Turkish New Lira

Turkish New Lira. David Bull Amy Mettling Seth Ohringer Scott Beville. History of Turkish Lira. In 1996, the Turkish money supply of Lira grew 130% leading to hyperinflation.

Turkish New Lira

E N D

Presentation Transcript

Turkish New Lira David Bull Amy Mettling Seth Ohringer Scott Beville

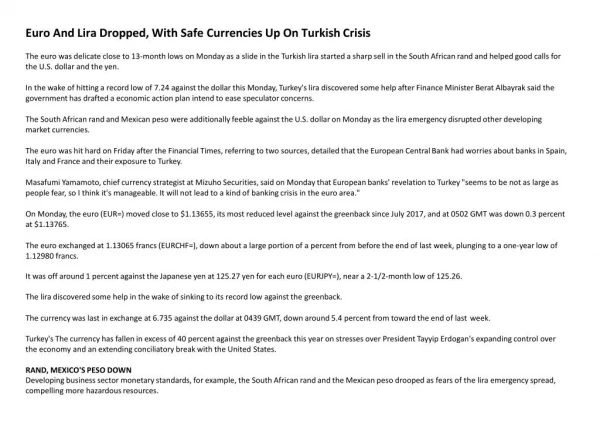

History of Turkish Lira • In 1996, the Turkish money supply of Lira grew 130% leading to hyperinflation. • In the 1960s, the Lira traded for about 9 per USD but in early 2003, the currency traded for 1,650,000 per US Dollar. • On Jan. 1, 2005, the New Turkish Lira was issued and each New Turkish Lira was worth 1,000,000 Turkish Lira. • This helped stabilize prices and inflation in Turkey.

Technical Analysis One Week Forecast reveals a strengthening Lira

Methods and Analyses • Moving Average Crossover Strategy: Moving spot rate crossed the 180-day average line and has continued to rise since mid-April; signaling strength • Market momentum: Currency shows overall strengthening over past 30 days, especially over the past two weeks • Bollinger Band Analysis: Moving spot is well under the upper-level Bollinger Band and shows no sign of bursting out of it

Graphical Analysis This inverted graph shows a combination of things; the green line being the 180-day average, within the blue area is included within the Bollinger Band. Time period is 31 Oct, 2005 to 1 May, 2006 http://fx.sauder.ubc.ca

Short-term Graphical Analysis This inverted graph shows the past 30 days as well as the 60-day moving average (green line). Time frame is 1 April, 2006 to 1 May, 2006 http://fx.sauder.ubc.ca

Implications & Advice • For a global firm headquartered in the US and with manufacturing operations in Turkey; the New Lira is strengthening against the dollar which means the company will suffer decreasing revenues due to increased relative local costs • In order to combat this, the company has a couple options if they choose to cover their open position…

Advice • One-week forward contract • this would cover their position in anticipation of the continued strengthening of the New Lira • Arrange a call option contract • for a price, this will allow the company to set a ceiling level for the New Lira at which the option will kick in and will save the company from an exchange loss • Given the circumstances, my recommendation would be for the company to sign a forward contract IF they choose to cover their open position at all

Asset Choice Model Turkish interest rates are relatively higher than US interest rates

The Central Bank of Turkey kept the rates unchanged at 13.5% to borrow and 16.5% to lend. Although in 2005 the Turkish Central Bank cut interest rates nine times. The central bank has been fighting it’s 30 year inflation by lowering interest rates and tightening the monetary policy

United States (4.75%) and the Euro zone (2.25%) • I do not recommend a Foreign Direct Investment into Turkey. • The country is still changing and is very risky for an investor who does not know what new policies will be in place in the next three months. • The Lira currency is at unstable levels and a US business investing in Turkey will have to hedge their short term exposure with forward contracts and options.

I predict the Turkish Lira, within the next three months, to continue to follow its current erratic movements against the US dollar. The New Lira has been on a strengthening trend within the last 20 days, but the trend shows an equal decrease after the strengthen. • Oven though the interest rates are higher in Turkey than the US, they are constantly being adjusted to normal levels to catch up to the lowered inflation rates. I would not recommend trying to take advantage of this interest rate differential.

Balance of Payment Model The Current Account deficit shows that the currency will weaken in the next three months

The list shows the Turkish Current Account deficit, (in millions of US dollars)10-2005 -881.0011-2005 -2615.0012-2005 -3751.0001-2006 -2431.0002-2006 -3487.00 As stated on the first page of the Central Bank of Turkey website, “The primary objective of the Bank shall be to achieve and maintain price stability.” Since the Turkish Central Bank plans to eliminate the public debt as one of the tools to fight inflation; the country will need a lot of foreign capital to finance their deficit. Since it is a long term fight against public debt and inflation I do not predict the Lira to strengthen in the next three months. The Lira will stay at current levels against the US dollar and will not strengthen until inflation and the debt is at desired levels.

US company implications • For a US company manufacturing in Turkey with a weakening Lira • US will benefit with lowered costs in US term • US company selling to Turkey with a weakening Lira • US will be at risk because there will be decreased demand from more expensive US products relative to domestic products

Relative PPP With a small inflation differential, the New Turkish Lira will not depreciation too much relative to the US Dollar.

Relative PPP • After the introduction of the New Turkish Lira, the inflation rate has begun to stabilize. • At the same time, the United States’ annual inflation rate has been experiencing an uphill trend. • Both currencies are expected to hover around 4% annual inflation in the next few years.

PPP Results • Variables: • Current Spot as of 4/27/06: 1.3214/US$1 • Expected US future annual inflation rate: 3.7% • Expected Turkish future annual inflation rate: 4% • Inflation differential = (4% - 3.7%) 0.3% • The New Turkish Lira should depreciate by 0.3% • Relative PPP Spot = Current Spot x (1 + infhome)^n/(1 + infforeign)^n • = 1.3214 x (1.04)^5/(1.037)^5 • = 1.3214 x 1.2166/1.1992 • = 1.3214 x 1.0145 • = 1.3406

Advice • For a Turkish Manufacturer: • The next five years look good in terms of exporting goods outside of Turkey • For an American company exporting to Turkey: • Set up a factory in Turkey because soon enough, it will be expensive to export to Turkey.

Problems • Finding the annual inflation rate for 2005 was not hard to find. • Necessary to know previous years’ inflation rate because of Turkey’s hyperinflation • Finding the inflation rates for the past couple of years was difficult for both Turkey and the US.

International Fisher Effect5 Year Forecast The IFE forecasts that the New Turkish Lira will weaken against the USD in the next five years.

International Fisher Effect • Current spot rate: 1.3287 (European terms: 1 USD = 1.3287 TRY) April 28, 2006 • Turkey 5 Year Bond Yield on 4/10/06 (1736 day): 15.09% • US 5 Year Bond Yield: 4.91% • New Turkish Lira 5 Year Forecast Rate = Current Spot rate * (1+inthome)^5 / (1+intforeign)^5 = 1.3287 * (1.1509^5 / 1.0492^5) = 2.1102

Data Collection • US rate was very easy to find due to the US’s stable economy • Turkish government issued 5 year bond was much more difficult to find • Auction prices • Interest rates ranged from 12% to over 15% over the past 4 months

Recommendations • US firm manufacturing in Turkey: • global diversification should still be used to cover any unknown economic exposure • US firm exporting to Turkey: • cover its accounts receivable or transaction exposure by a long forward contract