Download

1 / 17

180 likes | 496 Vues

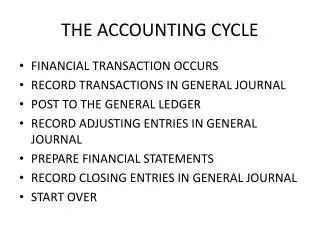

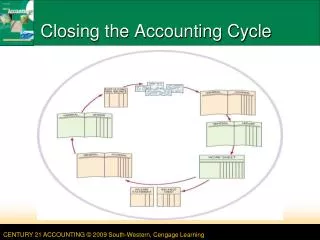

Closing the Accounting Cycle. Closing the Accounting Cycle. Please note that all slides are available on the class website. THE ACCOUNTING CYCLE. page 217. 1. Analyzes transactions. 1. 2. Journalize. 2. 3. Post. 8. 4. Prepare work sheet. 5. Prepare financial statements. 3.

E N D

Closing the Accounting Cycle Please note that all slides are available on the class website.

THE ACCOUNTING CYCLE page 217 1. Analyzes transactions 1 2. Journalize 2 3. Post 8 4. Prepare work sheet 5. Prepare financial statements 3 6. Journalize adjusting and closing entries 7 4 7. Post adjusting and closing entries 8. Prepare post-closing trial balance 6 5 LESSON 8-3

ADJUSTING ENTRY PROCEDURES page 202 1. Write the heading. 2. Write the date. 3. Write the title of the account debited. Record the debit amount. 4. Write the title of the account credited. Record the credit amount. LESSON 8-1

TERMS all on page 206 of your text book page 212 • permanent accounts • temporary accounts • closing entries LESSON 8-2

TERMS all on page 206 of your text book page 212 • Permanent Accounts – Accounts used to accumulate information form one fiscal period to the next. Examples of permanent accounts include asset and liability accounts (balance sheet accounts), as well as the owner’s capital account. • Temporary Accounts – Accounts used to accumulate information until it is transferred to the owner’s capital account. Examples of temporary accounts are revenue and expense accounts (income statement accounts), the owner’s drawing account, and the income summary account. LESSON 8-2

TERMS all on page 206 of your text book page 212 • Closing Entries – Journal entries used to prepare temporary accounts for a new fiscal period. The temporary account balances must be reduced to ZERO at the end of each fiscal period. LESSON 8-2

NEED FOR THE INCOME SUMMARY ACCOUNT page 207 LESSON 8-2

(Debit to close) CLOSING ENTRY FOR AN INCOME STATEMENT ACCOUNT WITH A CREDIT BALANCE page 208 1. Write the heading. 2. Write the date. 3. Write the title of the account debited. Record the debit amount. 4. Write the title of the account credited. Record the credit amount. LESSON 8-2

(Credit to close) CLOSING ENTRY FOR INCOME STATEMENT ACCOUNTS WITH DEBIT BALANCES page 209 1. Date 2. Income Summary 3. Credit 4. Debit amount LESSON 8-2

(Capital: credit torecord net income) (Income Summary:debit to close) CLOSING ENTRY TO RECORD NET INCOME OR LOSS AND CLOSE THE INCOME SUMMARY ACCOUNT page 210 1. Date 2. Debit 3. Credit LESSON 8-2

(Credit to close) CLOSING ENTRY FOR THE OWNER’S DRAWING ACCOUNT page 211 1. Date 2. Debit 3. Credit LESSON 8-2

GENERAL LEDGER ACCOUNTS AFTER ADJUSTING AND CLOSING ENTRIES ARE POSTED page 213 LESSON 8-3

POST-CLOSING TRIAL BALANCE page 216 1. Heading 2. Account titles 3. Account balances 4. Single rule 5. Compare totals 6. Totals 7. Record totals 8. Double rule LESSON 8-3