Bridge Loan Process: Streamlined Application and Documentation

The bridge loan process is straightforward, requiring a signed purchase agreement for the new property, a firm sale agreement for the current home, equity-based loan amount calculations, and lender or broker applications. Best Mortgage Onlineu2019s process analysis details application simplicity, documentation requirements, and processing speed. Understanding the bridge loan process enables Canadian homebuyers to accelerate approvals through a comprehensive study and professional consultation, ensuring process optimization.<br><br>https://bestmo.ca/alternative-mortgage/bridge-loan/

Bridge Loan Process: Streamlined Application and Documentation

E N D

Presentation Transcript

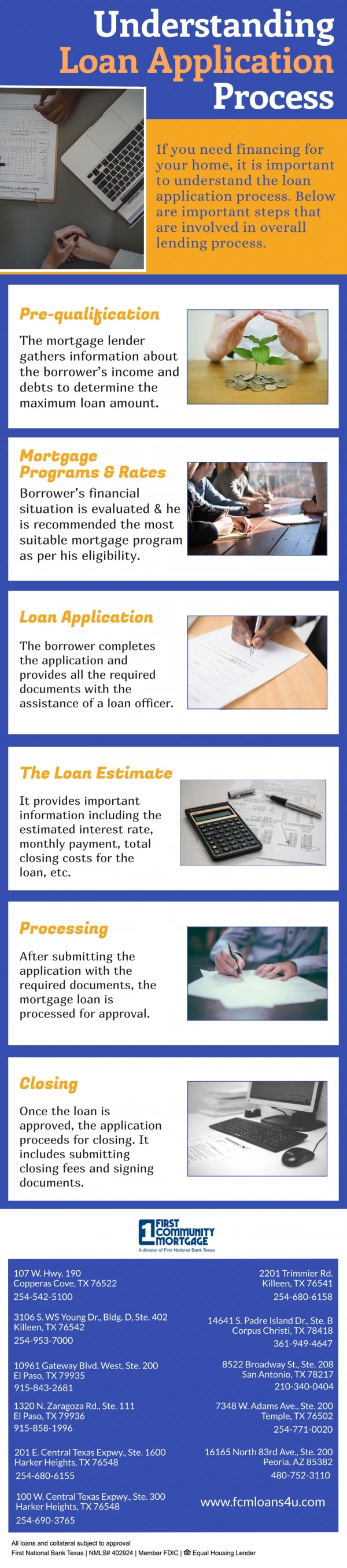

What is a Bridge Loan? How does it Work in Canada? Home Alternative Mortgage Options in Canada What is a Bridge Loan? How does it Work in Canada? Are you looking to buy a new home before selling your current one? A bridge loan or bridge mortgage is an alternative mortgage option which allows Canadian homebuyers to access the equity in their current property to put towards purchasing a new home. This guide covers everything you need to know about bridge mortgage, including how they work, costs, bene?ts, risks, and alternatives. What is a Bridge Loan? A bridge loan, also known as interim ?nancing or a gap loan, is a short-term mortgage designed to close the gap between the closing dates on a new home purchase and the sale of an existing home. These loans allow homebuyers to tap into the equity built up in their current property to come up with the down payment on a new home purchase. This provides ?exibility for buyers who ?nd their dream home before selling their existing one. They are generally repaid within 90 – 120 days, the typical timeframe between closing on the sale and purchase. You continue paying the mortgage on your current property until the new purchase closes. The funds are advanced to your real estate lawyer, who handles the down payment when you close the new purchase. The bridge loan itself is never in your possession. Once your current home sale closes, your lawyer repays the loan amount plus applicable fees and interest out of the equity proceeds. How does a Bridge Loan Work? There are 3 scenarios where a bridge loan helps homeowners buy a new property when the timing of the sale and purchase do not align perfectly:

