Download

1 / 20

200 likes | 230 Vues

If you are into food business with revenue below 20 Lakhs, you must obtain an FSSAI Registration before starting operations. Corpseed can help you to obtain FSSAI registration for your business. Money back guarantee. Get free consulting<br>Kindly Visit: https://bit.ly/2wKV6Rj

E N D

Looking for something else? Search NON-BANKING FINANCIAL COMPANY (NBFC) REGISTRATION NBFC Registration 600000 (20% Off On 750,000) + Govt. Expenses APPLY NOW Incorporation of company under the company act (ROC). Fintech Lending Business Market & Product Research Short-Term, Medium-Term & Long-Term Business Plan Loan Syndication Advisory Technology Advisory Hi there, Tal

Takeover of NBFC 650000 650000 + Govt Exp APPLY NOW Due diligence of Acquiring Company Amendments & Appointment of new board of directors Fintech Lending Business Market & Product Research Short-Term, Medium-Term & Long-Term Business Plan Loan Syndication Advisory Technology Advisory Annual Compliance 170000 170000 APPLY NOW Annual Filing for Companies Prepare or revision of Annual Balance Sheet

Preparation and Filing of Annual Return Preparation and Filing of Income Tax Return Annual Compliance Management Communication with RBI INTRODUCTION TO NBFC’S Non-banking financial companies (NBFCs) are evolving as a vital part of the Indian financial system. NBFC’s have multiplied in large numbers and varying types since the financial crisis of 2007-08, playing a key role in meeting the credit demands unmet by the traditional banks, specifically focusing on peer to peer lending. It is a Company registered under the Companies Act (other than commercial and co-operative banks), engaged in the business(es) of providing credit facilities like loans & advances, accepting deposits, leasing, hire purchase, retirement planning, facilitating securities trade and money market trade, merger activities, underwriting facilities etc. They raise funds from the public, directly or indirectly (from other commercial or co- operative banks) and provide credit or loan facilities to the ultimate spenders. They provide loans and advances and other credit facilities to small, micro and medium scale industries and individual business persons. Thus, they have widened the spectrum and array of products and services offered by the financial sector. Progressively, NBFC’s are gaining increasing recognition due to their customer-oriented services; flexible

products, abridged procedures; better rates of return on deposits; flexibility and timeliness in meeting the credit needs of the seekers of credit; etc. NBFCs are regulated by the Reserve Bank of India(RBI) within the framework of the Chapter IIIB of the Reserve Bank of India Act, 1934 and any rules made thereunder or any directions issued by it under the Act. RBI Act defines an NBFC as: A Company Registered under the Companies Act; A company which is engaged in the business of providing credit facilities like loans and advances, acquisition of securities and debt instruments or other marketable securities of a like nature, leasing, hire-purchase, insurance business, chit business. A non-banking institution which is a company registered under the Companies Act and has the principal business of accepting deposits under any scheme or arrangement in one lump sum or in installments by way of contributions or in any other manner is also a non-banking financial company (Residuary non- banking company) within the meaning of this Act. However, as per the RBI act following categories do not fall under the purview of an NBFC: Any institution whose principal business comprises of agricultural activities Any institution whose principal business comprises of industrial activity Any institution whose principal business comprises of purchase or sale of any goods (other than securities) Any institution whose principal business comprises of providing any services and sale/ purchase/ construction of immovable property. FINANCIAL ACTIVITY as “Principal Business” implies that financial assets of the Company shall constitute more than 50% of the total assets of the Company and income from such Financial assets shall constitute more than 50% of the gross revenue of the Company NBFC’s ARE DIFFERENT FROM A BANK Activities of an NBFC are similar to that of a bank, however, there are some differences between the two as stated below: An NBFC cannot accept demand deposits; NBFC’s are not a part of the payment and settlement system NBFC cannot issue cheques drawn on itself; Unlike a bank, Deposit insurance facility is not available to the depositors of NBFCs.

