Download

1 / 64

640 likes | 794 Vues

Mr. Somphong Wanapha Secretary General Thailand Board of Investment January 2003. Outline of Presentation. Macroeconomic Overview FDI in 2002/2003 Thailand’s Competitive Advantages Targeted Opportunities in Thailand. The Macroeconomic Picture in Statistics (1 of 2).

E N D

Mr. Somphong Wanapha Secretary General Thailand Board of Investment January 2003

Outline of Presentation • Macroeconomic Overview • FDI in 2002/2003 • Thailand’s Competitive Advantages • Targeted Opportunities in Thailand

The Macroeconomic Picture in Statistics(1 of 2) 1998 1999 2000 2001e* 2002e** GDP Growth (%) -9.4 4.4 4.6 1.8 4.9 GDP (US$ Bil)111.9 122.4 122.1 114.4 125.6 Inflation (%) 8.1 0.3 1.6 1.6 0.6 GDP Per Capita 1,820 1,980 1,957 1,830 1,990 (US$) Fiscal Balance (US$ Bil)-2.6 -3.0 -2.6 -2.5 -2.8 Sources: * = Bank of Thailand ** = ThailandOutlook.com (January 10, 2003)

The Macroeconomic Picture in Statistics(2 of 2) 1998 1999 2000 2001e* 2002e** Foreign Reserves 29.5 34.8 32.7 33.0 38.7/*** (US$ Bil.) Export Growth (%) -6.6 7.4 19.5 -6.9 1.7 Value of Exports 54.5 56.8 67.9 63.2 64.3(US$ Bil.) Current Account 12.6 10.1 7.6 5.3 3.6 (% of GDP) MPI 96.5 108.6 112.1 113.5 130.1*** (Manufacturing Production Index) Sources: * = Bank of Thailand ** = ThailandOutlook.com (January 10, 2003) *** = As of January 3, 2003

Government Stimulus • Restructuring Farm Debts • Providing Million Baht Grants to all 70,000 villages • Thailand Asset Management Corporation • Supporting SMEs via State Banks

Board of Investment Approved Foreign Investment by Country 2000 2001 2002 Number Value of Number Value of Number Value of of Investment of Investment of Investment Projects (mil. US$) Projects (mil. US$) Projects (mil. US$) Total1,116 6,967 820 5,987 721 3,775 Foreign 761 5,295 575 4,713 483 2,316 By Country Japan 282 2,674 257 1,874 215 892 U.S.A. 73 944 40 902 37 258 Taiwan 120 439 50 153 41 63 Hong Kong 31 155 20 218 5 37 Singapore 84 495 51 202 40 305 E.U. 144 776 79 518 65 378 Note 1: Investment projects with foreign equity participation from more than one country are reported in the figures for each country Note 2: 2000 US$=40.16 baht; 2001 US$=44.48 baht; 2002 US$=43.00 baht

Investment from the US • Approved projects in 2002 • Honeywell — US$12 million to produce plated thermal spreaders • Cargill — US$5 million in agriculture (chicken) • Johnson Controls — US$8.5 million for automotive seats • An International Procurement Office from 3M • Regional Operating Headquarters from ExxonMobil

Regional Operating Headquarters (ROH) • In August, the Government Established Regulations Covering Regional Operating Headquarters • Companies must be incorporated under Thai law and have paid-up minimum capital of 10 million baht • They must service branches or affiliates in at least 3 countries • Income must come from managerial, administrative, technical, or other prescribed supporting services for branches/associated companies

ROH • Benefits • Corporate income tax at 10% for: • Qualified services • Royalties from ROH in Thailand • Interest income on loans made to ROH branches/associated enterprises • Tax exemption for dividends from ROH branches/associated enterprises • Expats working for ROH are taxed at 15% for 1st 2 years, instead of on sliding scale

FDI in 2003 • Targeting Same Level of Investment as 2002 • Quality is More Important Than Quantity • We are Looking for Projects to: • Enhance the competitiveness of Thai industry • Upgrade human capital (i.e. human resource development) • Help develop and transfer skills and technology • Nurture Thai talent

FDI in 2003 • Objectives Include: • Encouraging Cluster Development • Particularly in automotive and petrochemicals (Eastern Seaboard) • Targeting investment • By region and by industry • We have established 5 target industries and will develop industry-specific measure to support them • Non-target industries • No changes in policy, no backtracking

Competitive Advantages • ASEAN and AFTA • Progressively being implemented • Location and Social Stability • Peaceful Buddhist country • Free from social unrest • Well-developed infrastructure • Political System • Stable democracy • Reform-oriented government • Workforce • Trainable and adaptable

Competitive Advantages • Cost-effective Local Inputs • Least expensive office space in Asia • Vibrant supporting industries support subcontracting • Canon sources 70% of all parts locally • Toyota is looking to source 100% locally by 2006 • More and more manufacturers and assemblers acknowledge that Thai local inputs are key to global competitiveness