Buying before selling your current home Many homebuyers come across their ideal new home before ?nding a buyer for their existing property. A bridge loan allows you to take advantage of the equity you have built up and put an o?er on your next home without waiting for the sale to close. New purchase closing sooner than sale If the closing date for your new property comes before the closing date for the sale of your current home, a bridge loan covers the gap in between. This provides faster access to your down payment funds. Time needed between selling and buying Some homeowners want a period of time between the sale and purchase to handle renovations, packing, and moving. A bridge loan lets you close on the new property ?rst while giving you breathing room before the sale closes. When Are Bridge Loans Needed? How is the Amount of a Bridge Loan Calculated? Lenders will assess the amount you qualify for based on the equity built up in your current home, minus estimated closing costs: Home equity – The current market value of your home minus what you owe on your mortgage determines the equity available. Closing costs – Expenses like legal fees, taxes, and title transfer fees must be accounted

for. Loan amount – Your lender will advance up to 80-90% of the remaining equity after closing costs. For example, if you have $200,000 in equity and $10,000 in estimated closing costs, you may qualify for a loan of up to $180,000. What Are the Pros and Cons of Bridge Mortgages? What are the bene?ts? There are 5 advantages bridge loans o?er Canadians buying and selling properties: Buy before selling – This loan allows you to purchase a new home before ?nding a buyer for your existing property, eliminating timing challenges. Access equity – Tap into your built-up home equity for the new down payment instead of waiting until after closing. More moving time – Closing on the purchase ?rst provides more time for renovations, packing, and moving before the sale closes. Avoid two mortgage payments – You only need to pay one mortgage at a time on your current home until the new purchase closes. Act quickly in a competitive market – This loan allows you to jump on a new listing by securing your down payment funds ahead of the sale. While bridge loans provide ?exibility, there are 3 risks to consider: Higher interest rates – These loans typically have higher interest rates, similar to a home equity line of credit or an open mortgage.

Paying two mortgages – If the sale of your current home falls through, you may make payments on both mortgages until a new buyer is found. Default risk – The short repayment timeframe means defaulting if the sale does not close on time, which poses a risk. Carefully evaluate the trade-o?s of bridge loans to make an informed decision on your home buying process. What is the Process to Get a Bridge Loan? The process to apply for a bridge loan is relatively straightforward. You’ll need: Signed purchase agreement for the new property Signed (or ?rm) sale agreement on your current home Calculate the loan amount based on your equity and closing costs Apply through your mortgage lender or broker Lenders can often process this loan quicker than regular mortgages, sometimes within a week of ge?ing the needed documentation. Where Can You Get Bridge Loans in Canada? While not all lenders o?er them, bridge loans are available from a variety of reputable lending sources in Canada, including: Major Banks Most of Canada’s Big Six Banks provide bridge loans, including TD, Scotiabank, RBC, CIBC, and BMO. Their loans often get packaged together with the new mortgage. Credit Unions Local credit unions are an option for bridge ?nancing in many regions. They may o?er more ?exibility than major banks when evaluating eligibility. Online Lenders Various online-based lenders in Canada, including mortgage investment corporations (MICs), o?er bridge loans. They provide quicker approvals and funding than banks. Mortgage Brokers Experienced mortgage brokers have access to these loans through their lending networks. Brokers can compare multiple institutions’ options to ?nd the best rate and terms. The most competitive rates are available to quali?ed borrowers with good credit, moderate debt levels, and su?icient home equity built up.

How Much Does a Bridge Loan Cost? How Much Does a Bridge Loan Cost? Bridge loans come with higher interest rates and fees compared to traditional mortgages: Interest rate – Usually prime + 2% or 3%, similar to an open mortgage or home equity line of credit. [Source] Administration fees – Lenders typically charge $200-500 to arrange. Legal fees – If a lien is registered on your property, lawyer costs apply to remove it after repayment. While these loans have higher costs, you only pay interest for the short duration between closings, minimizing the amounts. What Are the Alternatives to a Bridge Loan? If bridge ?nancing does not ?t your situation, here are 4 options to consider: Options Details A revolving credit line against your home Home equity line of credit equity. The interest rate is usually lower. Ask the buyers of your current home if you Rent-back agreement can rent it back for the gap period between closings.

