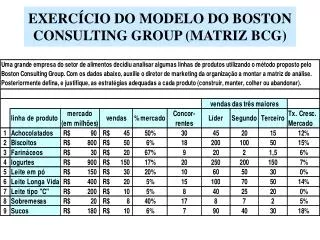

Download

1 / 11

170 likes | 663 Vues

El Modelo Econométrico. Y= XB + U. CONSTRUCCIÓN DE MODELOS ECONOMÉTRICOS. VARIABLES. Y t = β 0 + β 1 X 1t + β 2 X 1t-1 + β 3 X 2t + β 4 y t-1 + u t. Predeterminadas (exógenas), explicativa o regresor. Endógena, explicada o regresando. Perturbación aleatoria.

E N D

El Modelo Econométrico Y= XB + U

CONSTRUCCIÓN DE MODELOS ECONOMÉTRICOS VARIABLES Yt = β0 + β1 X1t + β2 X1t-1+ β3 X2t + β4 yt-1 + ut Predeterminadas (exógenas), explicativa o regresor Endógena, explicada o regresando Perturbación aleatoria

CONSTRUCCIÓN DE MODELOS ECONOMÉTRICOS X21=0, X22=0, X23=1, X24=0, X25=0, ..... VARIABLES Yt = β0 + β1 X1t + β2 X1t-1+ β3 X2t + β4 yt-1 + ut Retardadas o desplazadas Endógena, explicada o regresando

CONSTRUCCIÓN DE MODELOS ECONOMÉTRICOS VARIABLES. COEFICIENTES. Multiecuacional Y1t = β0 + β1 X1t + β2 X1t-1+ β3 X2t + β4 yt-1 + ut Coeficientes Endógena, explicada o regresando Y2t = β5 + β6 Y1t + β7 X1t-1 + wt

CONSTRUCCIÓN DE MODELOS ECONOMÉTRICOS FASE DE ESPECIFICACIÓN • ELECCIÓN DEL CAMPO DE APLICACIÓN • CONOCIMENTO PREVIO DEL SISTEMA • BÚSQUEDA DE MODELOS EN EL ÁREA ELEGIDA (INVESTIGACIÓN BIBLIOGRÁFICA) • CAPTACIÓN DE INFORMACIÓN (DEPURACIÓN, HOMOGENEIZACIÓN,...)

CONSTRUCCIÓN DE MODELOS ECONOMÉTRICOS FASE DE ESPECIFICACIÓN • Relación Funcional • Coeficientes y Variables • Ct = 0 + 1 Rt + 2 Ct-1 + ut • t= 1980-2000 Consumo

CONSTRUCCIÓN DE MODELOS ECONOMÉTRICOS Software especializado (MCO,MCI,...) FASE DE ESTIMACIÓN • Ct = 0 + 1 Rt + 2 Ct-1 + ut • t= 1980-2000 Cálculo de Estimadores, valor estimado de la endógena y residuos • ^ ^ ^ ^ • Ct = 0 + 1 Rt + 2 Ct-1 + ut

CONSTRUCCIÓN DE MODELOS ECONOMÉTRICOS Software especializado (MCO,MCI,...) FASE DE CONTRASTE Y VALIDACIÓN • Ct = 0 + 1 Rt + 2 Ct-1 + ut • t= 1980-2000 Contraste del modelo, Hipótesis de los parámetros estimados y propiedades de los residuos • ^ ^ ^ ^ • Ct = 0 + 1 Rt + 2 Ct-1 + ut

CONSTRUCCIÓN DE MODELOS ECONOMÉTRICOS Software especializado (MCO,MCI,...) FASE DE CONTRASTE Y VALIDACIÓN • Ct = 0 + 1 Rt + 2 Ct-1 + ut • t= 1980-2000 Validación del Modelo: Bondad del modelo, medidas de error, modelos alternativos... • ^ ^ • Ct - Ct = ut • F, R2,SR, ECM...

CONSTRUCCIÓN DE MODELOS ECONOMÉTRICOS FASE DE UTILIZACIÓN Perfeccionamiento del Modelo (mejoras, método iterativo) • Ct = 0 + 1 Rt + 2 Ct-1 + ut • t= 1980-2000 • Análisis Estructural • Evaluación de Políticas • Predicción

CONSTRUCCIÓN DE MODELOS ECONOMÉTRICOS INFORME A REDACTAR: ESTUDIO ECONOMÉTRICO • Índice, • Resumen (tema, modelo, datos, método, conclusiones) • Introducción (Objetivos) • Antecedentes econométricos • Modelo Seleccionado (notación, alternativas, modelo final) • Datos Utilizados (tablas, transformaciones,...) • Estimación y Contraste • Principales Resultados. Conclusiones • Bibliografía.