China • Should You Put All Your Eggs in the China Basket? • China has huge potential, but investment landscape is a bit uncertain

China • JETRO Report Found That: • In 14 categories, Thailand was ranked better than China in 11, including: • Legal framework • Transparency • Infrastructure • Development of parts industry • For Global Markets, Even China Invests in Thailand

Target Industries • We Have Identified 5 Groups of Target Industries • Agro-Industry • Automotive • Fashion • Electronics and ICT • High-Value Services

Target Industries • Specific Policies and Measures Will Be Developed for Each Target Industry, Based On • Competitiveness • Levels of technology • Market potential • Non-target Industries • No change in policy • No backtracking • No reduction in incentives

Leading Agricultural Exports Export Value ------------------------------------------------------------------------------------ • Rice 73,812* • Canned Seafood 65,957 • Shrimp 48,696* • Rubber 43,942* • Canned Tuna 21,886* • Chicken 21,796 • Canned Fruit 21,767 • Sugar 21,687 • Canned Pineapple 11,433* * #1 Exporter in the World Unit = Million Baht

Agricultural Priority Activities • Under revised BOI policy (effective August 1, 2000), 26 agricultural activities have been classified as priority activities, including 8 newly-promoted categories: • Manufacturing of alcohol or fuel through plants • Fertilizers produced through biotechnology • Manufacturing of products through herbs • Analysis of plant disease • Analysis and certification of agricultural products • Soil and water analysis for agriculture • Agricultural Trading Centers • Agricultural Processing Zones

Automotive Industry in 2001 • Assembly • Market 297,052 units +13.3% • Export 175,299 units +14.7% • Production 459,418units +11.6% • Total Component Industry – US$3.8 billion • OEM US$2.3 billion • OESpare US$0.5 billion • REM US$1.0 billion • 500 Component Manufacturers • Employing 100,000 Workers

Auto Parts & Components Manufactured in Thailand • Engines • Diesels, Motorcycles • Engine Components • Starters, Alternators, Pumps, Filters, Hoses, Gears, Flywheels • Body Parts • Chassis, Bumpers, Fenders, Hoods, Door Panels • Brake Systems • Master Cylinders, Drums, Discs, Pads, Linings, • Steering Systems • Steering Wheels, Gears, Columns, Pumps, Linkages • Suspensions • Shocks, Coils, Ball Joints • Transmissions • Gears, Casings, Rear Axles, Drive Shafts, Propellor Shafts • Electrical/Electronics • Alternators, Starters, Speedometers, Lamps, Motors, Flasher Relays • Interiors/Exteriors • Seats, Mats, Weather Strips, Console Boxes • Others • Windshields, Seat Belts, Radiators, Wheels, Compressors

Components Not Produced in Thailand • Passenger Car Engines • Fuel Injection Pumps • Transmissions • Differential Gears • Final Gears • Injection Nozzles • Electronic Systems • Electronic Control Units

Thai Automotive Trends • Gradual Recovery of Automotive Market • Expanding Exports • Continued Investment in Parts & Components • Continued Investment in Assembly • Thailand is Hub of Auto Industry in Region

Fashion • Develop Thailand as Fashion Center for Southeast Asia • Leather • Opportunities lie in technical cooperation and quality improvement, particularly in design and branding • Jewelry • Thai gold, silver, and costume jewelry in high demand , due to Thai artisanship • Opportunities to bring in high-tech equipment and to help with design • Garments • Provide training institute to produce international-standard fashion graduates • Provide consistent supply of high-quality raw materials

High Value Added Services • High-Value Services • Regional Operating Headquarters • Attractive package of tax incentives (comparable to any in the region) • Non-tax incentives from the BOI • Long-Stay Tourism • Retirement homes • “Snowbirds” • ICT-Related Services • E-Commerce Application Service Providers • E-Commerce Users

Electronics & Electrical Appliances in Thailand • Consumer Electronics • Computers & Peripherals • Telecom & Office Equipment • Electronic Components & Parts • Electrical Products & Parts • The Industry • 750 Companies • 300,000 –350,000Employees • US$17.2Billion Investment • Export US$21 billion annually

Electronics Exports • Consumer Electronics • 2000 Exports –US$3.3Billion (+17%) • 2001 Exports – US$2.9 Billion (-12%) • Computers and Peripherals • 2000 Exports – US$7.8 Billion (+3%) • 2001 Exports – US$6.8 Billion (-12%) • Telecoms and Office Equipment • 2000 Exports – US$1.2Billion (+10%) • 2001 Exports – US$1.0 Billion (-17%) • Electronic Components and Parts • 2000 Exports – US$9.3 Billion (+23%) • 2001 Exports – US$7.8 Billion (-15%) • Electrical Products and Parts • 2000 Exports –US$1.9Billion (+17%) • 2001 Exports – US$2.1 Billion (+11%)