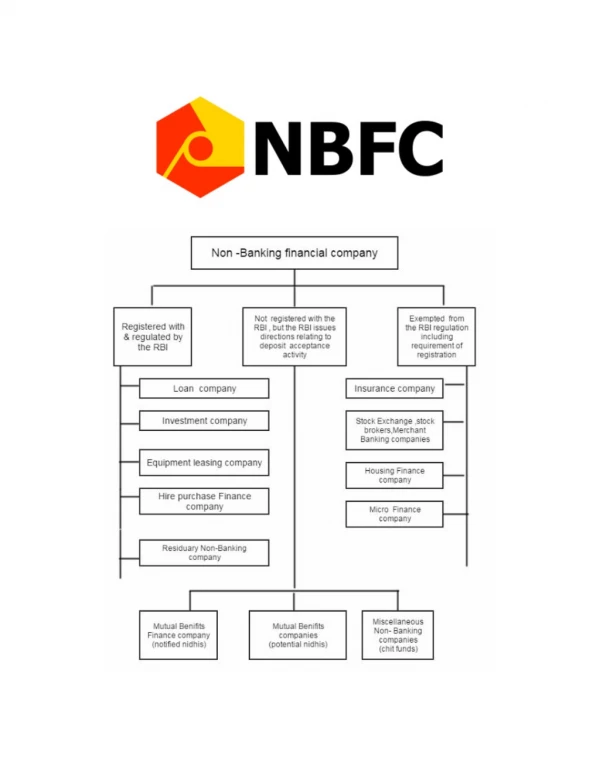

REQUIREMENTS FOR REGISTRATION OF AN NBFC An NBFC should: Be a Company registered under the Companies Act; Should have a minimum net owned fund of INR 2 Crores; There is a specialized Net Owned Fund requirement for specialized categories of NBFC’s NBFC REGISTRATION PROCESS In order to establish a financial institution in any of the aforementioned categories, a registration number has to be mandatorily received from the Reserve Bank of India. For the purpose of registration of an NBFC an application is to be submitted in the prescribed along with the necessary attachments with the RBI for its perusal. On being satisfied that the provisions of the RBI Act have been complied with A CERTIFICATE OF REGISTRATION is issued to the institution. It is imperative to fulfill the following prerequisites for obtaining a certificate of registration of NBFC from RBI: The applicant must be a Company registered under the Companies Act for the time being in force The Company shall have a minimum NOF (Net Owned Funds) of INR 2 Crores for an Indian entity and INR 5 Crores for a foreign Company or investors who wish to set up an NBFC in India. At least one of the directors who should be Whole-Time Director of the Company should possess an experience in a similar field or should be an experienced banker. The CIBIL records of the Company should be free from any irregularities. On satisfaction of the aforementioned essentials, the Company should for its registration as NBFC in the form prescribed by the RBI along with all the mandatory documents and attachments. This application (COSMOS) can be filled on the website of RBI. On Successful submission of the application, an application reference number (CARN) is issued by the RBI to the applicant for the purpose of tracking the status of its application. Once, the CARN is obtained a physical copy of the application along with all the attachments should also be submitted with the branch of RBI having jurisdiction over the location of the registered office of the applicant. Once the application is received by the respective office the license of registration of NBFC is granted by the RBI on comprehensive and careful analysis of such application CLASSIFICATION OF NBFC’S

CLASSIFICATION OF NBFC S NBFC’S CLASSIFICATION ON THE BASIS OF ACTIVITY ASSET FINANCE COMPANY(AFC) [DEPOSIT TAKING NBFC] As per RBI, any NBFC can act as an AFC, subject to the condition that the income arising from the aggregate of physical assets supporting its economic activity is not less than 60% of its: i. Total assets; and ii. Total income respectively. Once the company satisfies this condition it can visit the regional office having jurisdiction over the place of registered office of the Company along with their certificate of registration as issued by the bank to get registered as an asset finance companies. Principal Business of an Asset Finance Company (AFC) is comprised of the following 2 activities: Financing of physical assets that correspond to productive or economic activity such as plant or machinery, automobile, material, equipment, power generators, etc. The act of pledging assets Viz. Bills of exchange, short-term inventories or investments to borrow funds in the form of loan or cash. This type of financing is used when a person is seeking short-term borrowing for working capital needs. 2. INVESTMENT COMPANY (IC) OR (NBFC-IC) [DEPOSIT TAKING NBFC] An Investment Company which is a financial institution registered with RBI is a type of NBFC engaged in the activity of acquisition of shares, stock, bonds, debentures or securities. These kinds of NBFC cannot deal in

