Download

1 / 49

490 likes | 680 Vues

Market Update and the Road to Value-based Care May 2019 Colorado MGMA PAHCOM Payer Day. Introduction. Jim Hammond Publisher & CEO of The Hertel Report Managing Consultant, Professional Healthcare Solutions Healthplan & Provider Relations Expert

E N D

Market Update and the Road to Value-based Care May 2019 Colorado MGMA PAHCOM Payer Day

Introduction • Jim Hammond • Publisher & CEO of The Hertel Report • Managing Consultant, Professional Healthcare Solutions • Healthplan & Provider Relations Expert • Conference Speaker & Resource to: HonorHealth, AzHHA, AHE, MCMS, HFMA - AZ, CBIZ, ASPA, AMN, HCAA, CMSA, Sonora Quest, Humana, Dignity Health, U of A, CNBC, Money Radio, Wall Street Journal, NPR, Modern Healthcare, Phoenix Business Journal, Arizona Daily Star, Vitalyst Health Foundation, Web AZ, and more • Former AZ HFMA President

The Hertel Report • Trusted & Respected • Impartial & Timely • Solutions Focused • Locally Owned • Weekly News • Monthly Newsletter • Quarterly Data • Networking & Conferences

Agenda • Market Update • Colorado Political moves • Medicaid • Medicare Advantage • Marketplace • Value-based Care Trends • Discussion

Colorado Legislative Update Oil and Gas Regulation Death Penalty Repeal Failed Gun Control - Red Flag Sex Education Reforms Full-day Kindergarten

Polis PrimaveraRoadmap for Saving Money on Healthcare Universal Coverage – Almost There – 6.5% Uninsured Rate State Backed insurance Option – Health Care Cost Savings Act Hospital Prices - HB1004 Reduce Out of Pocket Costs – HB1174 Drive Down Cost of Insurance – HB 1168 Lower RX Costs: Colorado Wholesale Importation of Prescription Drugs Act* Failed Improve Vaccination Rates HB 1168 Addresses • High Premiums • Competition • Rural Access Impact 250K residents Needs $120M state funding Hospital Funding Changed to Include • Limit on Hospital Fees • Hospital Exemptions PASSED State will submit federal waiver

Colorado Medicaid 2013: 740,000 Uninsured 2014: ACA + Expansion Approved 400K Expansion Population By 2015: 39% Reduction in Uninsured April 2019 Colorado Medicaid Population 1.2Million

COLORADO CONSORTIUM FOR PRESCRIPTION DRUG ABUSE PREVENTION National Innovator Colorado Passes Legislation AMA Priorities Expand Rural Treatment Stock Overdose Meds in Public Places Inmate Access to Withdrawal Meds

376,241 MA Lives PLAN MIX 95 HMO Plans 209 Local PPO Plans MA MARCH 2019 UnitedHealthcare: 120K Kaiser: 111K Anthem: 35K Humana: 27K Rocky Mountain HMO: 12K KFF MA Data Spotlight 2019

Regional Accountable Entities (RAEs) • Integrating Physical & Behavioral Healthcare Start: July 2018 Responsible for developing and managing a network of primary care physical health providers and behavioral health providers to ensure access to appropriate care for Health First Colorado members. • All behavioral health providers who want to receive reimbursement for providing services covered by the capitated behavioral health benefit must contract directly with the RAE(s).

Western Colorado Accountable Health Community Model NW CO Community Health Partnership West Mountain Regional Health Alliance Mesa County Public Health Tri-County Health Network Southwest Area Health Educ. Center/San Juan Basin Health Dept. Source: Rocky Mountain Health Plans Presentation

Uninsured Trends (CO vs US) Uninsured Rates: Colorado 2013: 14.1% 2016/2017: 7.5% 2013: 729K 2016: 410K 2017: 414K

Health First Colorado Buy-In Program Premiums Working Adults with Disabilities Ages 16-64 Below 450% FPL Some May Earn More & Qualify Monthly Earnings Max: $9,171 Must Pay Monthly Premiums Based on Income

Objectives of Reform • Reduce Uninsured • Mandates and Exchange/Marketplace • Medicaid Expansion • Bend the Cost/Quality Curve • Value

Healthcare as % GDP Projected https://www.cms.gov/research-statistics-data-and-systems/statistics-trends-and-reports/nationalhealthexpenddata/nhe-fact-sheet.html

Employer and Employee Costs Rising Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits 7

FAILED relationship Fee-For-Service • Cost = Rate x Utilization • Health Plan Cost = Provider Revenue • Health Plan reduces price • Providers incentivized to wait for it…….. Increase Utilization

1992 Risk to Provider Controls Cost Degree of Risk RISK TO PROVIDER

Relationship Responsibility Authority

2018 “The Accountable Care Model” Value based Networks Provider Accountability Risk/reward PROVIDER INCENTIVES EVOLVE Value=Quality/Cost Time

QUALITY MATTERS 47% of Physicians Have Compensation Tied to Quality – 2018 Physicians Foundation CMS: Largest Payer $140M Nationally CMS STAR RATINGS • Who Uses Information on Healthcare Quality? • Consumers & Employers • Physicians & Clinicians • ACOs & VBNs • Policy Makers No Significant Correlation between Consumer Ratings & Quality Performance Scores – Journal of the American Medical Informatics Association 2017 Study