Thailand Board of Investment BOI on the Internethttp://www.boi.go.th For the past two years, the BOI web site was ranked #5 Investment Promotion Agency website in the world byCorporate Location Email: head@boi.go.th • Up-to-date Info on BOI Policies, Procedures, Incentives and Services • Links to Business News About Thailand • What’s New at the BOI • Links to Important Business Sites • Cost of Doing Business in Thailand • Database of Promoted Companies • Comprehensive Information From Other Government Agencies • BOI Statistics • Trade Statistics • Demographic Data • Industrial Estates

The Road Ahead • Seven Key Strategies to Keep Thailand Competitive • Remove obstacles to investment • Proactive marketing of Thailand • Improve overseas networking • Improve competitiveness • Market community enterprises • Monitor global trends • Cut through “red tape”

Removing Obstacles • The BOI Wants to be Your Business Partner • We constantly meet with investors to find out what we can do to improve investment climate • We are committed to playing a coordinating role with other government agencies • We have set up an investment facilitation unit to work with investors to help solve problems

Proactive Marketing • Target Three Key Regions • Europe (EU) • Asia (Japan, China, Singapore, Hong Kong, Korea) • North America (U.S. and Canada) • Plans to Open New Offices in: • Shanghai • San Francisco • Osaka • Promote Target Industries

Improve Networking • Develop Linkages, Networks, Partnerships With: • Banks • Investment Promotion Agencies • Provincial Governments • Develop Sister City/Sister Province Relationships • Work With Chambers of Commerce • Both in Thailand and overseas

Improving Thai Competitiveness • Send a “Wake-Up Call” to Thai Industry, Particularly SMEs • Inform them of changes in global marketplace • Make them aware of need to adopt “industry best” practices and technology • Help them coordinate skills transfer through training

Marketing Community Enterprises • BOI Will Play a Coordinating Role With Thai SMEs • Working with other Ministries to ensure SMEs receive maximum government support • Encourage foreign SMEs to partner with Thai SMEs to provide • Technical assistance • Foreign market access • Assistance in adapting Thai products for foreign markets

Monitoring International Investment Trends • Separate Unit at BOI to Monitor Global Investment Environment • Provide both the Thai government and the Thai investment community early warnings about legislative and procedural changes in the international investment arena

Improve the BOI • The BOI is Always Looking to Improve the Way We Do Business • Already ISO 9002 certified, ensuring all investors receive fair and transparent treatment • We will continue to improve range of services • We will look to streamline procedure to cut through “red tape”

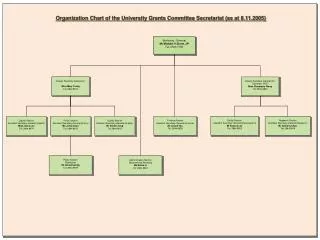

The Board of Investment Organization Chart Thailand Board of Investment Board of Investment Office of the Prime Minister Policy Administrative Office of the Board of Investment

MIDA EDB EDB BOI MIDA EDB EDB MIDA MIDA EDB EDB MIDA

EDB MIDA MIDA BOI EDB MIDA EDB EDB BOI MIDA EDB MIDA

BOI EDB MIDA MIDA สำนักงานส่งเสริมการลงทุนในญี่ปุ่น EDB MIDA MIDA EDB EDB MIDA

BOI Policy Priority Activities (1 of 2) • Agriculture – Backbone of the Country • Technological and human resource development • Infrastructure, public utilities and basic services • Environmental protection/conservation • Targeted Industries - such as: • Steel casting using induction furnace • Forged steel parts • Electronic design • Software and software park

BOI Policy Priority Activities (2 of 2) • These five categories of priority activities are eligible for special incentives: • Import duty exemption on machinery • Eight-year corporate income tax holiday, regardless of zone

Services of the BOI The BOI offers : Investment Matchmaker Program Support around the world – 4 overseas offices (New York, Paris, Frankfurt, Tokyo) One-Stop Shop for Visas and Work Permits – Work Permits within 3 hours Services of BUILD Unit to promote industrial subcontracting – Vendors Meet Customers Program ASEAN Supporting Industry Database (ASID) Comprehensive, world-class website Help with work and residency permits Interaction with other government agencies on behalf of investors

Big Mac Index Source: The Economist, April 2002

New Activities Eligible for Promotion • E-Commerce Application Service Provider • E-Commerce User • Regional Headquarters • International Distribution Centers • International Procurement Offices • Retirement Homes • Dedicated Health Centers • Waste Recycling

Supporting Industriesin ASEAN ASEAN Supporting Industry Database Expands the scope of ASEAN’s supporting industries by serving as the region’s industrial yellow pages The ASID home page (www.asidnet.org) contains information about more than 11,000 supporting industry companies throughout ASEAN Provides communication links to facilitate electronic commerce between ASEAN suppliers and foreign purchasers.