Understanding Business Combinations: Bargain Purchase Gain vs. Goodwill

In business combinations, accounting outcomes can result in either a Bargain Purchase Gain or Goodwill. A Bargain Purchase Gain occurs when the fair value of acquired assets exceeds the fair value of liabilities and equity. Conversely, Goodwill arises when the fair value of liabilities and equity surpasses that of the assets. Understanding these concepts is crucial for accurate financial reporting and decision-making. This knowledge helps organizations better navigate the complexities of their financial valuations during mergers and acquisitions.

Understanding Business Combinations: Bargain Purchase Gain vs. Goodwill

E N D

Presentation Transcript

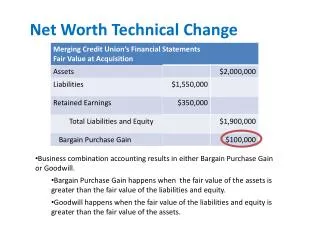

Business combination accounting results in either Bargain Purchase Gain or Goodwill. • Bargain Purchase Gain happens when the fair value of the assets is greater than the fair value of the liabilities and equity. • Goodwill happens when the fair value of the liabilities and equity is greater than the fair value of the assets. Net Worth Technical Change