Staying with family/friends or renting a Temporary housing short-term place can provide ?exibility. Coordinating the closing of your sale and the Align closing dates new purchase for the same day avoids the gap entirely. Explore more alternative mortgage solutions to navigate Canada’s complex housing market: Bad Credit Mortgage Debt Consolidation Mortgage Investment Property Mortgage Vendor Take Back Mortgage Key takeaways: How to Decide if a Bridge Loan is Right for You? Consider the following factors when deciding if a bridge loan suits your home buying/selling needs: Will the gap between my sale and purchase closings be 90 days or less? This loan is ideal for short gaps. Do I have at least 20% equity in my current home? You typically need signi?cant equity built up to qualify. Is my credit score strong? This loan requires good credit scores. Otherwise, you can opt for alternative lenders like B-lenders or Private lenders. Can I handle the higher interest rate and fees? Factor in the total costs. Am I comfortable with the risks, like a failed sale? Assess your risk tolerance. For Canadians navigating the home buying and selling process, bridge loans can provide much- needed ?exibility when the timing is challenging. While coming with risks and higher costs, they allow you to access your equity before your sale and capitalize on competitive purchase opportunities. As with any ?nancial decision, researching, evaluating alternatives, and seeking expert guidance is key to determining if a bridge loan makes sense for your goals. FAQs about Bridge Loan in Canada How long do you have to repay a bridge loan in Canada? Bridge loans typically must be repaid within 90-120 days in Canada. Your lawyer repays the loan using proceeds from selling your current home.

Who offers bridge loans in Canada? Major banks, credit unions, mortgage investment corporations, online lenders, and mortgage brokers in Canada o?er bridge loans. How do you qualify for a bridge loan in Canada? It would help if you typically had good credit (700+ score), at least 20% home equity, a low debt-to-income ratio, secure employment, and a mortgage pre-approval for the new property. Can you get a bridge loan for over 90 days in Canada? Most bridge loans are capped at 90-120 days. Longer terms may be available in unique cases after extensive lender evaluation. The interest rates and fees will be much higher. Do you make interest payments on a bridge loan in Canada? Interest accrues daily on bridge loans, but you do not make payments. The interest owed gets repaid as part of your closing costs when the sale of your home ?nalizes. Can you default on a bridge loan in Canada? Yes, default is possible if the sale of your current home encounters delays extending beyond the bridge loan repayment date, usually 90-120 days. This should be avoided. Do bridge loans affect your credit score in Canada? Bridge loans can negatively impact your credit if you miss payments on your existing home mortgage before it sells or if you default on repaying the bridge loan itself. Are bridge loans risky in Canada? Bridge loans do carry risks, including higher rates/fees, paying two mortgages, and defaulting if your sale is delayed. Make sure you evaluate the risks before proceeding. Article Sources Company HOTTEST NEWS Privacy Policy Canada Land Transfer Tax BestMo helps you search for Canada’s home loans by answering just a few simple questions. Our process eliminates in?ated interested rates, fees, and unnecessary time-wasting. Because a home loan doesn’t have to be so complicated. Term Of Service Bank of Canada Rate Schedule Best HELOC rates About Us Reverse Mortgage in Canada Overview Contact Us Visit our blog Check it out

Disclaimer: The information provided on bestmo.ca should not be construed as professional financial advice. This website only provides referrals to financial service providers and accepts no liability for the products, services, or advice given by these third parties. It is your responsibility to evaluate any service provider thoroughly before engaging their services. The website owner will not be held responsible for any errors or omissions in this information, nor for the availability of this information. All mortgage rates, terms, and programs are subject to change at any time without notice. This website does not make any guarantees regarding special offers or promotions posted on this website. By using bestmo.ca, you agree to hold the owner and operator harmless from any disputes that may arise from your use of this website. Copyright by BestMO in Canada © All rights reserved