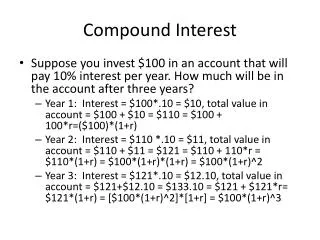

Compound Interest

Compound Interest. A word on terminology. You will find it useful to remember that compounding Annually means once a year Semiannually means twice a year Quarterly means 4 times a year Monthly means 12 times a year Weekly means 52 times a year Daily means 360 times a year. Not 365!.

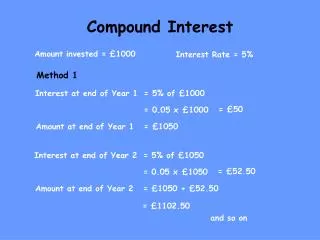

Compound Interest

E N D

Presentation Transcript

A word on terminology • You will find it useful to remember that compounding • Annually means once a year • Semiannually means twice a year • Quarterly means 4 times a year • Monthly means 12 times a year • Weekly means 52 times a year • Daily means 360 times a year Not 365!

Many questions about financial transactions can be dealt with using the Compound Interest Formula. • But we’ll consider a different way of looking at compound interest. • We will extensively use the TVM solver of your TI calculator.

To access this feature of your calculator, proceed as follows: • If you are using a TI-83+ or TI 84, • Select APPS, Finance, TVM Solver • If you are using TI-83, • Select 2nd, x-1, TVM Solver

TimeValueofMoneySolver Open the TVMsolver and you’ll see something like: • N= • I%= • PV= • PMT= • FV= • P/Y= • C/Y= • PMT:End Begin. Note the TVMvariables:

Defining the TVM variables • N: Total number of compounding periods • I: Annual interest rate • PV: Present value of money • PMT: Payment amount per compounding period • FV: Future value of money • P/Y: Number of payments per year • C/Y: Number of compounding periods per year

Remarks about using the TVM Solver • P/Y will always be the same as C/Y. • Interest is entered in percent, not in decimal form. • Cash inflows (money received) must be entered as positive numbers • Cash outflows (money paid) must be entered as negative numbers. • At the bottom of the TVM Solver menu, make sure that End, not Begin, is always highlighted.

We now consider a few of examples. • In each one, please try to see • how we interpret information to put in the TVM solver • how we interpret information obtained from the TVM Solver The emphasis is on getting used to the TVM Solver variables

Example #1: An old problem revisited • A loan company charges 20% interest per year compounded quarterly for a 1-year $1000 loan. • What is the total interest for this loan?

Example #2 Jane is 21 and wants to have $10,000 on her 25th birthday. How much money does she have to invest at 6% interest compounded monthly to achieve her goal?

Example #3 Jim is the beneficiary of a trust fund established for him at his birth. If the original amount placed in the trust was $10,000, how much will he receive 21 years later, assuming the money has earned interest at the rate of 8% per year compounded quarterly?

Example #4 Joe puts $2,000 into a savings account that earns interest at a rate of 4.5% compounded daily. How long will it take him to triple his investment?

Example #5 Jim is the beneficiary of a trust fund established for him at his birth. If the original amount placed in the trust was $10,000, how much will he receive 21 years later, assuming the money has earned interest at the rate of 8% per year compounded quarterly? Monthly? Daily? 1000 times a year? 10000 times a year? Continuously?