Download

1 / 63

670 likes | 1.09k Vues

Understanding the Harvard Chart of Accounts. Your Roles and Responsibilities. As a Harvard employee with financial transacting and/or reporting responsibilities: This course will help you build basic skills needed to carry out these responsibilities.

E N D

Your Roles and Responsibilities As a Harvard employee with financial transacting and/or reporting responsibilities: This course will help you build basic skills needed to carry out these responsibilities • You are responsible for ensuring that University monies are spent and accounted for: • In accordance with University policies • In accordance with donor or sponsored terms • Your transactions impact University-wide reports like the Balance Sheet and the Statement of Changes in Net Assets

Course Goals After finishing this course, you will be able to: • Describe the purpose and importance of the Chart of Accounts (CoA) • Explain the information that is tracked by each segment of the Chart • Determine the appropriate 33-digit coding for basic transactions in your area • Describe how local transactions impact University-wide reports

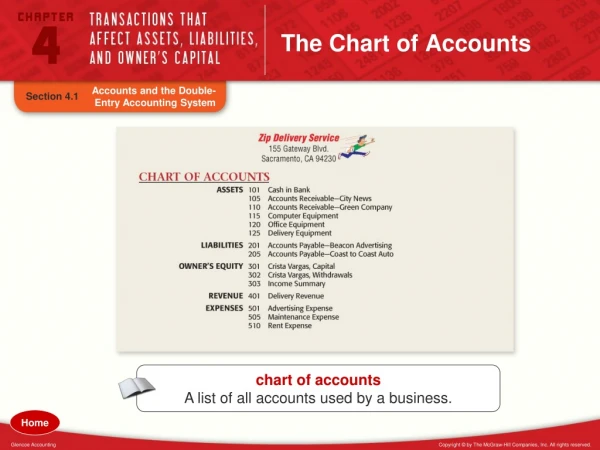

What Is the Chart of Accounts (CoA)? • A 33-digit code that accompanies every financial transaction at the University • An organizing framework used to: • Establish and track budgets • Record details about income and expenses • Provide accurate and consistent financial reports across schools • Ensure that accounting regulations, donor restrictions, and sponsored requirements are met

Tub Org Fund Object Activity Root Which account the transaction involved and if it impacted any restricted funds What the funds were used for and if a faculty member was involved Which school and department created the transaction What type of income or expense the transaction represented What Does the CoA Tell Us? Sub- activity

Chart of Accounts Unit 1: Tubs & Orgs

Tub The Segments - Tub Tub is the first segment of and has three digits • Tub represent the highest financial reporting levels at Harvard and are usually schools or high-level units • Examples include: HLS, GSE, SPH, and Central Administration • Several of the larger schools contain more than one tub • There are over 70 tubs at Harvard • A full list can be found at: http://able.harvard.edu/coa/coa_index.shtml • Tub is a required field

Org The Segments – Org Org is the second segment and has five digits • Orgs identify financial groups within a tub, usually departments within a school or administrative unit • Examples include the Microbiology department in HMS or the Center for Workplace Development in Central Admin • New orgs are set up by a tub’s financial office • Org is a required field

Org Tub Org Naming Conventions Tub Org Org Name 215 . 16450 “KSG^Admissions” 255 . 20825 “GSE^Publications” “HMS^Genetics” 520 . 45314 “CADM^Accounts Payable VPF” 610 . 56232 Details about the naming conventions for each segment can be found at: http://able.harvard.edu/coa/qr/coa-naming-conventions.pdf

Ranges Values that belong to a single unit are grouped together in numerical ranges to make them easier to identify For example: the Orgs belonging to the Graduate School of Education are all grouped in the numerical range 20600 - 21099. GSE^Grad School of Education Tub 255 GSE^Academic Support Org 20601 GSE^Progs in Prof Ed Org 20870 GSE^Student Affairs Org 20780

Chart of Accounts Unit 2: Classifying Transactions With Object Codes

The Segments - Object Object Object is the third segment and has four digits Object Codes: • Identify the nature of the transaction • Generally change most often between transactions • Are grouped by categories and ranges • Are established by Central Administration • Object is a required field

Harvard’s Object Code Categories Object Code Category Range Assets 0001 - 1999 Liabilities 2000 - 3699 Net Asset Balances 3700 - 3999 Revenue (Income) 4000 - 5999 Expenses 6000 - 8999 Non-operating activity 9000 - 9999

Range for Assets0001 - 1999 Assets • An asset is something of value that the University owns or controls, such as: • Cash • Investments • Buildings and Land • Money owed to Harvard (accounts receivable)

Range for Liabilities2000 - 3699 Liabilities • Liabilities are claims against the University, or money it owes • Bills to be paid for goods or services already received (accounts payable) • Debt • Pension • Security deposits

Range for Net Asset Balances3700 - 3999 Net Asset Balances • The difference between what Harvard owns and what it owes is called “net assets” • Balances in object codes 3700-3999 represent the beginning of the fiscal assets and are calculated each operating and endowment fund Net Asset Balance object code balances may not be changed during the year.

