Download

1 / 44

440 likes | 552 Vues

Discover the significance of present value and future value in financial decisions using examples and interest formulas. Learn about accumulating interest over time, annuities, and the impact of interest rates on investment decisions.

E N D

Present Value Calculations The Time Value of Money

Which would you rather have, $1,000 now or $1,000 in three years? Since you can invest the $1,000 now and have the $1,000 plus interest in three years, the $1,000 now would be preferable.

Which would you rather have, $1,000 now or $1,500 in three years? The answer depends upon the amount of interest that you can earn during the three years, which depends upon the interest rate at which you can invest.

How much interest would accumulate over time? • The longer the time, the more interest will accumulate. • The higher the interest rate, the faster the interest will accumulate. • In later periods, interest will be earned on the interest from earlier periods.

Accumulating InterestPeriod Beginning Interest. Ending . • 1 P

Accumulating InterestPeriod Beginning Interest. Ending . • 1 P P*I

Accumulating InterestPeriod Beginning Interest. Ending . • 1 P P*I P+(P*I)

Accumulating InterestPeriod Beginning Interest. Ending . • 1 P P*I P+(P*I) =P*(1+I)

Accumulating InterestPeriod Beginning Interest. Ending . • 1 P P*I P+(P*I) =P*(1+I) • 2 P*(1+I)

Accumulating InterestPeriod Beginning Interest. Ending . • 1 P P*I P+(P*I) =P*(1+I) • 2 P*(1+I) P*(1+I)*I

Accumulating InterestPeriod Beginning Interest. Ending . • 1 P P*I P+(P*I) =P*(1+I) • 2 P*(1+I) P*(1+I)*I P*(1+I)+P*(1+I)*I =P*(1+I)2

Accumulating InterestPeriod Beginning Interest. Ending . • 1 P P*I P+(P*I) =P*(1+I) • 2 P*(1+I) P*(1+I)*I P*(1+I)+P*(1+I)*I =P*(1+I)2 • 3 P*(1+I)2 P*(1+I)2*I P*(1+I)2+P*(1+I)2*I =P*(1+I)3

Accumulating InterestPeriod Beginning Interest. Ending . • 1 P P*I P+(P*I) =P*(1+I) • 2 P*(1+I) P*(1+I)*I P*(1+I)+P*(1+I)*I =P*(1+I)2 • 3 P*(1+I)2 P*(1+I)2*I P*(1+I)2+P*(1+I)2*I =P*(1+I)3 • 4 P*(1+I)3 P*(1+I)3*I P*(1+I)3+P*(1+I)3*I =P*(1+I)4

Accumulating InterestPeriod Beginning Interest. Ending . • 1 P P*I P+(P*I) =P*(1+I) • 2 P*(1+I) P*(1+I)*I P*(1+I)+P*(1+I)*I =P*(1+I)2 • 3 P*(1+I)2 P*(1+I)2*I P*(1+I)2+P*(1+I)2*I =P*(1+I)3 • 4 P*(1+I)3 P*(1+I)3*I P*(1+I)3+P*(1+I)3*I =P*(1+I)4 • N P*(1+I)N

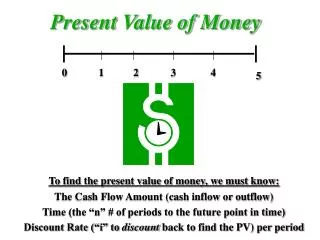

Present and Future Values of a Dollar • Future Value - FV 1 2 3 45 6 7 • Present Value - PV

Interest Formulas • FV$ = (1+I)N • PV$ = (1+I)-N = 1/ PV$

Present and Future Value of a Dollar Calculations • Present Value = Known Future Value * PV$ • Future Value = Known Present Value * FV$

Future Value of a Dollar • Invest a known amount now and find what it is worth in the future. • Given a known sales price now, how much will be due if payment is delayed.

How much will we have if we invest $1,000 for 8 years at 10% • We know the present value, we want to find the future value. • Future Value = Present Value *FV$ • Future Value = $1,000 * (1.10)8. • Future Value = $1,000 * 2.143 • = $2143.60

How much will we have to invest now at 7% if we want to have $5,000 in 6 years? • We know the future value ($5,000), we want to find the present value. • Present Value = Future Value *PV$ • Present Value = $5,000 * (1.07)-6. • Present Value = $5,000 * .6663 • = $3,331.70

In the interest formulas, “i” and “n” must agree • I n . • rate per month number of months • rate per quarter number of quarters • rate per year number of years

Observations about Interest Factors • As you move forward, the magnitude grows! • As you move back, the magnitude declines! • The greater the interest rate, the greater the change! • The greater the number of periods, the greater the change!

