Download

1 / 12

120 likes | 595 Vues

Hurricane Mitigation Plans. Michael A. Walters FCAS, MAAA CAS Catastrophe Seminar October 16, 2000. Topics of Discussion. Creating a mitigation/class plan in Florida Could have used a single model Did use multiple sources Deciding cost/effective class variables

E N D

Hurricane Mitigation Plans Michael A. Walters FCAS, MAAA CAS Catastrophe Seminar October 16, 2000

Topics of Discussion • Creating a mitigation/class plan in Florida • Could have used a single model • Did use multiple sources • Deciding cost/effective class variables • Standards and considerations • Selecting a base class • Adjusting to new base class

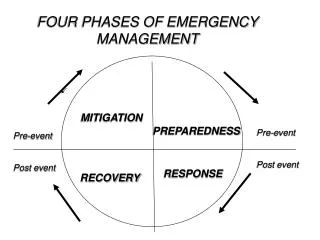

Creating a mitigation/class plan • Florida hurricane is already separate • In Windpool (FWUA) wind coverage • Split out Other Wind • Goal: mitigation plan plus rate level • Identify true costs • Incentive for insureds to mitigate home • Transition plan: stagger premium increases • Payback in a few years of premium savings

Could have used a single model • For base class, use single house in each zip code at base coverage • For each class, run model for single house by zip code • Track relationship to base by zip • Use mapping software to group similar zip code relationships • Publish relativities by zone or statewide

Florida: did use multiple sources • Decide what variables to include • Survey sources for relativities • Use several zip codes around state • Delphi technique for outliers • Apply actuarial judgment • Peer review by engineering experts

Decide rating variables • Roof - shape, covering, waterproof sheathing, pitch, overhang • Connections - straps, nailing (size,spacing) • Windows and Doors - shuttering, garage door size & bracing, glazing • House Features - stories, porches, construction • Environment - terrain, debris exposure

Standards • Homogeneous • No clear subsets of large different loss potential • Reasonably related to loss hazard • Well Defined • Exhaustive and mutually exclusive • No ambiguity in placement • No manipulation by insureds • Practical • Reasonable cost to administer • Able to be tested by actual loss data

Considerations • Prioritize items that insureds can change • Use results from mitigation programs • Combine categories to control number of classes • Measure interaction among variables • May need on-site survey by independent professionals

Selecting/Adjusting Base Class • Base Class • Generally the prevailing condition • Discounts for other classes • Sample: gable roof, no shutters, no roof clips • Adjust Loss Costs to New Base • Estimate distributions of classes • Use class relativities to calculate off-balance

Base Class Assumptions (italics) • Roof • Shape - gable unbraced, gable braced, hip, flat • Cover - Shingle, tile, slate, metal, poured concrete • Waterproof sheathing underlayment - No, yes • Pitch - <10d, 10-30, >30 degrees • Overhang - <16,16-36, >36 inches • Connections • Hurricane Clips - No, yes: at roof, at foundation • Sheathing Attachment - 6d nails, 8d nails

Base Class Assumptions (italics) • Windows and Doors • Shuttering - None, ordinary, hurricane resistant (debris impact) • Glass patio doors - Yes, no • Garage doors - single-wide, double-wide; braced, unbraced • Laminated glass - No, yes

Base Class Assumptions (italics) • House Features • Number of stories - one, >one • Porches/canopies/carports - Yes, no • Construction - frame, masonry: reinforced? • Year Built/Code Enforcement - before 1995/not enforced, other • Environment • Suburban light tree cover, dense • Other - waterfront, urban, rural