Balanced Scorecard

Balanced Scorecard. Dr. Nancy Mangold California State University, East Bay. Why Does Business Need a Balanced Scorecard?. If you can’t measure it, You can’t manage it. Why Balanced Scorecard?.

Balanced Scorecard

E N D

Presentation Transcript

Balanced Scorecard Dr. Nancy Mangold California State University, East Bay

Why Does Business Need a Balanced Scorecard? If you can’t measure it, You can’t manage it.

Why Balanced Scorecard? • An organization’s measurement system strongly affects the behavior of people both inside and outside the organization. • If companies are to survive and prosper in information age competition, they must use measurement and management systems derived from their strategies and capabilities.

Why Balanced Scorecard? • Unfortunately, many organizations espouse strategies about customer relationships, core competencies, and organizational capabilities while motivating and measuring performance only with financial measures.

Historical Measurement System • Historically, the measurement system for business has been Financial • Accounting has been called the “language of business” • Managers are pressured to deliver consistent and excellent short-term financial performance.

Financial Measurement • Trade-offs are made that limit the search for investments in growth opportunities. • Under pressure for short-term financial performance, companies reduce spending on • new product development • process improvements • human resource development • information technology, data bases, and system • customer and market development.

Financial Measurement • In the short-run, a company could maximize short-term financial results by exploiting customers through high prices or lower service. • In the short-run, these actions enhance reported profitability. • But the lack of customer loyalty and satisfaction will leave the company highly vulnerable to competitive inroads.

Financial Measurement • Financial measures are inadequate for guiding and evaluating organizations through competitive environments. • They are lagging indicators that fail to capture much of the value that has been created or destroyed by managers’ actions in the most recent accounting period.

Balanced Scorecard • BSC provides executives with a comprehensive framework that translates a company’s vision and strategy into a coherent set of performance measures

Translating a Mission into Desired Outcomes Vision (What we want to be) Mission (Why we exist) Strategy (Our game plan) Balanced Scorecard (Implementation and focus) Strategic Initiatives (What we need to do) Personal Objectives (What I need to do) Strategic Outcomes Satisfied Shareholders Delighted Customers Effective Processes Motivated and Prepared Workforce

Mission Statements • Communicate fundamental values and beliefs to all employees • Addresses core beliefs and identifies target markets and core products • Should be Inspirational • Supplies energy and motivation to the organization

Mission Statements • Rockwater (an undersea construction company) CEO led a two-month effort among senior executives and project managers to develop a detail mission statement. • A project manager from a drilling platform asked • What am I supposed to do? • How should I behave each day to deliver on our mission statement? • There is a large void between the mission statement and employees’ day-to-day actions.

Mission Statements • Mission statements are insufficient to guide employee’s day to day actions. • BSC translates mission and strategy into objectives and measures.

Balanced Scorecard Key Performance Indicators Internal Business Organizational Financial Customer Process Learning Perspective Perspective Perspective Perspective Critical Success Factors Internal Business Organizational Financial Customer Process Learning Perspective Perspective Perspective Perspective Strategic Goals Strategy Vision & Mission • Where is the organization going? • How do we get there • What are the strategic goals for which we are striving? • What do we need to “do well” to achieve these strategic goals • How do we measure how well we are doing?

Balance Scorecard • The scorecard provides a framework, a language, to communicate mission and strategy. • It uses measurement to inform employees about the drivers of current and future success.

Balanced Scorecard • By articulating • the outcomes the organization desires and • the drivers of those outcomes, • Senior executives hope to channel the energies, the abilities, and the specific knowledge of people throughout the organization toward achieving the long-term goal.

What is a Balanced Scorecard? A Strategic Management System that includes… • a set of Cause & Effect relationship assumptions linking key indicators and strategy • a set of targets for each one of the key indicators linked to a compensation system • a strategic feedback loop

Strategic Feedback Process Organizational Strategy Update the Strategy A strategic feedback process supports executives decision-making and allows executives to revise strategy as needed Strategic Learning Loop Measure the strategy Problem Solving Balanced Scorecard Financial Strategic Objective Strategic Measure --Financially Strong --Return on Capital Employed CUST --Delight the Consumer--Mystery Shopper Rating --Win-Win Relationship –Dealer/Pioneer Gross Profit split Internal --Safe & Reliable --Manufacturing Reliability Index --Competitive Supplier --Days Away from Work Rate --Good Neighbor --Laid Down Cost vs. Best --Quality Competitive Reliable Supply --Environmental Index --Quality Index L&G --Motivated & Prepared –Strategic Competency Availability Test strategy And identify issues Determine Tactical priorities Operations Planning & Monitoring Business Plans Strategic Initiatives Budget Individual Perf. Mgmt

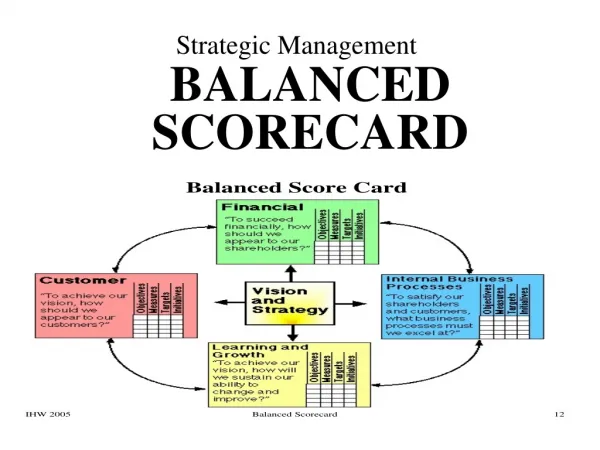

Four Scorecard Perspectives Financial Perspective To succeed financially, how should we appear to our internal and external shareholders? Customer Perspective To achieve our financial goals, how should we appear to our customers? Process Perspective To satisfy our shareholders and customers, at which internal business processes must we excel? Learning and Growth Perspective To achieve our vision, how will we improve the skills of our human resources, increase the effectiveness of our business processes and sustain our ability to change?

