Download

1 / 19

210 likes | 592 Vues

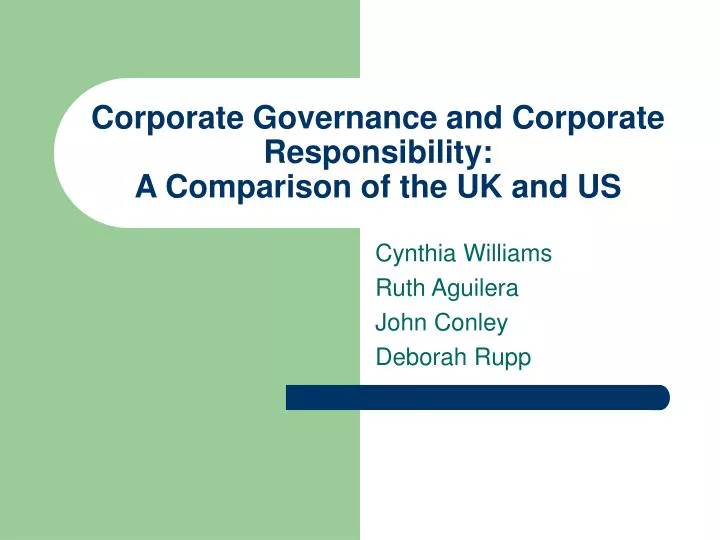

Corporate Governance and Corporate Responsibility: A Comparison of the UK and US. Cynthia Williams Ruth Aguilera John Conley Deborah Rupp. CAPITAL MARKETS. LAW. SUPPLIERS. MANAGERS. OWNERS. FIRM. EMPLOYEES. BOARD OF DIRECTORS. CONSUMERS. LABOR MARKETS. PRODUCT MARKETS.

E N D

Corporate Governance and Corporate Responsibility:A Comparison of the UK and US Cynthia Williams Ruth Aguilera John Conley Deborah Rupp

CAPITAL MARKETS LAW SUPPLIERS MANAGERS OWNERS FIRM EMPLOYEES BOARD OF DIRECTORS CONSUMERS LABOR MARKETS PRODUCT MARKETS

Dispersed ownership/uncommitted owners Developed financial markets “Relatively” high financial transparency Active mergers and acquisitions market Flexible labor markets Low employee participation in management “Outsider” system of accountability v. “insider” Anglo-American system(in contrast to Continental system):

Refinements to the UK/US Portrait: • “Dispersed ownership” versus increasing institutional ownership • 60% of US market and 80% of UK market held by institutions, domestic and foreign • Owners can coordinate action and act collectively in both market

Differences between the UK/US • Inside the firm: • CEO and Chair of Board are split in 90% of UK companies (Higgs) • CEO and Chair are split in only 19% of US companies (Higgs) • CEO compensation design in US (higher absolute levels and greater incentive proportion) may indicate greater power

Differences between the UK/US • Between the firm and stockholders: • More of institutional ownership in the UK is comprised of pension funds and insurance companies • US: higher concentration of mutual funds • Do pension funds and insurance companies exhibit a longer time-frame in their investment strategy? • Indexed owners should as well: Hawley & Williams Fiduciary Capitalism • Turnover is lower for UK institutions v. US institutions

How stockholders act: UK • Engagement: Cadbury and then Myners have encouraged • Result: quiet diplomacy on strategy, board effectiveness, succession, executive remuneration: Black & Coffee, 1994; Holland, 1998 • Financial institutions avoid “one man show” style of US CEOs: Holland, 1998 • Mallin et al., 2005: Outsiders in the traditional corporate governance framework are starting to act like the insiders of Continental system

How stockholders act: US • Institutions typically have a more distant relationship • US securities law may require • Reg. FD discourages quiet diplomacy • Recent SEC proposal to allow shareholders more power in the relationship (nominations) have been rejected • Communications filtered through IR departments, not direct to the top as we’ve heard in the UK • Closer to the “outsider” model than in the UK

Government emphasis differs • www.csr.gov.uk • The UK government gateway to Corporate Social Responsibility: • “Welcome to the Government’s website on CSR. We have an ambitious vision for UK businesses to consider the economic, social and environmental impacts of their activities, wherever they operate in the world.” • OFR: new requirement for boards to disclose effects of company action on environment and society • What will the impact be? How important is it? • We’ve heard conflicting accounts • Explicit emphasis on long-term shareholder value

Government: • Mr. Malcolm Wicks is the new Minister for Corporate Social Responsibility. • "I want Britain to be a leading player in this coming green industrial revolution"Rt Hon Tony Blair MP, Prime Minister

Institutional investors’ actions • SIP requirements to disclose SEE as context • Conley & Williams interviews: this made a significant difference in fund’s behavior • ISC principles, 2002: Will intervene for business strategy and if approach to CSR is problematic • ABI, Disclosure Guidelines, 2000: Expect disclosure on approach to CSR • Coalitions on climate change, HIV/Aids, oil and gas revenue transparency, labor conditions in supply chains • Why?

Aguilera, Rupp, Williams & Ganapathi: Three basic motives based on justice research (Cropanzano, Byrne, Bobocel & Rupp, 2001; Cropanzano, Rupp, Mohler, & Schminke, 2001) • Instrumental motives-self-interest driven • Relational motives- concerned with relationships among group members • Moral motives-concerned with ethical standards and moral principles

Theoretical Framework Aguilera, Rupp, Williams & Ganapathi (AMR, forthcoming 2006)

Application to institutional investors: • Instrumental motives predominate • Competitive advantage to firms’ reputations from attending to environment and social issues • Reputation affects stock prices and reduces volatility (Clark & Hebb, 2005) • E.g., Extractive Industry Transparency Initiative • E.g,, I.I. Group on Climate Change

Other motivations • Relational: Could be a bandwagon effect • E.g., 11 of 20 top fund managers in Social Investment Forum, interviews show not all “true believers” • Moral: Individuals within funds may have strong moral or political views about these matters • Usually discuss in terms of long-term value of investments, not their own values

Why less interest in the US? • No required disclosure of social and environmental facts, either by companies or pension funds • No systematic government encouragement • Less consumer interest, so less likely to have a consumer backlash? • Demonstrating financial materiality is required in order to interest US mainstream investors • Geography and sociology of London allow norms to shift rapidly • What else are we missing?

Conclusions • On matters of core corporate governance, important differences • UK is becoming more relational/more like an “insider” system • More emphasis on long-term shareholder value, at least by government and some large shareholders • CSR is a wedge issue that is further driving differences • At some point it becomes inaccurate to speak of “Anglo-American” corporate governance system