Annuities • A series of payments through time • Often the payments are equal • End of year payments form an ordinary annuity • Beginning of year payments form an annuity due

Annuities • Bond Interest • Mortgage Payments • Lease Payments • Pension Contributions • Pension Withdrawals • Installment Payments

Annuities • The present value of the annuity is the sum of the present value of each of the payments (p).

Annuities • PV=p*(1+I)-1+ p*(1+I)-2+ p*(1+I)-3+…+ p*(1+I)-n • PV=p*[(1+I)-1+(1+I)-2+ (1+I)-3+…+(1+I)-n] • PV=p*PVA • PVA= (1+I)-1+(1+I)-2+ (1+I)-3+…+(1+I)-n

Present Value of an Annuity • PVA=(1+I)-1+(1+I)-2+ (1+I)-3+….+(1+I)-n • (1+I)*PVA=1+(1+I)-1+(1+I)-2+ (1+I)-3+.+(1+I)-n+1 • I*PVA=1-(1+I)-n • PVA=[1-(1+I)-n]/I • PVA=[1-PV$]/I

Annuity Interest Factor • Given the payment, the interest rate and the duration, we can calculate the present value. PV = P * PVA • Given the present value, the interest rate and the duration, we can calculate the payment. P = PV / PVA

Numeric Example - Annuities • Suppose that you want to take out a $125,000 mortgage from your local bank to purchase a new home. If the mortgage rate is 12% and you wish to finance over 30 years, what will your monthly mortgage payment be? • Ignore taxes, both income and property.

Numeric Example - Annuities • We know the present value and wish to calculate the payment. • P = PV /PVA • = 125,000 / [1-PV$] / I [n=360, I=.01] • = 125,000 / [1-.02782] / .01 • = 125,000 / 97.218 • = 1,285.77

Numeric Example 2 - Annuities • Suppose that we are considering leasing some equipment for 36 months for $500 per month. The equipment has an economic life of 5 years, and we could purchase it for $16,500. • A reasonable rate of interest is 8%.

Numeric Example 2 - Annuities • To compare the lease and purchase options, we must find the present value of the lease payments. • PV = P * PVA • = 500 * [1-PV$]/I N=36I=.006667 • = 500 * [1-.7873]/.006667 • = 500 * [31.91] = $15,955

Numeric Example 2 - Annuities • Lease Option • pay 15,955 to use asset for 3 years • Purchase Option • pay 16,500 to use the asset for 5 years

Future Value of an Annuity • The interest factor for the future value of an annuity can be constructed by adjusting PVA. PVA will convert a series of future payments into a single sum equivalent at time 0. If we can move the single sum to the end of period N, we will have FVA. • FVA = PVA * FV$ = [FV$ - 1] / I

Future Value of an Annuity FV = P * PVA * FV$ Payments- P PVA 1 2 3 4 5 6 7 FV$ PV FV

Annuity Due • Same as an ordinary annuity, except that the payments are at the beginning of the year rather than at the end of the year. • Common on leases and installment payments.

Interest factor for an annuity due. • Since the end of year one is the same as the beginning of year two, most of the payments are the same. • The annuity due has an extra payment at the beginning and is missing a payment at the end.

Ordinary Annuities and Annuities Due 7 Year Annuity and 7 Year Annuity Due Annuity 0 1 2 3 4 5 6 7 Annuity Due

Adjusting PVA for End of Year Payments • Since the first payment of the annuity due happens at time period 0, it has an interest factor of 1.0. • We can eliminate the extra payment at the end of the ordinary annuity by subtracting 1 from N. • PVAD = PVA(N-1) + 1

Numeric Example • Suppose that we sell $5,000 of merchandise to a customer who wished to pay in 36 monthly installments beginning immediately. • Assume that a reasonable interest rate is 12%.

Numeric Example • We know the Present Value and wish to calculate the payment. • P = PV / PVAD • = 5,000 / [PVA(35) + 1] • = 5,000 / [29.41 +1] • = 164.43

Future Value of an Annuity Due • FVDA can be constructed from PVAD, just as FVA was constructed from PVA. • FVAD = PVAD * FV$

Perpetuities • Perpetuities are annuities to continue forever. Consider the formula for PVA when N gets very large. • PVP = [1-(1+I)-] / I = 1 / I • This is similar to the concept of a P/E ratio and is the foundation for the earnings capitalization method for valuing a business.

Summary of Interest Factors • PV$ = (1+I)-N • FV$ = 1/PV$ • PVA = (1-PV$)/I • FVA = PVA * FV$ • PVAD = PVA(N-1)+1 • FVAD = PVAD *FV$ • PVP = 1/I