Translating Vision and Strategy: Four Perspectives Financial “To succeed financially, how should we appear to our shareholders?” Objectives, Measures, Targets, Initiatives Internal Business Process “To satisfy our shareholders And customers, what Business processes must We excel at?” Objectives, Measures, Targets, Initiatives Customer “To achieve our vision, how should we appear to Our customers? Objectives, Measures, Targets, Initiatives Vision And Strategy Learning and Growth “To achieve our vision, how will we sustain our ability to change and improve?” Objectives, Measures, Targets, Initiatives

Defining Key Performance IndicatorsCritical Success Factor KPI (Measures)

Financial Perspective • Financial performance measures indicate whether a company’s strategy, implementation, and execution are contributing to bottom-line improvement.

Financial Perspective • Relate to profitability-measures • Operating income • Return on capital employed • Economic value-added • Rapid sales growth • Generation of cash flow

Customer Perspective • Identify the customer and market segments in which the business unit will compete and • The measures of the business unit’s performance in these targeted segments. • Includes several core or generic measures of the successful outcomes from a well-formulated and implemented strategy.

Customer Perspective-Core Outcome Measures • Customer satisfaction • Customer retention • New customer acquisition • Customer profitability • Market and account share in targeted market

Market Share Customer Profitability Customer Outcomes Account Share Customer Retention Customer Acquisition Customer Satisfaction

Customer Perspective • Measures of value propositions that the company will deliver to customers in targeted market segments.

Customer Perspective • The segment specific drivers of core customer outcomes represent factors critical for customers to switch to or remain loyal to their suppliers • Short lead-time • On-time delivery • A constant stream of innovative products and services

Customer Perspective • A supplier able to anticipate their emerging needs and capable of developing new products and approaches to satisfy those needs.

Customer Perspective • Enables business unit managers to articulate the customer and market-based strategy that will deliver superior future financial returns.

Internal Business Process Perspective • Identify the critical internal processes in which the organization must excel.

The Internal Value Chain Postsales Service Cycle Operation Cycle Innovation Cycle Customer Need Identified Customer Need Satisfied Identify the Market Create The Product/ Service Offering Build The Products/ Services Deliver The Products/ Services Service The Customer

Internal Business Process Perspective • These processes enable the business unit to • Deliver the value propositions that will attract and retain customers in targeted market segments, • Satisfy shareholder expectations of excellent financial returns.

Internal Business Process Perspective • Focus on the internal processes that will have the greatest impact on customer satisfaction and achieving an organization’s financial objectives.

Internal Business Process Perspective • Two fundamental differences between the traditional and the BSC approaches to performance measurement. • Traditional approaches attempt to monitor and improve existing business processes. • Focus on improvement of existing processes.

Internal Business Process Perspective • BSC approach usually identify entirely new processes at which an organization must excel to meet customer and financial objectives. • It must develop a process to anticipate customer needs or one to deliver new services that target customers value. (processes not currently performing)

Internal Business Process Perspective • BSC incorporates innovation processes into the IBP perspective. • Traditional performance measurement systems focus on the processes of delivering today’s products and services to today’s customers. • They control and improve existing operations

Internal Business Process Perspective • Short-wave of value creation from. • Receipt of an order from an existing customer for an existing product (or service). • Ends with the delivery of the product to the customer. • Value created from producing, delivering, and servicing this product and the customer at a cost below the price it receives.

Internal Business Process Perspective • The drivers of long-term financial success may require an organization to create entirely new products and services that will meet the emerging needs of current and future customers.

Internal Business Process Perspective • The innovation process -long-wave of value creation • A more powerful driver of future financial performance than the short-term operating cycle.

Internal Business Process Perspective • The ability to develop a multiyear product-development process. • The ability to reach entirely new categories of customers. • May be more critical for future economic performance than managing existing operations efficiently, consistently and responsively.

Learning and Growth Perspective • Identifies the infrastructure that the organization must build to create long-term growth and improvement. • Customer and IBP perspectives identify the factors most critical for current and future success.

Learning and Growth Perspective • Businesses are unlikely to be able to meet their long-term targets for customers and internal processes using today’s technologies and capabilities. • Intense global competition requires that companies continually improve their capabilities for delivering value to customers and shareholders.

Learning and Growth Perspective • Organizational learning and growth come from three principal sources: • People • Systems • Organizational procedures.

Learning and Growth Perspective • BSC approaches will reveal large gaps between the existing capabilities of people, systems and procedures and what will be required to achieve breakthrough performance.

Learning and Growth Perspective • To close these gaps, businesses will have to invest in reskilling employees, enhancing information technology and system, and aligning organizational procedures and routines. • These objectives are articulated in the learning and growth perspective of the Balanced Scorecard.

Learning and Growth Perspective • Employee-based measures along with specific drivers of these generic measures • Employee satisfaction • Employee retention • Employee training • Employee skills-indexes of the particular skills required for the new competitive environment.

Learning and Growth Perspective • Information system capabilities. • Measured by real-time availability of accurate, critical customer and internal process information to employees on the front lines of decision making and actions.

Learning and Growth Perspective • Organizational procedures can examine alignment of employee incentives with overall organizational success factors • Measured rates of improvement in critical customer-based and internal processes.