Download

1 / 14

210 likes | 752 Vues

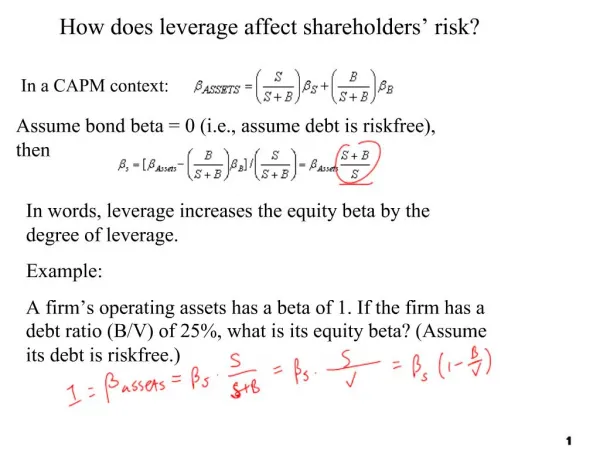

Double Leverage: A Seductively Dangerous notion. Rate-making Capital Structure: Holding Company vs. Operating Company Enrique Bacalao 45 th Financial Forum Society of Utility and Regulatory Financial Analysts April 18, 2013. Hypothetical Capital Structures.

E N D

Double Leverage:A Seductively Dangerous notion Rate-making Capital Structure: Holding Company vs. Operating Company Enrique Bacalao 45th Financial Forum Society of Utility and Regulatory Financial Analysts April 18, 2013

Hypothetical Capital Structures • Double leverage can be viewed as a sub-set of the use of hypothetical capital structures in regulatory proceedings. • Question: Under what circumstances might the use of a hypothetical capital structure be appropriate? • Suggested answer: Only when it would render a more accurate reflection of the regulated utility company’s marginal cost of capital. • Challenge: This answer requires judgment – it’s definitely not an automatic or prescriptive approach. • Example: South Beloit Water Gas and Electric Company

The Concept of Double Leverage • Can be imputed to a utility operating company that: • Has issued its own debt • Is wholly owned by a parent holding company • Whose parent holding company has also issued debt • The term “double leverage”: • Initial financial leverage on the earnings for the operating company’s common stock • Additional financial leverage on the earnings for the parent holding company’s common stock to the extent it has borrowed the funds invested in the operating company’s common stock • Imputation could be extended to additional leverage if there are additional levels of corporate ownership in the holding company.

Alternative Imputation Methods • The parent company’s weighted average cost of capital (WACC) determines the operating company’s cost of equity • Equity contributions and retained earnings are both deemed to have been funded by a blend of parent company equity and debt • The parent company’s WACC becomes the utility’s cost of equity • The operating company’s debt-to-capital ratio rises as a result • The parent holding company’s WACC determines only part of the operating company’s cost of equity • The operating company’s retained earnings are not adjusted • Only the portion of equity that has been contributed by the parent is adjusted to reflect double leverage, as above • The operating company’s debt-to-capital ratio rises as a result

Double Leverage Assumptions In order to justify double leverage adjustments: • The parent holding company must have debt outstanding • The debt must be deemed to have funded incremental equity investments in the utility operating company • The business and financial risk profile of the holding company’s other subsidiaries are identical to the operating utility company’s profile • The resulting distortion to the operating company’s financial leverage does not affect its cost of capital • Financial analysis (both credit and equity) disregards any difference between operating and holding companies

The Siren Song • Holding companies that qualify for a double leverage adjustment would enjoy a windfall profit, absent the adjustment (higher equity rates of return being earned for lower-cost debt funding) • Stand-alone utility companies face a higher cost of equity than comparable utility companies owned by a levered holding company (unfair treatment) • These excess earnings, as with any subsidy, distort commercial incentives and capital budgeting decisions (triggering the white elephant syndrome)

Fundamental Flaws with the Notion • Economic concepts violated: • The return required by an investor is a function of the risk of the investment. • The cost of equity is therefore the risk-adjusted opportunity cost faced by the marginal investor. • The cost of equity is not a function of how the investment is funded. • The cost of equity is based on future expectations, not historical events. • Practical concepts violated: • Equity is equity, regardless of its ownership or funding source • Retained earnings are incorrectly treated: • One approach assumes the parent funds retained earnings (wrong) • The other approach treats equity contributions and retained earnings differently, thus leading to two different costs of equity simultaneously for the same company (wrong)

The Nonsense Exposed If double leverage imputation were accepted as being reasonable, then two otherwise identical utility companies would face different costs of capital if the equity: • Was funded differently; or • The ownership of one did not involve a parent holding company while the ownership of the other did; or • The ownership had to be traced back to each ultimate beneficial owner and the imputed leverage calculated for each company accordingly. The valuation of those two otherwise identical utility companies would also be different as a result of: • Variations in ownership • Variations in the funding of tha ownership

Based on Reasonable Assumptions? The Underpinning Assumptions Comments and Questions What if the parent issued preferred stock instead of debt? Requires tracing funds dollar-for-dollar from sources to uses: Quixotic proposition Highly unlikely in almost all cases, even if all other operating subsidiaries are also utility companies Unreasonable assumption - viewed negatively by credit rating agencies Highly unlikely in almost all cases: Structural subordination of parent company debt Differences in business risk profiles between operating and holding companies • The parent holding company must have debt outstanding • The debt must be deemed to have funded incremental equity investments in the utility operating company • The business and financial risk profile of the holding company’s other subsidiaries are identical to the operating utility company’s profile • The resulting distortion to the operating company’s financial leverage does not affect its cost of capital • Financial analysis (both credit and equity) disregards any difference between operating and holding companies

The Reality for Utility Holding Companies • The risk profiles of its subsidiaries sets the risk profile and cost of equity for the holding company, not the other way around. • The business risk profile of various subsidiary companies is different, leading to individual optimal capital structures • Consequently, the optimal capital structure of the parent holding company and that of any one of its regulated operating subsidiaries is necessarily different • Financing at the parent holding company is driven by its own investment requirements, not those of its subsidiaries • The investment requirements vary over time among its subsidiaries • The mere existence of parental debt does not prove it has been used to fund its equity at a utility operating company subsidiary

The Reality for Utility Operating Companies • Utility companies must optimize their capital structure to minimize their overall marginal cost of capital, i.e., they should minimize their marginal WACC • This approach maximizes the value of the utility operating company • In turn, this maximizes the value of the parent holding company, which tends to be the aggregate of the value of its operating companies • What rational and informed parent holding company knowingly undermines its own value by sub-optimizing its operating company subsidiary’s capital structure?

The Implications of Double Leverage • Artificially overstates financial leverage • Distorts the fair return on equity estimates • Fails to accurately reflect the significance, nature and cost of retained earnings • Reduces the potential efficiencies of a holding company system for the utility operating company and its customers • Undermines the regulatory function: • Hope and Bluefield fair rate of return standards • Creates a disincentive to attract needed capital by systematically under-compensating the investment of that capital.

Conclusions • Hypothetical capital structures are justifiable only if they more accurately reflect a stand-alone utility company’s actual marginal cost of funding • Double leverage does not meet that standard • Double leverage has serious shortcomings, both conceptual and practical • The balance of the professional literature has swung against the validity of the double leverage concept over the past 30 years • Double leverage has largely disappeared from modern regulatory practice