Download

1 / 4

40 likes | 60 Vues

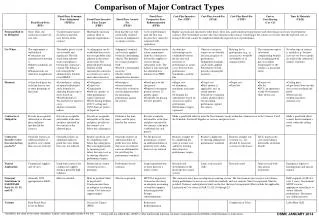

This review explores market risk, credit risk, liquidity risk, operational risk, reputation risk, and fraud. It also discusses questions that a risk manager may ask regarding interest rates, issuer exposure, risk distribution, capital adequacy, and risk profiling.

E N D

Review of the Major Risk Types • Market Risk • Sensitivity to the parameters of our pricing functions • Credit Risk • Probability that the other side fails to live up to a contract • Liquidity Risk • Not enough funds on hand to manage daily cash management needs • Operational Risk • System failures, human mistakes • Reputation Risk • Are we doing the right thing? Ethics matter. • Fraud • Sometimes people do bad things

Questions a Risk Manager May Ask… • How sensitive am I to interest rate changes? • Fed action • Fed tightening/easing • FOMC desk “Quantitative Easing” • Supply and demand • The market’s view : “implied” future interest rate environment • How exposed am I to a particular Issuer? • They may request a bank loan and we want to know how much debt they have outstanding • How is my risk distributed in my trading book? • By rating, by maturity bucket, by issuer • What does history tell us about what to expect in the future? • VaR :“Value a Risk” • How much capital should I have on hand for a rainy day (VaR is an input) • What extreme moves should I test for (that may not have already happened)? • Stress testing vs. “expected” moves • How do I know I have just the right amount of capital (not too much)?

Questions a Risk Manager May Ask (cont.) • Are we net long or short, and where in the term structure? • How did my risk profile change during the day, from yesterday, last week, last month? • “Position” Pnl • “New business” (trading activity from beginning of day to close of day) • Risk of new portfolio - where did risk change come from? Which position(s)? • How much PnL did I realize? • Realized vs.. unrealized PnL • Mark to Market • Does the desk have a view?

Historical VaR & Stress Testing • What does this mean: “95% 1 day VaR is $1mm” • What is VaR primarily used for? • Limitations of VaR • Run pricing scenarios on total book and calculate total risk: • All yields by +10, +50, +100, +150, +200 basis points • All yields by -10, -50, -100, -150, -200 basis • Tilt up and down (flattener/steepener) • Need historical data to calculate day over day P&L changes • We will treat these as pricing scenarios applied to our trading book today • Full re-val VaR vs stored sensitivity approximation