Download

1 / 35

350 likes | 512 Vues

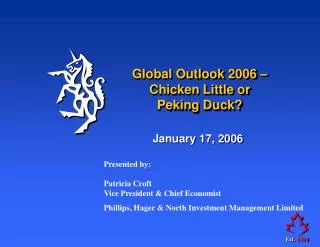

Global Outlook 2006 – Chicken Little or Peking Duck?. January 17, 2006. Presented by: Patricia Croft Vice President & Chief Economist Phillips, Hager & North Investment Management Limited. Outlook 2006 It’s All About Oil and Inflation. Global growth still healthy and better balanced

E N D

Global Outlook 2006 – Chicken Little or Peking Duck? January 17, 2006 Presented by: Patricia Croft Vice President & Chief Economist Phillips, Hager & North Investment Management Limited

Outlook 2006 It’s All About Oil and Inflation • Global growth still healthy and better balanced • Some improvement in Europe and Japan – Canada remains strong • Soaring energy prices have had little impact but… • Storm clouds on the horizon • Tightening Fed • Housing bubbles and yawning current account deficit • Protectionist sentiment • Energy prices

WTI Crude 70 60 50 40 US$/barrel 30 20 10 0 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 Crude Oil Prices Still Elevated – Chicken Little?

Long-term Price of Oil Has Increased – But to $45 not $100 • Days of $22-28/barrel are behind us • Global demand shift • Alternative resources take time to develop • Refinery capacity is limited and inadequate

Central bank monetary policy normalization 4.0 Tightening since trough 3.50 3.5 Tightening in last year Estimated distance from neutral 3.0 2.5 2.0 Percentage points 1.75 1.75 1.5 1.00 1.0 0.50 0.5 0.00 0.0 -0.5 U.S. Canada Australia U.K. Eurozone Japan Estimated neutal rate = LR core inflation target + LR potential real GDP growth rate Monetary Policy: Key Theme for 2006

300 250 U.K. Australia 200 U.S. Index, 1994Q1 = 100 Canada 150 100 50 1994 1996 1998 2000 2002 2004 House Prices Still High

Outside North America, Things Are Looking Up • UK in a soft spot but has likely bottomed • Europe doing better – interest rates still low • Japan improving – end of deflation in sight? • China still strong – now bigger and better • Global growth holding up but likely to ease in 2007 as lagged effects of rate hikes start to hit home globally

12 Retail sales 10 Manufacturing output 8 6 4 % change year ago 2 0 -2 -4 -6 -8 1997 1998 1999 2000 2001 2002 2003 2004 2005 UK Economy on the Mend?

Italy France Germany Real GDP Real GDP 20 20 Real GDP 20 Private expenditure Private expenditure Private expenditure Fixed Capital Formation Fixed Capital Formation Fixed Capital Formation Exports Exports Exports 15 15 15 10 10 10 5 5 5 0 0 0 -5 -5 -5 -10 -10 -10 2000 2001 2002 2003 2004 2005 2000 2001 2002 2003 2004 2005 2000 2001 2002 2003 2004 2005 Will 2006 Be Europe’s Year? Year-over-year % change

Japan’s Recovery – Is This the Real Thing? • Corporate profits are improving and business investment is increasing • Private consumption and employment are increasing moderately • Exports and industrial production are picking up • Risk is the impact of oil prices on both domestic and overseas economies

Japan's key export markets 40 35 32.1 33.7 30 28.1 23.4 25 Percent of total Export share, USA 20 Export share, China 14.1 15 Export share, Other Asia 10 5.1 5 0 Jul-05 Jul-01 Jul-02 Jul-04 Oct-04 Jul-99 Jul-00 Jul-03 Apr-01 Jan-01 Oct-05 Apr-99 Apr-00 Apr-02 Apr-03 Apr-04 Oct-03 Oct-01 Apr-05 Jan-99 Oct-99 Oct-02 Jan-04 Oct-00 Jan-02 Jan-00 Jan-03 Jan-05 Japan’s Reliance on China Growing but U.S. Still Top Dog