MIPS brings threats of fee schedule cuts and incentives based on MIPS scores • All providers are required to participate in MIPS in 2017, proposed rule • First reporting period 1/1/2017 to 12/31/2017 • Payments adjusted in 2019 based on performance in the 2017 period • MIPS is budget neutral so any incentives are paid for via cuts to other providers • However there is a budget exempt $500 million dollars for “exceptional” performance in the first 5 years The Advisory Board Health Care Cheat Sheet Series MACRA: Educational Briefing for IR Professionals, April 2016 19

How Do We Address Increasing Costs with Inconsistent Outcomes? THE VALUE-BASED NETWORK

Let’s talk about Nomenclature • Accountable Care Organizations – ACO’s are funded by the ACA and specifically address traditional Medicare • Clinically Integrated Networks • Physician Hospital Organizations (System ACO) • Independent Physician Associations • Primary Care • Multispecialty • Single TIN Groups All can be Value-Based Networks

Indicators of Value-Based Networks • Aggregate Providers into Integrated networks • Contract with health plans with rewards tied to triple/quadruple aim • Connect electronically • Track and report quality data • Track and report utilization data • Upside risk agreements (MSSP Basic A&B, Commercial ACO deals) • Upside and downside risk (MSSP Enhanced, Next Gen, spending targets) • PMPM Targets • Percent of Premium • Experienced with episode and population based payment models

Indicators of Value-Based Networks • Aggregate physicians and providers into integrated networks • Contract with carriers or government with rewards tied to triple aim • Connect electronically • Track and report quality data • Track and report utilization data • Upside risk agreements (MSSP ACO Track 1, Commercial ACO deals) • Upside and downside risk (New 2019 ACO models, Next Gen) • PMPM Targets • Percent of premium

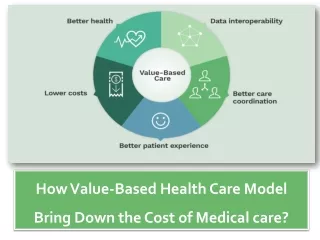

“Transactional Services” • Better relationship between patient and provider • Can uncover multiple conditions leading to better care • Potential to reduce ER Visits and avoidable admissions • Potential to reduce cost of care • Right Services, Right Place, Right Time • Increased Revenue Potential for Risk Entity (Appropriate RAF scoring) • Increased Revenue Opportunity for Providers • Health Risk Assessments • Gaps in care • Medication reconciliation • Attestations • CCM • 99490, 99487, 99489 • TCM • 99495, 99496 = WIN for the Patient, Win for the Provider, Win for the Payor Targets the triple aim: Better Care, Better Patient Experience, Lowers the Cost of Care

Value-based Model OON/OOA No Benefits OON/OOA Healthplan Network Reduced Benefits Healthplan Network • Can be • System • Independent • Owned • Affiliated Networked • Share • Values • Information • Measurement • Risk ”Value Network” Best Benefits ”Narrow Network” Value Based Network

Narrow / High-Performing Networks There is a pronounced shift from broad PPO networks to narrow / high-performing networks in Arizona. • High performing physicians and facilities • Combination of lower unit costs, lower total medical costs through elimination of waste and improved care patterns and value (vs volume) based reimbursement methods • Not there yet – slowly moving away from fee-for-service contracts. • Challenges • Geographic coverage • Experience with risk, reserves

Pressure on Physicians • Non-traditional Competition • Regulations • Quality Measures • Utilization Scrutiny • Rate Pressure • Investment in Technology • Alliance/ACO

Investment in Technology Improve Electronic Integration • Consumer Experience • Waste and Fraud • Manage attribution • Support transparency • Monitoring, Reporting, Analytics

The Triple Quadruple Aim • Improving the patient experience of care (including quality and satisfaction), known as Patient Experience • Improving the health of populations, known as Population Health • Reducing the per capita cost of health care, known as Cost of Care • Improving the work life of health care providers, clinicians and staff, known as Provider Well-Being

Healthcare, A Call To Action OUTCOMES Patient Experience Patient experience Cost Outcomes Outcomes Physician experience Cost

Provider Measurements 3 Scores MeasurementMaximum Score • Cost 10 • Quality 10 • Patient Satisfaction 10

Considerations/Success Factors • Team Approach • Think Long Term • Learn from Performers • Prepare to Deal with Purchasers • True Clinical Integration • Transparency • Competition • Reduced Variation • Physician Leadership • Utilization Scrutiny • Investment in Technology

Bending the Cost Curve TRI LL IONS The Bent curve

The Pain Consumer TRILLIONS THE PAIN Physicians Employer Insurance Co

Winston Churchill “We can always count on the Americans to do the right thing, after they have exhausted all other possibilities”

John F. Kennedy “We should to go to the moon in this decade and do these other things not because they are easy but because they are hard.”

Provider-Healthplan Relationship ConsultingStrategic Planning

Please visit our website at: www.thehertelreport.com Be part of our membership community and sign up today for timely, impartial market news, data and exclusive reports!