Range for Revenue4000 - 5999 Revenue (Income) • Revenue is income received to support the work of the University. • Examples include: • Tuition • Gifts for current use • Sponsored grants & contracts • Endowment income distributions • Other miscellaneous income • Sales of goods, health clinic fees, admissions, parking, rent, etc.

Expenses Range for Expenses6000 - 8999 • The costs of most goods or services purchased in the course of conducting University business are called expenses. Examples include: • Salaries & wages • Employee benefits costs • Scholarships & student awards • Supplies, materials & equipment • Space & occupancy costs • Depreciation • Other expenses

Are All Expenditures “Expenses”? • Most expenditures are expenses but some are for assets • Assets generally have a significant cost and lasting value • Equipment and furniture purchases use separate sets of expense object codes for purchases where the unit cost is: • under $5,000 (expense costs) or • greater than or equal to $5,000 (capitalized costs) • Larger purchases may be considered capital projects

Am I Buying An Asset? Are you purchasing equipment, software, computers, furniture, fixtures, or vehicles? Yes No Noncapitalized Expense Object codes 6710 - 6769, 6780 - 6789 Does the item cost less than $5,000? Are you purchasing a building or land? Asset Call your financial office for details Yes Yes No No Asset Call your financial office for details Is the item financed by a loan? Are you making capital improvements worth more then $100,000? Potential Asset Call your financial office for details Yes Yes No No Capitalized Expense Object codes 6801 - 6869 Expense Use standard expense object codes

Range for Non-operating Activity9000 - 9999 Non-operating activity Non-operating activity object codes include transactions that are not reported as part of the University’s operations. These are known as “below the line” activities and include items like: • appreciation on investments • fund balance transfers • endowment capitalizations or decapitalizations Non-operating activity object codes are generally transacted to by Central Administration only

Special Types of Object Codes • Parent and Child Roll-Up codes • General and Detailed codes • Central-only object codes • Budget-only codes • “Unallowable” expense codes • Internal transfer codes

8511 - Local Telephone Usage 8512 - Long Distance Usage 8513 - Telephone Lines 8514 - One-Time Charges 8515 - Phone Repair & Maint. 8516 - Communications Equip. S851 - Telephone + Telecommunications Expenses You could report on the totals of each separate (Child) code: Or you could report on total of the Super (Parent) code: Roll-Up or “Parent” Object Codes While transactions are recorded in distinct object codes, roll-up codes also exist to help organize related expenses into groups for better reporting.

Object Code Roll-Up Levels Rollup Levels Sample Expense Object Codes Level of Reporting Tera T600 Total Expenses Summary of all expenses G601 Salaries G760 Other Expenses G650 Supplies Giga Financial Statement M853 Reproduction M846 Telephone M764 All Travel Higher-level Summaries Mega Super (Parent) S765 Domestic Travel S767 Foreign Travel Lower-level Summaries 7651 Airfare^ Domestic Travel 7652 Lodging^ Domestic Travel 7671 Airfare^ Foreign Travel 7672 Lodging^ Foreign Travel Transaction- level (Child) Individual Expenses (data entry level)

7651 - Airfare^ Domestic Travel 7652 - Lodging^ Domestic Travel 7650 Domestic Travel, GENERAL 7653 - Ground Transportation^Domestic Travel 7654 - Meals + Incidentals ^ Domestic Travel 7655 - Business Meals + Entertainment^ Domestic Travel General vs. Detailed Object Codes General expenses vs. Detailed expenses Which you should use depends on… • University policies • Funding agency requirements for sponsored transactions • Tub or department level reporting requirements

Central-Only Object Codes • Certain object codes can only be used by Central Admin • For assets and liabilities, “CO” is in the title • e.g. 0070 - CO^Student Receivables • For income, expense, and non-operating object codes, “CO” is not in the title but can be found in the unabridged object code listing at: http://able.harvard.edu/coa/csma/userguide/unabridged-object-code-list.xls • Tubs CAN report on the activity in these object codes, even through they cannot transact to them If you choose one of these codes for a transaction and you do not have proper access, the system will return an error message.

Budget-Only Object Codes • Represent high-level categories used for budgeting purposes only. You may not transact directly to these codes. • Are followed by the phrase “Budget Only” If you choose one of these codes for an income or expense transaction, the system will return an error message.

