Download

1 / 6

60 likes | 290 Vues

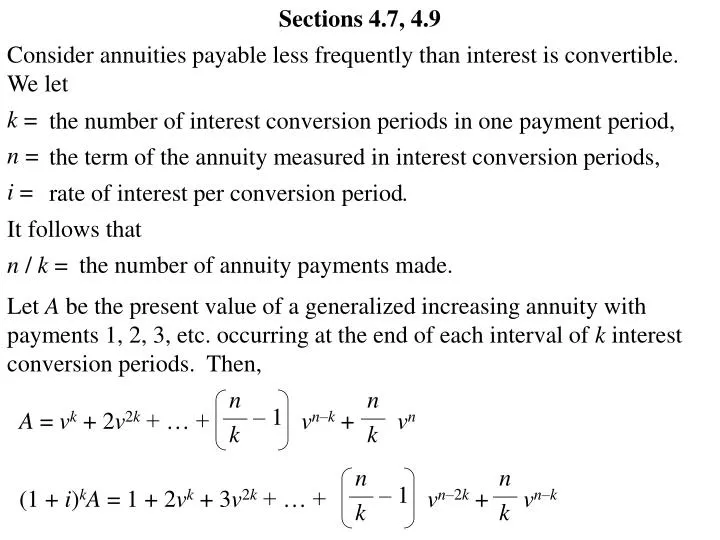

Sections 4.7, 4.9. Consider annuities payable less frequently than interest is convertible. We let k = n = i =. the number of interest conversion periods in one payment period,. the term of the annuity measured in interest conversion periods,. rate of interest per conversion period .

E N D

Sections 4.7, 4.9 Consider annuities payable less frequently than interest is convertible. We let k = n = i = the number of interest conversion periods in one payment period, the term of the annuity measured in interest conversion periods, rate of interest perconversion period. It follows that n / k = the number of annuity payments made. Let A be the present value of a generalized increasing annuity with payments 1, 2, 3, etc. occurring at the end of each interval of k interest conversion periods. Then, n — – 1 k n — k A = vk + 2v2k + … + vn–k + vn n — – 1 k n — k (1 + i)kA = 1 + 2vk + 3v2k + … + vn–2k + vn–k

n — – 1 k n — k A = vk + 2v2k + … + vn–k + vn n — – 1 k n — k (1 + i)kA = 1 + 2vk + 3v2k + … + vn–2k + vn–k Subtracting the first equation from the second, we have n — k A[(1 + i)k– 1] = 1 + vk + v2k + … + vn–k–vn a – n| a – k| a – n| n — k This is the present value of an increasing annuity with payments 1, 2, 3, etc. occurring at the end of each interval of k interest conversion periods. – —————— i vn a – k| A = s – k| Similar derivations can be done when payments increase in some other arithmetic progression.

Consider an increasing annuity payable more frequently than interest is convertible with constant payments during each interest conversion period. Let the annuity be payable mthly with each payment in the first period equal to 1/m, each payment in the second period equal to 2/m, etc. Letting i be the rate of interest per period, we use i(m) to write a formula for present value of the n-period annuity-immediate denoted by . (m) (Ia)– n| Making the mthly payments of k/m in period k is the same as making one payment equal to the accumulated value of the mthly payments at the end of the period, that is, one payment of k — m k — m (1 + i(m)/m)m – 1 ——————— = i(m)/m i k — i(m) = s – m| i(m)/m 1 — m 1 — m 1 — m 1 — m k–1 —– m k — m k — m k — m k — m n–1 —– m n — m n — m m — m n — m … … … … … 0 1 k– 1 k n – 1 n

Consequently, the increasing annuity payable mthly is the same as an increasing annuity with P = Q = , which implies i — i(m) .. a – n| i — i(m) – nvn ————— i(m) (m) (Ia)– n| (Ia)– n| = = i — i(m) i k — i(m) i n — i(m) 1 — m 1 — m 1 — m 1 — m k–1 —– m k — m k — m k — m k — m n–1 —– m n — m n — m m — m n — m … … … … … 0 1 k– 1 k n – 1 n

Find the present value of a perpetuity which pays 1 at the end of the third year, 2 at the end of the sixth year, 3 at the end of the ninth year, etc. Let i be the effective rate of interest, and treat 3 years as one period. Then i* = is the rate of interest for three years. (1 + i)3– 1 With P = Q = 1, the present value of the perpetuity is PQ — + — = i*i*2 1 1 ————— + ————— = (1 + i)3– 1 [(1 + i)3– 1]2 v3 ——— (1 –v3)2 (1 + i)3 ————— = [(1 + i)3– 1]2 Look at Example 4.16 in the textbook (page 119) for an alternative way to obtain this present value.

Find the accumulated value at the end of eight years of an annuity in which payments are made at the beginning of each quarter for four years. The first payment is $3000, and each of the other payments is 95% of the previous payment. Interest is credited at 6% convertible semiannually. 3000 (1.03)16 + (0.95)(1.03)15.5 + (0.95)2(1.03)15 +… + (0.95)15(1.03)8.5 = 3000 (1.03)16 1 + (0.95/1.03) + (0.95/1.03)2 +…+ (0.95/1.03)15 1 – (0.95/1.03)16 ——————— = 1 – (0.95/1.03) = 3000 (1.03)16 $49,134.18 Look at the first three rows together with the first three columns of Table 4.1 (page 121) in the textbook.