y q the investments they hold. Services of this kind of NBFC is helpful in starting a Venture Capital Fund or a Private Equity Business. 3. SYSTEMICALLY IMPORTANT CORE INVESTMENT COMPANY (CIC-ND-SI) [DEPOSIT TAKING NBFC] A CIC-ND-SI is a type of Investment Company which carries on the business of acquisition of shares and securities is recognized as a Systematically important core investment if it fulfills the following conditions: At least 90 percent of the NBFC’s total assets should be in the form of investments in equity shares, preference shares, loan or debt in its group companies. The investment in equity shares, including all securities or instruments convertible into equity within a period of not more than ten years from the date of issue, in the group companies, shouldn't be less than 60% of its total assets. The NBFC does not trade in securities or Loans of its group companies. The only exception to this is if such trading is done through a block sale place in the event of dilution or disinvestment. The company shall only carry the activities of investment in bank deposits, government securities, money market instruments, loans and investment in debt securities or guarantees on behalf of group companies. The minimum Asset Size of such NBFC should be Rs 100 Crore. This kind of NBFC can accept public funds. 4. LOAN COMPANIES (LC) [DEPOSIT TAKING NBFC] A Loan Company is a financial institution registered under the Companies Act whose principal business is providing loans and advances. 50% of the assets of this kind of NBFC must be in lending and 50% of the total income of such income shall arise from the aforesaid assets. 5. INFRASTRUCTURE FINANCE COMPANY (IFC) [NON-DEPOSIT TAKING NBFC] The Infrastructure Finance Company is a type of NBFC engaged in the principal business of providing infrastructure loan. The credit facility(ies) (term loans, project loans, etc.) granted by this kind of NBFC’s to the borrowers in the specific infrastructure sectors Viz. Transport, Energy, Water and Sanitation, Communication, and Social and Commercial Infrastructure are referred to as the Infrastructure Loans. As per RBI, any NBFC can be registered as an Infrastructure Finance Company, subject to the condition that it should be a non-deposit accepting - loan company and must fulfill the following conditions: Minimum 75% of the total assets of the NBFC should be deployed in the infrastructure loans. The minimum net worth of the Company should be Rs 300 Crore. The CRAR (capital to risk-weighted asset ratio) of the company should be at least 15% with i i Ti I i l 10%

minimum Tier-I capital at 10%. The minimum credit rating of the Company should be “A” or equivalent of CRISIL, or equivalent to any other Credit rating agencies. 6. INFRASTRUCTURE DEBT FUND (IDF-NBFC) [NON-DEPOSIT TAKING NBFC] A debt fund is a pool in which core assets are investments with fixed returns. This type of funds is vital because of the fact that investment/funding in infrastructure sector is complex as compared to other types of funding because of the volume of investment(s) required, long maturity period and period of funds required. In India, and IDF can be set up as a trust or a fund. If it is set up as a trust then it shall be mutual fund and shall be governed by the provisions of SEBI. Such funds are called IDF-MF and would issue rupee- denominated bonds of minimum 5-year maturity for the purpose of raising funds infrastructure projects. If IDF is set up as a Company, it would be categorized as an NBFC and shall be governed by the relevant provisions of RBI. Infrastructure Debt fund is a non-deposit taking NBFC having a net owned fund of Rs 300 Crores of mores. IDF-NBFC provide long-term debt to infrastructure projects. This type of NBFC’s usually raise resources through currency bonds of five years or more and invests majorly in Public-Private Partnerships and in post-commencement operations date (COD) infrastructure projects which have completed at least 1 year of satisfactory commercial operation. 7. NON-BANKING FINANCIAL COMPANY – MICROFINANCE INSTITUTION (NBFC- MFI) [NON-DEPOSIT TAKING NBFC] NBFC-MFI is another type of non-deposit taking NBFC which provides short-term credit facilities to low- income groups. An NBFC can be categorized as an NBFC-MFI subject to the following conditions: A minimum of 85% of the assets of such institution is in the form of microfinance Such Microfinance shall be provided subject to the following conditions: In rural areas, Loans should be given to people with income of Rs. 60000/- IN urban areas, Loans should be given to people with income of Rs. 120000/- Such loans should not exceed Rs. 50000/- The tenure of such loans should not be less than 24 months Such loans should be given without collaterals The borrower should be given the choice of repayment on a weekly, fortnightly or monthly basis 8. NON-BANKING FINANCIAL COMPANY – FACTORS (also known as NBFC- FACTORS) [NON-DEPOSIT TAKING NBFC] NBFC-Factors to finance institution having the principal business of acquisition of receivables on discount or