New GDP Old GDP Primary Primary 13% Tertiary 15% Tertiary 32% 41% Secondary Secondary 46% 53% $1.6 trillion US $1.9 trillion US = 20% increase! China Vaults to Number Four Global Economy Source: National Bureau of Statistics

China’s Far Reaching Impact • It has altered world trading patterns, shifting income • It has pressured wages of low skilled workers in rich countries • It has helped companies increase return on capital without pressure from workers for higher wages

U.S. Economy Remarkably Resilient • Despite higher oil prices, natural disasters and consumer worries, real growth still strong • Federal Reserve appears to be close to end of tightening cycle • Biggest risk: U.S. consumer • Negative personal savings rate • Rising debt servicing costs • Higher energy costs • Real estate reliant

US capacity indicators 90 2 4.9% 88 3 86 4 84 5 Cap U LR avg = 81.4% 82 6 % % 80 7 78 8 76 9 Capacity utilization rate, all industries (left) 74 10 Unemployment rate (right) 72 11 70 12 Q4 1983 Q1 1970 Q4 1972 Q3 1975 Q2 1978 Q1 1981 Q3 1986 Q2 1989 Q1 1992 Q4 1994 Q3 1997 Q2 2000 Q1 2003 Q4 2005 Why is the Fed Still Tightening?

Will the Fed Tighten Too Much? Source: ASeychuk

US yield curve slope - 10-year Treasury bond - 3-month T-bill 5 4 3 Percentage points 2 1 0 -1 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 Real US 3-month T-bill rates 7 6 5 4 3 % 2 1 0 -1 -2 -3 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 Yield Curve is Flat But Real Rates Still Low

US consumer price inflation 18 15 Core CPI 12 Headline CPI Percent, Year-over-year 9 6 3 0 -3 1960 1966 1972 1978 1984 1990 1996 2002 Core Inflation Well Behaved – So Far Source: ASeychuk

US Real House Prices 170 160 150 140 Index 130 120 110 100 90 1975 1980 1985 1990 1995 2000 2005 Source: Office of Federal Houising Enterprise Oversight, Bureau of Labor Statistics U.S. House Prices Continue to SurgeSustained low interest rates tend to fuel asset bubbles

250 12 Net equity extraction through cash-out refinancing 10 200 As a percent of disposable income 8 150 6 US$ Billions, quarterly rate 100 % of disp income 4 50 2 0 0 -50 -2 Q1 1990 Q2 1991 Q3 1992 Q4 1993 Q1 1995 Q2 1996 Q3 1997 Q4 1998 Q1 2000 Q2 2001 Q3 2002 Q4 2003 Q1 2005 Source: "Estimates of Home Mortgage Originations, Repayments, and Debt on One-to-Four Family Residence”, Kennedy and Greespan, Federal Reservce 2005 U.S. Consumer Using Home as a Cash Machine

US Dollar and Current Account Balance 2 150 1 140 0 130 -1 120 -2 % of GDP Index 110 -3 100 -4 90 -5 % of GDP (left) 80 Trade-weighted value of US dollar -6 against major currencies (right) -7 70 1973 1975 1978 1980 1983 1985 1988 1990 1993 1995 1998 2000 2003 2005 Current Account Deficit Still a Dollar Risk

Canadian Economic Growth Strong But Unbalanced • Higher energy prices benefit Canada as we are a net energy exporter • However, high energy prices create a transfer of wealth from central Canada to Alberta • The Canadian dollar has become a petro currency – a stronger dollar will further challenge the manufacturing base • Fiscal policy is loose – monetary policy is tightening

Cumulative job creation since January 2004 500 450 Total 400 Full-time 350 300 Thousands 250 200 150 100 50 0 Jul-04 Jul-05 Jan-04 Jan-05 Nov-04 Nov-05 Mar-04 Mar-05 Sep-04 Sep-05 May-04 May-05 Canadian Job Creation Has Been Very Strong

