Download

1 / 10

100 likes | 316 Vues

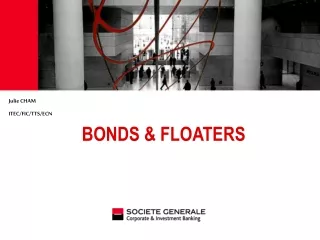

Floaters and Inverse Floaters. Zvi Wiener tel: 02-588-3049 mswiener@mscc.huji.ac.il. 106. 6. 6. 6. 6. 6. 6. 100+L 6. L 1. L 2. L 5. L 0. L 3. L 4. Straight bond. Floater. 0 1 2 3 4 5 6 7. How to treat Floaters.

E N D

Floaters and Inverse Floaters Zvi Wiener tel: 02-588-3049 mswiener@mscc.huji.ac.il http://pluto.mscc.huji.ac.il/~mswiener/zvi.html

106 6 6 6 6 6 6 100+L6 L1 L2 L5 L0 L3 L4 Straight bond Floater 0 1 2 3 4 5 6 7 Floaters, Inverse Floaters

How to treat Floaters • Floater is similar to a constantly renewed loan with fixed spread (!). • Thus the yield of a floater is equal to the yield on the basis plus the spread. • Note that some of the Israeli government bonds have funny linkage to other bonds. Floaters, Inverse Floaters

100+L3 100+L2 100+L1 100+L0 100 100 100 100 Pricing of AA Floaters Cashflow -100 L0 L1 L2 L3 100+ L4 Price • Years • 0 • 1 • 2 • 3 • 4 • 5 100+L4 Floaters, Inverse Floaters

Pricing of Floaters Cashflow -100 L0+D L1+D L2+D L3+D 100+L4+D Fair loan -100 L1+d L2+d L3+d 100+L4+d Difference ?? D-d D-d D-d D-d • Years • 0 • 1 • 2 • 3 • 4 • 5 Floaters, Inverse Floaters

Pricing of Floaters Cashflow -100 L0+D L1+D L2+D L3+D 100+L4+D Fair loan -100 L1+d L2+d L3+d 100+L4+d Difference ?? D-d D-d D-d D-d • Years • 0 • 1 • 2 • 3 • 4 • 5 Two types of duration: index duration and spread duration. Floaters, Inverse Floaters

Reverse (Inverse) Floater • USD 5 year interest rates are 5%, however short term interest rates are Libor =2%. • Libor = London Interbank offered rate • on Bloomberg see FWCV + currency • One can construct so-called reverse floater: Floaters, Inverse Floaters

Inverse Floater bond -100 5 5 5 5 105 loan +100 -L0 -L1 -L2 -L3 -100- L4 bond -100 5 5 5 5 105 Reverse Fl. -100 8 10-L1 10-L2 10-L3 110- L4 • Years • 0 • 1 • 2 • 3 • 4 • 5 Floaters, Inverse Floaters

Duration of inverse floater • Inverse Floater = 2*Bond – Floater • IF = 2*B - F Floaters, Inverse Floaters

See Fabozzi: “The Handbook of Fixed Income Securities”, ch. 14, Floating Rate Securities. • Duration of Floaters, see in T. Bjork, “Arbitrage Theory in Continuous Time”, Ch 15. • Accrual Range, see Accrual Swaps in Hull, “Options, Futures, and Other Derivatives” Ch. 25 Floaters, Inverse Floaters