investors of whole loans • Underwriters

Who are the Participants? (continued) • Purchasers of mortgage backed securities (individuals, lenders, brokers, private equity funds, hedge funds, mutual funds, pension funds, insurance companies) • Insurers • Credit enhancers

What are the Actions? • Administrative enforcement actions • Consumer class actions • Individual consumer actions • “Commercial” disputes between industry participants

Administrative Enforcement Actions • State Attorneys General • FTC • DOJ • Federal banking agencies • State banking and consumer credit departments • SEC

Consumer Class Actions • Shareholder suits for alleged violations of securities laws • Unfair and deceptive lending practices • Option ARM loan cases (including claims under TILA) • Discriminatory lending practices (claims under ECOA/FHA) • Advertising practices (FCRA firm offer on credit cases) • Servicing practices

Individual Consumer Actions • Predatory lending • Wrongful lending • Fraud • Option ARM loans • Appraisal practices

Types of Policies That May Be Implicated In Subprime Lending Litigation • Directors and Officers Liability Insurance ((“D&O”) • Errors & Omissions Liability Insurance (“E&O”) • Commercial General Liability Insurance (“CGL”) • Mortgage Bankers Bond

D&O Coverage • PART A: • The Company shall pay, on behalf of the Insured Persons, Loss for which the Insured Person is not indemnified by the Organization and which the Insured Person becomes legally obligated to pay on account of any Claim first made against the Insured Person during the Policy Period for a Wrongful Act. • PART B: • The Company shall pay, on behalf of the Organization, Loss for which the Organization grants indemnification to an Insured Person, as permitted or required by law, and which the Insured Person becomes legally obligated to pay on account of any Claim first made against the Insured Person during the Policy Period for a Wrongful Act. • PART C: • The Company shall pay, on behalf of the Organization, Loss which the Organization becomes legally obligated to pay on account of any Securities Claim first made against the Organization during the Policy Period for a Wrongful Act.

Private Company D&O Insurance Coverage • Part C—“Entity Coverage”—may be expanded to cover all “Claims” as defined by Policy. • Part C coverage may not be limited “Securities Claims.”

Definition of “Wrongful Act” Wrongful Act means: (a) any error, misstatement, misleading statement, act, omission, neglect, or breach of duty committed, attempted, or allegedly committed or attempted by an Insured Person in his or her Insured Capacity, or for purposes of coverage under Part C, by the Organization; or (b) any other matter claimed against an Insured Person solely by reason of his or her serving in an Insured Capacity.

Potential Subprime Mortgage Claims That May Trigger D&O Insurance Coverage • Investigations by SEC, Attorneys General or other governmental agencies. • Investor lawsuits alleging omissions or misrepresentations relating subprime mortgage problems. • Claims or actions by employees relating to investments in subprime mortgages by the company in connection with retirement plans/401k’s. • Claims or actions by borrowers against directors/officers (or entities under private D&O insurance) for allegedly improper lending activities.

Definition of Claim Claim means: (a) a written demand for monetary damages or non-monetary relief; (b) a civil proceeding commenced by the service of a complaint or similar pleading; (c) a formal civil administrative proceeding commenced by the filing of a notice of charges or similar document or by entry of a formal order of investigation or similar document; or (d) a criminal proceeding commenced by the return of an indictment against an Insured Person or the Organization under Part C for a Wrongful Act.

Key Issues Under Definition of Claim • “formal” vs. “informal” investigation • Expand to include “subpoenas” and “target” letters • Expand to include “investigations” without limitations

Definition of Loss • Loss means the amount the Insured Person (for purposes of Part A and B) or the Organization (for purposes of Part C) becomes legally obligated to pay on account of any covered Claim, including but no limited to damages, judgments, settlements, pre-judgment and post-judgment interest and Defense Costs. • Typically “Loss” will not include punitive damages, taxes, fines, penalty and the multiplied portions of damage awards. To the extent these items are insurable, they may be included by negotiation. Restitution may not be insurable.

Potentially Applicable D&O Exclusions • Fraudulent/dishonest conduct • Personal profit • Known claims

Other Issues • Claims made feature of policies • Self-liquidating feature of policies • Notice of facts and circumstances that may give rise to a claim • Problems arising from settlement without consent • Need for early notice

E&O Overview • Overview of E&O Terms • Differences between E&O and D&O • Potential Claims that May Trigger E&O Coverage • Potential Defenses

What is E&O Coverage? • E&O is the “general rubric” used to describe many types of insurance that protect persons or entities that render “professional services” for liabilities arising from errors or omissions committed while rendering such services, usually for a fee or commission. • Terms vary widely by industry and often are narrowly tailored to “professional services” of particular industry. • Terms vary widely not only by industry, but also by insurer within an industry group.

Typical E&O Insuring Agreement • “To pay on behalf of the Insured all sums which the Insured shall become legally obligated to pay as Damages resulting from any Claims first made against the Insured and reported to the Insurer during the Policy Period … for any Wrongful Act of the Insured or any other person for whose actions the Insured is legally responsible, but only if such Wrongful Act … occurs solely in the rendering or failure to render Professional Services.” • AIG, Mortgage Bankers/Mortgage Brokers E&O Insurance, 63530 (3/96).

Other Common Features of E&O Coverage • Claims-Made Coverage (claim generally must be made against insured during policy period; often claim must be reported to insurer during policy period or set time period thereafter). • Defense (policies vary widely, but certain policies issued to mortgage lenders include a duty to defend, rather than a duty to reimburse defense costs). • Damages (often defined broadly to include all economic losses, but some policies limit coverage for fines, penalties, and/or punitive damages).

Other Common Features of E&O Coverage, cont’d. • “Claim” – wide variation of coverage for regulatory investigations or proceedings. • Some policies expressly include administrative/regulatory proceedings and investigations. • Some policies define “Claim” as “any demand against the Insured for monetary Damages, and includes a lawsuit” (silent on regulatory proceedings). • Some policies exclude Claims brought by any state or federal regulatory or administrative agency.

E&O v. D&O • The line between D&O and E&O is not always clear, and certain lawsuits may potentially trigger coverage under both lines of coverage. • “Professional Services” • D&O policies generally exclude claims related to rendering of “professional services.” • E&O policies expressly afford coverage for “professional services.” • “Insured” • D&O (directors and officers and, in limited circumstances, company and/or employees). • E&O policies often define “Insured” more broadly to include the company itself, as well as directors, officers, employees, and third-parties for whose actions the Insured is legally responsible.

Definition of “Professional Services” • Some policies define “professional services” generically: • One policy defines Wrongful Act as certain errors or omissions committed by the Insured “solely in the performance of or failure to perform professional services for others in the Insured’s Profession as stated in Item 1.A. of the Declarations.” London, Specimen SUA MCPL 04. • Many policies specifically define “professional services” based on industry of policyholder.

Definition of “Professional Services,” cont’d. • Lenders (“the origination, sale, pooling and servicing of mortgage loans secured by real property…”). • Financial Services firms (“services that an Insured renders pursuant to an agreement with a customer or client, as long as the customer pays a fee, commission, or other compensation …”). • Investment Banks (“those services performed … by the Insured (or by any other person or entity for whose acts, errors, or omissions the Insured is … legally responsible) for, for the benefit of, or on behalf of a Customer … for a fee, commission or other consideration”).

Potential Exclusions and Defenses • Fraud Exclusions. • Final Adjudication standard v. “In fact” standard. • Specific Endorsements excluding claims for “Predatory Lending” claims. • Exclusions barring claims arising from any investor’s interest in mortgage-backed securities or the filing of any registration statement therewith, unless the claim results from the rendering of Professional Services.