Provincial labour markets 2006 provincial real GDP growth 7 16 Unemployment rate (ytd avg %) 14 6 Job growth (ytd % change) 12 5 10 4 % 8 % 3 6 4 2 2 1 0 0 -2 BC AL SK MB ON QC NB NS PEI NL NL PEI NB NS QC ON BC SK MB AL Source: RBC Financial Group Provincial retail sales and housing Provincial price pressures 9 15 Retail sales (ytd % change) CPI (ytd avg %) Housing starts (ytd % change) 8 Wages & salaries (ytd % change) 10 7 6 5 5 % % 0 4 -5 3 2 -10 1 -15 0 AL SK MB QC NB BC ON PEI NS NL PEI NS MB NL NB QC SK ON AL BC Alberta Roars While Central Canada Reels

Capacity utilization and unit labour costs Capacity utilization 90 8 Unit labour costs 88 6 86 84 4 82 Annual % change % 2 80 78 0 76 -2 74 72 -4 1987 1990 1993 1996 1999 2002 2005 Canadian Inflation Indicators Flashing Yellow

Canadian CPI inflation 5.0 Core (excl. 8 most volatile items) 4.5 Headline 4.0 3.5 3.0 % 2.5 2.0 1.5 1.0 0.5 0.0 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 For Now – Inflation Remains Tame

Central bank policy interest rates 7 6 5 Bank of Canada U.S. Federal Reserve 4 (%) 3 2 1 0 2001 2002 2003 2004 2005 Bank of Canada Back in Tightening Mode

Performance of the Canadian dollar in 2005 20 Change in value against selected currencies from Jan. 1 to Dec. 31 2005 18 16 14 12 % 10 8 6 4 2 0 U.S dollar New Zealand dollar Australian dollar UK pound Euro Yen Canadian Dollar Was A Star in 2005

Outlook 2006 - Summary • Global growth set to slow as weakness in the U.S. is partially offset by renewed vigor in Europe and Japan • Canada strong for now – growing regional disparities will challenge policy makers • Monetary policy normalization process to continue • C$ overvalued – U.S. bear market at hand • Risks • Energy prices/house prices • Geopolitical instability • Mother Nature • Protectionist sentiment

CBOE Volatility Index (VIX) 60 Old VIX (based on S&P 100) Black Monday New VIX (based on S&P 500) 55 50 LTCM 45 Above 40 = Panic 40 Gulf War II Index 35 9-11 Asian Crisis Gulf War I 30 25 20 15 Below 20 = Complacency 10 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 Easy Monetary Policy has Encouraged Risk Taking

Yield curve slope, current and year ago 250 year ago current 200 150 10 year - 3 month yields, bps 100 50 0 -50 Japan Eurozone Canada US UK Global Yield Curves Flattening

10-year government bond yields 7.0 2.5 6.5 2.0 6.0 5.5 1.5 5.0 % % 4.5 1.0 Canada (left) 4.0 US (left) 3.5 0.5 Germany (left) Japan (right) 3.0 2.5 0.0 2000 2001 2002 2003 2004 2005 Source: Datastream Long Bond Yields Still Low and Range Bound

Major stock markets since Jan. 2004 160 S&P 500 150 S&P/TSX MSCI EAFE (US$) 140 Nikkei 225 Index: Jan. 1 2004 = 100 130 120 110 100 90 Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Japan Soars – U.S. Sputters

28 26 24 S&P 500 TSX 22 MSCI EAFE Ratio 20 18 16 14 12 1998 1999 2000 2001 2002 2003 2004 2005 P/E Ratios Have Converged

Asset Mix Summary • Overweight equities, neutral on bonds, underweight cash • May add to U.S. or EAFE equity holdings • Corporate earnings still strong – corporations flush with cash • Valuation for stocks is reasonable, particularly in the U.S. • Proximity to end of Fed tightening cycle is a positive factor