Download

1 / 0

0 likes | 258 Vues

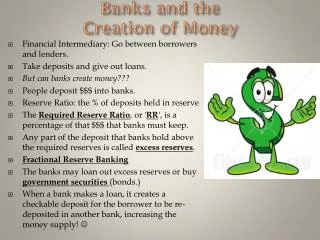

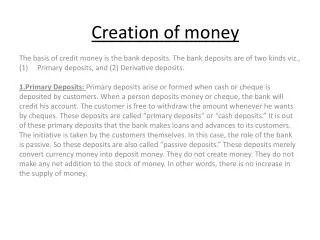

Creation of Money. Chapter 32. Currency. Checking deposits. Outside banks. In commercial. $710 billion. Banks $330 billion. M1. $1361 billion. Savings. Other. deposits. checkable. $4378 billion. deposits. $321 billions. Money market. M1 = $1361 billion. mutual funds.

E N D