Download

1 / 74

770 likes | 1.14k Vues

VALUATION OF FIXED INCOME SECURITIES OR VALUATION OF BONDS. Dr. U. Husain. Structure Introduction Bond valuation Valuation model Bond return Price-yield relationship Bond market The term structure of interest rate (yield curve) Riding the yield curve Duration Immunization.

E N D

VALUATION OF FIXED INCOME SECURITIES ORVALUATION OF BONDS Dr. U. Husain

Structure • Introduction • Bond valuation • Valuation model • Bond return • Price-yield relationship • Bond market • The term structure of interest rate (yield curve) • Riding the yield curve • Duration • Immunization

Introduction Fixed income financial instruments: • Traditionally identified as a long-term source of funds for a corporate enterprise are the cherished conduit for investor’s money. • An assured return and high interest rate are responsible for the preference of bonds over equities.

Types of Bonds Financial institutions, banks and corporate bodies are offering attractive bonds like: • Retirement bonds, Education bonds, Deep discount bonds, Encashbonds, Money multiplier bonds and index bonds.

Knowing how to value fixed income securities (bonds) is important both for investors and managers. (Such knowledge is helpful to the former in deciding whether Investor should buy or sell or hold securities at prices prevailing in the market.)

Bond Issuing Authorities A bond or debenture is a debt instrument issued by the: • Government • Public sectors • Corporations (business enterprise)

valuation of bonds In order to understand the valuation of bonds, we need to be familiar with certain bond-related terms. • Par Value- It is the value stated on the face of the bond. It represents the amount the firm borrows and promises to repay at the time of maturity. Usually the par or face value of bonds issued by business firms is $ 100. Sometimes it can be $ 1000.

Coupon Rate and Interest- A bond carries a specific interest rate which is called the coupon rate. The interest payable to the bond holder is simply par value of the bond x coupon rate. Most bonds pay interest semi-annually. For example, a GOI security which has a par value of $ 1000 and a coupon rate of 11 per cent pays an interest of $ 55 every six months.

Maturity Period- Typically, bonds have a maturity period of 1-10 years; sometimes they have a longer maturity. At the time of maturity the par (face) value plus perhaps a nominal premium is payable to the bondholder.

Example: A company issues 1,000, 10% Educational Bond @ $100 each. Par value; $ 100. Coupon Rate: 10% Maturity Value: $100

The time value concept • The time value concept of money is that the dollar received today is more valuable than a dollar received tomorrow. • Future Value = present value (1 + interest rate). Example: If hundred dollars are put in a savings account in a bank for one year, the future value of money will be: Future Value = $ 100 (1.0 + 6%) = 100 x 1.06 = $ 106.

If the deposited money is allowed to cumulate for more than one time, the period exponent is added to the previous equation. Future value = (Present Value) (1 + interest rate)t • n- the number of periods the deposited money accumulates as interest. Example: Suppose $ 100 is put for two years at the 6% rate of interest, money will grow to be $ 112.36. Future Value = Present value (1 + interest rate)2 = 100 (1 + 0.06) = 100 (1.1236) = 112.36. • To find out the values in a simple manner, the compound sum of $1 at the end of a period FVIF1,/r, tand compound sum of an annuity of $ 1 per period FVIFA tables are given in the appendix.

The present value The present value of money can be found simply by reversing the earlier equation. Present value x (1 + interest rate) = Future value Present value = Future value 1+ interest rate Here, the discounting principle is used. Today’s worth of $ 100 to be received after a year at 10 per cent interest would be: Present value = Future value 1+ interest rate = 100 = 100 = $ 90.90 1+ 0.10 1.10 The multiple period of present value equation takes into account of the multiple periods. Future value____ Present value = (1 + interest rate)n

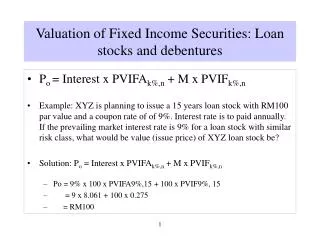

Bond Valuation model Determining the value of a bond requires: • An estimate of expected cash flows • An estimate of the required return. To simplify the analysis of bond valuation we will make the following assumptions: • The coupon interest rate is fixed for the term of the bond. • The coupon payments are made every year and the next coupon payment is receivable exactly a year from now. • The bond will be redeemed at par on maturity.

The Formula for valuation of a bond is: P = C x PVIFA r X n + M x PVIF rX t Where, P = value (in dollar) n = number of years C = annual coupon payment (in dollar) r = periodic required return (i= Rate of Interest) M = maturity value t = time period when the payment is received.

