Download

1 / 68

680 likes | 699 Vues

Learn the benefits of managing money, set goals, build a budget, stay on track, and save money. Determine your financial goals, differentiate between needs and wants, allocate your budget wisely, and review your finances regularly. Gain practical money-saving tips and access resources for financial guidance.

E N D

Budgeting For Your Life Presented by Erica Modaffari

What We Will do Today • Understand the benefits of money management • Set goals • Discover the Four-Step Plan to building a budget • Learn ways to stay on track • Share practical money saving tips

Why Do I Need a Budget? Havinga budget helps you . . . • Decide where your money goes • Make informed choices • Determine if you’re living within your means • Develop a savings plan • Control your financial future • Have peace of mind

Determine your Goals: • Short-term (within the next six months) • Intermediate-term(within the next one to five years) • Long-term(more than five years away)

Your Budget It starts with two key components: • Income • Expenses

Step 1: List All Income Sources Paycheck Savings Dividends Gifts Interest Tax refund Pension Other Social Security Rental income Bonus Child support/alimony

Step 2: Determine Monthly Expenses • Fixed (housing, car payment, internet) • Flexible (food, clothes, utilities, gifts) • Periodic (insurance, taxes, car registration)

Needs Vs. Wants Needs: Wants: • Something that is desired. • There may be unlimited wants, but limited resources. As a result, one cannot have everything one wants and must look for the most affordable alternatives. • Necessary for a person to live a healthy life. • Needs are essential or very important to live your life.

Needs • Housing • Mortgage, rent • Food • groceries vs. eating out • Utilities • water, trash, electricity, gas • Clothing

Needs • Transportation • car payment, gas, maintenance, insurance • bus pass • Technology • internet, phone • Medical expenses • insurance/out of pocket • doctor visits • medications • exercise

Suggested Allocations • Donations 10-15% • Savings 5-10% • Housing 25-35% • Utilities 5-10% • Food 5-15% • Transportation 10-15% • Clothing 2-7% • Medical/Health 5-10% • Personal 5-10% • Recreation 5-10% • Debts (remaining) 23% Each penny has a place! You are telling your money how to work for YOU!

Step 3: Balance Income & Expenses How does your cash flow? Goal: Match income with expenses If expenses > income = make changes! If income > expenses = save more!

Where Does Your Money Go?The little things add up… If you bought a soda/water every day for $1.50 The soda will cost you… • - $10.50 per week • - $45 a month • - $547.50 a year

Car Purchasing Tip • Should pay less than half of your annual income • Loses 70% of value in the 1st 4 years

Step 4: Review • Continue to track expenses • Update your budget monthly • Find places to save (cut spending) • Does your plan fit with your goals or have your goals changed?

Top 12 Practical Money-Saving Tips Consider yourself a creditor Pay down debt Refinance mortgage Bundle insurance with one company Shop around for insurance and credit Use credit cards wisely-Only charge what you can pay in full-Eliminate late payment fees; pay on time-Understand terms and conditions

Top 12 Practical Money-Saving Tips Send in rebates and use coupons Don’t go grocery shopping when … Bring your lunch Drive sensibly to save on gas or even walk/bike Make saving a habit: Payroll direct deposit Automatic withdrawal Save one year’s raise Ask, “Do I really NEED this?”

Bonus Money Saving Tip Start a change jar

Resources Noble Credit Union www.NobleCU.com Feed the Pig – Consumer Education Site www.feedthepig.org National Credit Union Administration – Consumer Microsite www.mycreditunion.gov ClearPoint Credit Counseling Solutions www.clearpointcreditcounselingsolutions.org US Department of Energy www.energy.gov www.fueleconomy.gov Annual Credit Report www.annualcreditreport.com

What We Learned Today How proper money management will enhance your everyday life The Four-Step Plan to building a budget Tips to keeping your financial plan on track Practical money saving tips

Remember … Noblecredit union can help you with all your financial needs. Erica Modaffari Community Relations Specialist Noble Credit Union (559) 451- 2392 EricaM@NobleCU.com

Budgeting For Your Life Presented by Erica Modaffari

Budgeting For Your Life Presented by Erica Modaffari

Budgeting For Your Life Presented by Erica Modaffari

Budgeting For Your Life Presented by Erica Modaffari

Budgeting For Your Whole Life Presented by Erica Modaffari

Slide Title Text goes here

What We Will do Today • Understand the benefits of money management • Set goals • Discover the Four-Step Plan to building a budget • Learn ways to stay on track • Share practical money saving tips

What We Will do Today • Understand the benefits of money management • Set goals • Discover the Four-Step Plan to building a budget • Learn ways to stay on track • Share practical money saving tips

What We Will do Today • Understand the benefits of money management • Set goals • Discover the Four-Step Plan to building a budget • Learn ways to stay on track • Share practical money saving tips

What We Will do Today • Understand the benefits of money management • Set goals • Discover the Four-Step Plan to building a budget • Learn ways to stay on track • Share practical money saving tips

Determine your Goals: • Short-term (within the next six months) • Intermediate-term(within the next one to five years) • Long-term(more than five years away)

Determine Your Goals Short-term • Within the next six months Intermediate-term • Within the next one to five years Long-term • More than five years away

Step 1: List All Income Sources Paycheck Savings Dividends Gifts Interest Tax refund Pension Other Social Security Rental income Bonus Child support/alimony

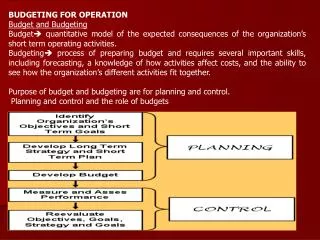

Today’s Topics 1 2 3 4 Balance the two Review Incomesources Determine expenses

1 Your Income Sources Paycheck • Dividends • Interest • Pension • Social Security • Rental income • Bonus • Child support and alimony • Savings • Gifts • Tax refund • Other

Step 2: Determine Monthly Expenses • Fixed (housing, car payment, internet) • Flexible (food, clothes, utilities, gifts) • Periodic (insurance, taxes, car registration)

2 Fixed • Housing, car payment, internet Flexible • Food, clothes, utilities, gifts Periodic • Insurance, taxes, car registration) Determine Monthly Expenses

Suggested Allocations • Donations 10-15% • Savings 5-10% • Housing 25-35% • Utilities 5-10% • Food 5-15% • Transportation 10-15% • Clothing 2-7% • Medical/Health 5-10% • Personal 5-10% • Recreation 5-10% • Debts (remaining) 23% Each penny has a place! You are telling your money how to work for YOU!