financing against such receivables by way of loans or advances or by the creation of security interest over such receivables but excludes normal lending by a bank. As per RBI, any NBFC can be registered as an Infrastructure Finance Company, subject to the condition that it should be a non-deposit accepting - loan company and must fulfill the following conditions: Minimum 75% of the total assets of the NBFC should be deployed in the factoring business. Minimum 75% of the gross income of such NBFC shall be from factoring business The minimum net worth of the Company should be Rs 5 Crores. POST REGISTRATION GUIDELINES On receipt of the Certificate of Registration the NBFC are subject to certain guidelines as modified by the RBI from time to time: Deposits payable on demand should not be accepted by them. The public deposits should be for a minimum period of 12 months and for a maximum period of 60 months Accepted by them Interest rates offered should not be higher than the ceiling rate prescribed by RBI from time to time. No additional benefits should be offered to the depositors like gifts or incentives. The NBFC’s have to get its credit rating done from a credit rating agency in every 6 months and shall ensure that it possesses at least an investment grade rating . RBI does not guarantee the repayment of amount/deposits taken by the NBFC’s All material information including any changes in the composition of the Company has to be furnished to the RBI. Deposits taken by the NBFC shall be unsecured. Audited Balance sheet and annual financials of the Company shall be submitted with the RBI annually. A return stating the deposits taken by the Company shall also be furnished with the RBI annually. A return stating the liquid assets of the company has to be furnished with the RBI Quarterly. A certificate stating that the company is in a position to pay back all the deposits or money taken from the Public shall be obtained from the auditors and submitted with the RBI. A half-yearly return has to be furnished by the company having Public Deposits of INR 20 Crores or more or assets of Rs. 100 Crores or more. Company shall maintain at least 15% of the public deposits as liquid assets.

LIST OF COMPLIANCE ON BASIS OF PERIODICITY NBFC MONTHLY COMPLIANCES FORM NAME PURPOSE OF THE FORM DEPARTMENT SUBMITTED BY ALL NON -DEPOSIT TAKING NBFCS Monthly Return Monthly Return on NBFC -ND SI with asset size of Rs.100 CR. & RBI above NBS_ALM 1 Statement of Short term dynamic liquidity to be filed within 10 RBI days of closer month TO BE SUBMITTED BY ALL DEPOSIT TAKING NBFC’S HAVING: ASSET SIZE ABOVE RS. 100 CRORES OR PUBLIC DEPOSITS OF RS. 20 CRORES AND ABOVE NBS 6 Monthly Return stating Exposure to Capital Market RBI NBFC QUARTERLY COMPLIANCES FORM NAME PURPOSE OF THE FORM DEPARTMENT TO BE SUBMITTED BY ALL DEPOSIT TAKING NBFC’S EXCEPT RESIDUARY NBFC: NBS 1 Quarterly Return on Material Financial Parameters of Deposit RBI Taking NBFCs NBS 2 Quarterly Statement of Capital Funds, Risk Assets/Exposures and RBI risk assets Ratio. NBS 2: CA & Certifying NBS 2 RBI CEO Cert. NBS 3 Quarterly Return on Statutory Liquid Assets RBI TO BE SUBMITTED BY ALL RESIDUARY NON -BANKING COMPANIES: NBS 3A Quarterly Return on Statutory Liquid Assets RBI Quarterly Return of investments RBI Return I SUBMITTED BY ALL NON-DEPOSIT TAKING NBFCS NBS -7 Quarterly Statement of Capital Funds, Risk Weighted Assets and RBI risk assets Ratio etc. NBS -7: SA & Certifying NBS -7 RBI CEO Cert. SUBMITTED BY NBFCS HAVING ASSET SIZE BETWEEN 50 - 100 CR. Quarterly Quarterly Return by NBFC- ND with asset size of Rs.50 100 Cr. RBI