For Example:How to compute the value of a bond? Consider a 10-year, 12 %coupon bond with a par value of $ 1000. Let us assume that the required yield on this bond is 13%. The cash flows for this bond are as follows: • 10 annual coupon payments of $ 120. • $ 1000 principal repayment 10 years from now. • The value of the bond is: • P = 120 x PVIFA 13X10+ 1,000 x PVIF 13X10 • = 120 x 5.426 + 1000 x 0.295 • = 651.1 + 295 = $ 946.1 Use Alternative Formula?

Bond values with semi-annual interest Most bonds pay interest semi-annually. To value such bonds, we have to work with a unit period of six months, and not one year. This means that the bond valuation equation has to be modified along the following lines: • The annual interest payment, C, must be divided by 2 to obtain the semi- annual interest payment. • The number of years to maturity must be multiplied by two to get the number of half-yearly periods. • The discount rate has to be divided by two to get the discount rate applicable to half-yearly period.

With the above modifications, the basic bond valuation becomes: P = C/2 (PVIFAr/2, 2n) + M (PVIFr/2,2n) (10.2) Where, P = value of the bond C/2 = semi-annual interest payment r/2 = discount rate applicable to a half-year period M = maturity value 2n = maturity period expressed in terms of half- yearly periods. Same changes will come in Alternative Formula.

Example:Consider a 8-year, 12 per cent coupon bond with a par value of $ 100 on which interest is payable semi-annually. The required return on this bond is 14 percent. Solution: P = C x PVIFA r X n + M x PVIF r X t = 6 (PVIFA7%, 16 yr) + 100 (PVIF7%, 16 yr) = $ 6 (9.447) + $ 100 (0.388) = $ 95.5 Please use alternative formula?

Bond return Holding period return- An investor buys a bond and sells it after holding for a period. The rate of return in that holding period is: Price gain or loss during the holding period + Coupon interest rate, if any Holding period return = ____________________________ Price at the beginning of the holding period The holding period rate of return is also called the one period rate of return. This holding period return can be calculated daily or monthly or annually. If the fall in the bond price is greater than the coupon payment the holding period return will turn to be negative.

Example: (a) An investor ‘A’ purchased a bond at a price of $ 900 with $ 100 as coupon payment and sold it at $ 1000. What is his holding period return ? Solution: Holding period return= Price gain + Coupon payment Purchase price 100 + 100 = 200 = 0.2222 900 900 Holding period return = 22.22%

(b) If the bond is sold for $ 750 after receiving $ 100 as coupon payment, then what is the holding period return? Holding period return= Price gain + Coupon payment Purchase price -150 + 100 = -50 = -0.0555 900 900 Holding period return = -5.55%

Current Yield The current yield is the coupon payment as a percentage of current market prices. Current yield = Annual coupon payment Current market price The current yield is the differs from the coupon rate, since the market price differs from the face value of the bond. When the bond’s face value and market price are same, the coupon rate and the current yield would be the same. For example, when the coupon payment is 8% for $ 100 bond with the same market price, the current yield is 8%. If the current market price is $ 80 then the current yield would be 10%.

Yield to maturity Yield to maturity is the total return that will be earned by someone who purchases a bond and holds it until its maturity date. The yield to maturity might also be referred to as yield, internal rate of return, or the market interest rate at the time that the bond was purchased by the investor. The yield to maturity is expressed as an annual percentage rate. https://www.accountingcoach.com/blog/what-is-yield-to-maturity

let's assume that a 5% $100,000 bond will mature in 5 years and will pay interest each June 1 and December 1. Hence the bond will pay interest =100,000X(.05)X(1/2) = $2,500 every six months until it matures.

If the current market interest rate for this type of bond is 6%, the bond's current market value will be less than $100,000. The market value of a 5% bond in a 6% bond market will be approximately $95,735. This is the present value of the $2,500 of interest that will be received every six months for 5 years plus the present value of the $100,000 that will be received at the end of 5 years. Any difference in the re-investment rate will cause a difference between the actual return and the YTM. In this sense, the YTM is only a measure of yield. It cannot be regarded as a measure of return from a coupon-paying bond.

Example: A Ten-year bond with the 9% coupon rate and maturity value of $ 1000 is currently selling at $ 887. What is its yield to maturity?

Alternative Formula: YTM = C + (P or D/years to maturity) (Po + F) / 2 YTM= Yield to maturity C = Coupon interest P or D = Premium or discount Po = Present value F = Face value

Zero Coupon Bonds (ZCB) • The YTM concept has a slightly different meaning for Zero Coupon Bonds (ZCB), popularly known as Deep Discount Bonds (DDB). • ZCBs do not carry any coupon but • Issued at a price discounted to the face value. • On maturity, these bonds are redeemed at face value. • Since these bonds do not have any coupon payments during the life of the bond, the question of re-investment of coupon payments does not arise at all.

Price-yield relationship Bond prices and yields Price move in opposite directions, which you may find confusing if you're new to bond investing. Bond Prices and yields act like a Yield seesaw: when bond yield go up, prices go down, and when bond yields go down, prices go up.

Relationship between bond price and time • Bond prices, generally, change with time as the price of a bond must equal its par value at maturity (assuming that there is no risk of default). For example, a bond that is redeemable for $1000 (which is its par value) after 5 years when it matures, will have a price of $ 1000 at maturity, no matter what the current price is?

Relationship between coupon rate, required yield, and price • Coupon Rate < Required yield Price < Par (Discount bond) • Coupon Rate = Required yield Price = Par • Coupon Rate > Required yield Price > Par (Premium bond)

Realized yield to maturity Assumption: The YTM calculation assumes that the cash flows received through the life of a bond are reinvested at a rate equal to the yield to maturity. This assumption may not be valid as reinvestment rate/s applicable to future cash flows may be different. It is necessary to define the future reinvestment rates and figure out the realized yield to maturity.

For Example: A $1000 par value bond, carrying an interest rate of 15 per cent (payable annually) and maturing after 5 years. The present market price of this bond is $ 850. The reinvestment rate applicable to the future cash flows of this bond is 16 per cent. The future value of the benefits receivable from this bond, calculated in bellow, works out to $ 2032.

Bond market The bond market is a financial market where participants can issue new debt, known as the primary market, or buy and sell debt securities, known as the secondary market. This is usually in the form of bonds, but it may include notes, bills, and so on.

The term structure of interest rate (yield curve) The bond portfolio manager is often concerned with two aspects of interest rates; the level of interest rate and the term structure of interest rate. The relationship between the yield and time or years to maturity is called term structure(yield curve). The general reception is that the curve will be upward moving up to a point then it becomes flat. This is indicated in the following Figure

There are at least three competing theories that attempt to explain the term structure of the interest rates. • Expectation theory, • Liquidity preference theory and • Preferred habitat or segment theory

Expectation theory The theory was developed by J.. Hicks (1939), F. Lutz (1940) and B. Malkiel (1966). A rising yield curve • indicates that the investors’ expectation of a continuous rise in interest rate. The flat yield curve (b) means that the investors expect the interest rate to remain constant. The declining yield curve (c) shows that the investor expects the interest rate to decline.

Liquidity preference theory “Keynes describes the liquidity preference theory in terms of three motives that determine the demand for liquidity”(Tobin, J. 1958). • The transactions motive: states that individuals have a preference for liquidity in order to guarantee having sufficient cash on hand for basic day-to-day needs. In other words, people have a high demand for liquidity to cover their short-term obligations, such as buying groceries, and paying rent or the mortgage. Higher costs of living mean a higher demand for cash/liquidity to meet those day-to-day needs. https://www.investopedia.com/terms/l/liquiditypreference.asp

The precautionary motive: relates to individuals' preference for additional liquidity in the event that an unexpected problem or cost arises that requires a substantial outlay of cash. These include unforeseen costs like house or car repairs. • The speculative motive: Individuals may also have a speculative motive. When interest rates are low, demand for cash is high as individuals prefer to use the cash or hold onto it until interest rates rise.

Keynes’ liquidity preference theory as advocated by J.R. Hicks (1939) • Liquidity preference theory suggests that an investor demands a higher interest rate, or premium, on securities with long-term maturities, which carry greater risk, because all other factors being equal, investors prefer cash or other highly liquid holdings. Investments that are more liquid are easier to sell fast for full value. According to the liquidity preference theory, interest rates on short-term securities are lower because investors are not sacrificing liquidity for as long as they would be with medium- to longer-term securities.

Segmentation theory Segmentation theory is stated that long and short-term interest rates are not related to each other. It also states that the prevailing interest rates for short, intermediate, and long-term bonds should be viewed separately like items in different markets for debt securities.

Riding the yield curve • Riding the Yield Curve is a trading strategy that involves buying a long-term bond and selling it before it matures so as to profit from the declining yield that occurs over the life of a bond. Investors hope to achieve capital gains by employing this strategy.