Return SUBMITTED BY ALL SECURITISATION AND RECONSTRUCTION COMPANY SCRC Quarterly statement of assets acquired/ securitized/ RBI reconstructed NBFC HALF YEARLY COMPLIANCES FORM NAME PURPOSE OF THE FORM DEPARTMENT TO BE SUBMITTED BY ALL DEPOSIT TAKING NBFC’S HAVING ASSET SIZE RS. 100 CRORES or more OR PUBLIC DEPOSITS OF RS. 20 CRORES AND ABOVE NBS_ALM 2 Details of any mismatches in Assets, liabilities and Regional office of the interest rate exposure (Within 20 days of the closure of Department in whose half year) jurisdiction NBFC is registered SUBMITTED BY ALL NON-DEPOSIT TAKING NBFCS NBS_ALM 3 Interest rate sensitivity Statement shall filed with the Bank NBFC YEARLY COMPLIANCES FORM NAME PURPOSE OF THE FORM DEPARTMENT SUBMITTED BY ALL NON-DEPOSIT TAKING NBFCS ALM Return Asset liability mismatches and interest rate exposure RBI SUBMITTED BY ALL RESIDUARY NON BANKING COMPANIES: Form NBS 1A Annual Return on Deposits (Filed annually after March 31 Regional Office of and latest by September 30) Department of Non -Banking Supervision, RBI where registered office of the company is situated SUBMITTED BY NBFCS HAVING ASSET of RS 100 TO RS 500CR NBS 8 Annual Return on Non-Deposit taking NBFC With Asset RBI Size from Rs.100 Cr. To 500 Cr SUBMITTED BY NBFCS HAVING ASSET SIZE BELOW RS 100CR NBS 9 Annual Return on NBFC ND SI With Asset Size Below RBI Rs.100 Cr

SUBMITTED BY ALL NON BANKING FINANCIAL COMPANIES ACCEPTING / HOLDING PUBLIC DEPOSITS, AND MNBCS EXCEPT RESIDUARY NON BANKING COMPANIES NBS 4 Repayment of Deposits only in respect of Department of Non -Banking rejected/cancelled companies Supervision, RBI CA certificate Certifying NBS 4 RBI form NBS - 4 NBFC UNDER COMPANIES ACT, 2013 FORM NAME PURPOSE OF THE FORM DEPARTMENT E- Form MGT-‐ Annual Return (Within 60 days of conclusion AGM) ROC 7 E- Form Filing of annual financials i.e. Balance Sheet & Profit & ROC AOC -4 Loss statement (Within 30 days of conclusion of AGM) E -Form DIR-‐ If there is any change in Directors (Within 30 days of the ROC 12 date of that change) LIST OF COMPLIANCE ON BASIS OF TYPE OF NBFC NON- DEPOSIT TAKING NBFCS FORM NAME PURPOSE OF THE FORM DEPARTMENT Monthly Return Monthly Return with asset size of Rs.100 CR. & above RBI NBS_ALM 1 Statement of Short term dynamic liquidity (Within 10 RBI days of the end of every Month) NBS- 7 Quarterly Statement of Capital Funds, Risk Weighted RBI Assets and risk assets Ratio etc. SA & CEO Certifying NBS 7 RBI certificate for NBS 7 NBS_ALM 3 Interest rate sensitivity statement shall filed with the Bank ALM Return Asset liability mismatches and interest rate exposure RBI

COMPLIANCE BY DEPOSIT TAKING NBFC’S WITH ASSET SIZE OF MORE THAN RS. 100 CRORES OR HAVING PUBLIC DEPOSITS OF RS. 20 CRORES OR MORE FORM NAME PURPOSE OF THE FORM DEPARTMENT NBS 6 Monthly Return on Exposure Towards Capital Market RBI NBS_ALM 2 Asset liability mismatches and interest rate exposure Regional office of the (Within 20 days of the closure of half year) Department in whose jurisdiction NBFC is registered COMPLIANCE BY DEPOSIT TAKING NBFC’S EXCEPT RESIDUARY NBFC’S: FORM NAME PURPOSE OF THE FORM DEPARTMENT NBS 1 Quarterly Return on Important Financial Parameters of RBI Deposit Taking NBFCs NBS 2 Quarterly Statement of Capital Funds, Risk RBI Assets/Exposures and risk assets Ratio. CA & CEO Certifying NBS 2 RBI certificate for NBS 2 NBS 3 Quarterly Return stating Statutory Liquid Assets RBI NBS 4 Repayment of Deposits Department of Non Banking (To be filed only in respect of rejected/cancelled Supervision, RBI companies) CA certificate Certifying NBS 4 RBI form NBS 4 SUBMITTED BY ALL RESIDUARY NBFC: FORM NAME PURPOSE OF THE FORM DEPARTMENT NBS 3A Quarterly Return on Statutory Liquid Assets RBI Quarterly Return of investments RBI Return I Form NBS 1A Annual Return on Deposits (Filed annually after closure Regional Office of of financial year and latest by September 30) Department of Non- Banking Supervision, RBI where registered office of the company is situated

Form Schedule General Information of the Company (filed annually as Regional Office of the "A" early as possible latest by the 30th September) Department of Supervision, Financial Companies Wing SUBMITTED BY NON-DEPOSIT TAKING NBFC’S HAVING ASSET SIZE BETWEEN RS. 50 CRORES TO RS. 100 CRORES FORM NAME PURPOSE OF THE FORM DEPARTMENT Quarterly Quarterly Return by Non-Deposit taking NBFC’s with RBI Return asset size of Rs.50 - 100 Cr. SUBMITTED BY ALL SECURITISATION AND RECONSTRUCTION COMPANY FORM NAME PURPOSE OF THE FORM DEPARTMENT SCRC Quarterly statement of assets acquired/ securitized/ RBI reconstructed SUBMITTED BY NON-DEPOSIT TAKING NBFCS HAVING ASSETS OF RS. 100 TO RS 500 CRORES FORM NAME PURPOSE OF THE FORM DEPARTMENT NBS 8 Annual Return on Non-Deposit taking NBFC’s With Asset RBI Size from Rs.100 Cr. To 500 Cr SUBMITTED BY NBFC-ND-SI HAVING ASSET SIZE BELOW RS 100CR FORM NAME PURPOSE OF THE FORM DEPARTMENT NBS 9 Annual Return on NBFC -ND -SI with Asset Size Below RBI Rs.100 Cr SUBMITTED BY ALL NBFCS WHETHER HOLDING PUBLIC DEPOSITS OR NOT FORM NAME PURPOSE OF THE FORM DEPARTMENT Special Return General information and Net Owned Funds RBI Branch Info Branch Details RBI DOCUMENTS FOR NBFC REGISTRATION

Certified copies of the Certificate of Incorporation of the Company. Certified copies of main object clause of the Memorandum of Association of the Company. Board resolution(s) stating the following: the company undertakes that it is not carrying on any NBFC activity or has not carried on and stopped any NBFC activities in the past activity and will not carry on or commence the same before getting registration from RBI the unincorporated bodies in the group where the director holds substantial interest or otherwise which has not accepted any public deposits in the past; and does not hold any public deposit as on the date of application will not accept any public deposits in the future the “Fair Practices Code” as per RBI Guidelines has been formulated by the Company the company: has not accepted public funds in the past and/or does not hold any public fund as on the date; and the Company will not accept any deposits in the future without the prior approval of Reserve Bank of India the company shall seek prior approval of RBI before creating any customer interface in the future Copy of Fixed Deposit receipt & bankers certificate indicating Net Operating Fund. The companies which are already in existence the following documents are to be submitted for the last 3 years OR from the period of incorporation of the Company till the closure date of the previous financial year: Audited balance sheet along with annexures Profit & Loss statement Directors Report Auditors report

Banker’s report regarding: Directors of the applicant company having substantial interest in any other companies Applicant company along with the directors of its group, subsidiary, associate, holding company and related parties. The Banker’s report should be about the dealings of these entities with these bankers as a depositing entity or a borrowing entity. Note: Bankers report is to be obtained from all the bankers of each of these entities. This report should specifically mention the details of deposits and loans balances as on the date of application and the conduct of the account. Copy of the certificate of highest educational and professional qualification in respect of all the directors Copy of experience certificate, if any, in the Financial Services Sector (including Banking Sector) in respect of all the directors ADDITIONAL DOCUMENTS IN ADDITION TO THE DOCUMENTS MENTIONED ABOVE, FOLLOWING LIST OF DOCUMENTS / INFORMATION REQUIRED TO BE SUBMITTED BY I. NBFC-MFI APPLICANT Board resolution stating that: the company will be a member of all the Credit Information Companies and will be a member of at least one Self-Regulatory Organization the company will observe the regulations relating to pricing of credit, Fair Practices in providing credit and non-coercive system of recovery as per RBI Guidelines the company has fixed internal exposure limits to avoid any undesirable concentration in specific geographical locations the company is not licensed under Section 25 of the Companies Act, 1956 / Section 8 of the Companies Act, 2013. Detailed Roadmap for achieving 85% qualifying assets. II. NBFC-FACTOR APPLICANT: Board Resolution stating the roadmap by which the company will have at least 50% of its total assets

in factoring business and not less than 50% of its gross income will be the income derived from factoring business (Specify the time frame) III. NBFC-IDF APPLICANT: NOC from RBI issued to NBFC-IFC for sponsoring the NBFC-IDF. Copy of Tripartite Agreement entered into between the concessionaire, the Project Authority and NBFC-IDF. Details regarding any changes in the management of the sponsor company during last financial year till date. Source of initial capital of the company with documentary evidence. Infrastructure Development Funds should raise its finances through the issue of Rupee or Dollar denominated Bonds with a minimum maturity period of 5-year. Request a Callback Name Email Contact No. Enquiry for No unwanted emails | No spam, corpseed use security methods to protect your personal data from unauthorized access. Submit

FAQ`s What are the benefits of taking services from Corpseed ? At Corpseed, we are committed to offer our services to the entrepreneurs and businesses as a very cost-effective proposition. We believe that a customer is always right and the focus of any business activity should be to serve the customer with utmost loyalty. All our services come with SLAs (Service Level Agreements) for on-time service delivery and money back guarantee to ensure high level of customer satisfaction. What if I'm not happy with the service? At Corpseed, our valued customers are always kept in the loop as far as service delivery timeline is concerned and we inform our customers every time a milestone is achieved during each stage of service request processing. But we also believe that we may come across a customer who is not satisfied with our efforts. For that we have a very responsive Customer Care Department which work 24x7 to attend to and solve customer complaints. We also have a money back guarantee for those, who want their service charges to be refunded. How can I be sure that my documents are safe? At Corpseed, We believe it is our responsibility to protect our customer information from unauthorized access. We have put systems and processes in place to make sure that the customer information is safe with us during its storage and transfer between in house and third party servers. We continuously test our systems and processes for security breach and vulnerabilities are identified and fixed at a regular basis.. What is Corpseed cashback policy? If a customer is not satisfied with the service we provided and if he contacts our customer care helpline and files a formal complaint within 15 days of service delivery date, Corpseed would refund the entire or partial amount of Professional Fee charged for that particular service. What is the process to register customer complaints? If a customer is having issues with our service delivery process, he has various alternatives available at his disposal to register his grievance with us. He can either email his complaint at complaints@corpseed.com or he can call our 24x7 Customer Care Helpline. Also, any customer is always welcome to visit our office to lodge a complaint with the senior management.

What is the process for online payment? A customer can buy our services directly from our online platform, for which he need to make online payment. Once he clicks on "Apply Now", a new window will open, a customer is required to submit the information in the respective fields and click "Make Payment". A unique ticket number will be auto generated, the customer need to quote this number as reference for any enquiry regarding his service request. Is the online payment secured All the monetary transactions performed on Corpseed online platform are secured with SSL System Protocol. We encrypt the customer information such as credit card and bank account details, before these are transmitted anywhere. We adhere to PCI DSS for data security standards for payment processing. Legal Guide Download free legal guide on how to successfully start and manage business in India & achieve 100% compliance. Enter Email Id... Enter Mobile Number... Download Latest News Get helpful tips and info from our newsletter!

Type Your Email Here... Submit Go to Knowledge Centre info@corpseed.com +91-8448 444 985 F-39, Sector 6, Noida, Uttar Pradesh. ABOUT COMPANY Knowledge Centre Become A Partner Contact Us About Us Join our team COMPANY POLICIES Privacy policy Terms and conditions Refund policy Law Updates SiteMap POPULAR SERVICES GST Registration Proprietorship Firm Trademark Registration FSSAI Basic Registration Private Limited Company Change Your CA