“Unallowable” Expense Object Codes • The University receives research funding from the government which includes funding for both direct and indirect costs • The government will not reimburse, either directly or indirectly, certain kinds of expenses • These are called “expenses ineligible for federal reimbursement” • All “ineligible” expenses must be charged to object codes 8450 (General) or 8451-8459 (Detailed) • Individuals can be reimbursed for these expenses by Harvard (when appropriate) but the expenses must be charged to 8450 so that they do not impact either direct or indirect federal funds • All spending from University funds or sponsored funds is subject to these rules

Unallowable Expenses • Expenses ineligible for federal reimbursement include: • Alumni activities • Antiques, art, or decorative objects for private offices • Bad debts • Business-related entertainment • Charitable contributions • Employee celebratory events • Flowers • Fines and penalties • Fundraising or commencement expenses • Gifts and awards to Harvard employees and non-Harvard personnel • Institutional advertising and promotion, including printed materials • Liquor, including liquor purchased with a meal • Lobbying, including memberships in lobbying organizations Complete details about unallowable expenses can be found on the Office of the Controller’s Policy Page at: http://vpf-web.harvard.edu/ofs/policies/policies.shtml

Internal Transfers • Departments occasionally need to transfer funds between University accounts • This can be done to support interdepartmental activities, assess administrative fees, or transfer costs • Certain rules must be followed to make sure that internal transfers: • Do not increase University income or expense • Do not cause misstatements of a unit’s operating results • Are not used to transfer donated money out of a fund

Internal Transfer Rules • To ensure compliance with University accounting policy, all transfers must either: • Debit and credit an income object code, • Debit and credit an expense object code, or • Debit and credit a non-operating transfer code • There are also many restrictions on transferring funds from gift accounts into unrestricted accounts

Internal Transfer Types INTER: Between two tubs INTRA: Within a tub Intra-tub Copying fees charged by one FAS org to another FAS org Inter-tub Telephone charges from UIS to FAS If you deal with internal transfers, please refer to the “Internal Transfers” policy for the complete rules and guidelines. It can be found at: http://vpf-web.harvard.edu/documents/fa_intrans104.pdf

Internal Transfer Exceptions If... Then... You will not use internal transfer object codes since these units are treated as external entities Your transaction is with Tub: • 130 - Harvard Magazine • 185 - Agencies • 190 - Yenching • 295 - American Repertory Theatre • 455 - HBS Research Centers • 595 - HPRE 3rd Party These are non-consolidated tubs which are treated the same as external entities since they are not included in the University’s annual Financial Statements.

Chart of Accounts Unit 3: Sources and Uses of Harvard’s Funds

Fund Accounting Basics • Fund Accounting is common to all non-profit organizations • Many funds have restrictions on how they can be used based on donor, sponsored, or departmental stipulations • Expenses from a restricted fund must comply with all donor or sponsored restrictions or we cannot use the money • Harvard’s CoA allows tracking of funds by source though the fund segment

The Segments - Fund Fund Fund is the fourth segment and has six digits • The fund value identifies the source of the money • There are more than 32,000 active funds • Fund is a required field when you are using object codes between 3700 and 9999 • Contact your tub Chart Administrator if you have questions about setting up a new fund in your tub

Fund Types and Ranges The major types of funds are: General Unrestricted Undesignated000001 General Unrestricted Designated 000002 Unrestricted Undesignated 000003 - 001999 Unrestricted Designated 002000 - 054999 Sponsored Support100000 - 299999 Gifts (unrestricted & restricted)300000 - 399999 Endowment (unrestricted & restricted)400000 - 699999 Other Fund Balances 700000 - 749999

Unrestricted Undesignated Funds Unrestricted undesignated funds have NO donor restrictions and are free to use for any purpose. • Unrestricted undesignated accounts include: • Undesignated funds 000001 and 000003-001999 • Gift funds 300000-301999 • Endowment funds 400000-429999 • If not used, year-end balances roll into tub’s fund000001 • Use fund000001for all expenditures from these funds

Unrestricted Designated Funds Unrestricted designated funds have no donor restrictions but have been designated for a specific purpose. • Unrestricted monies may be earmarked for a specific purpose by a department or the University • Each fund carries forward in a separate fund balance • Unrestricted designated accounts include: • Funds 000002 and 002000-054999

Restricted Funds • Funds may have restrictions based upon donor or sponsored requirements • Restricted gift funds 302000 - 399999 • Restricted endowment funds 430000 - 699999 • Sponsored funds 100000 - 299999 • It is essential to ensure that restricted funds are spent in accordance with the terms set forth by the donor or sponsor • More information about restricted funds is covered in the Intro to Harvard Accounting class

Chart of Accounts Unit 4: Identifying What and Who – Activities, Subactivities, and Roots

The Segments - Activity Activity Activity is the fifth segment and has six digits • It identifies the project or effort for which the money is being used • It also identifies the type of function for which the expense is incurred • e.g., instruction, research, administration, etc. • Activity is a required field for all expense transactions • Contact your tub Chart Administrator if you have questions on setting up a new activity in your tub

Activity Examples • Sponsored research • Course • Conference • Project • Seminar • Publication • Office Administration

Activity Types and Ranges Used with these types of Object Codes Range Activity Type Construction in Progress 001000 - 099999 Asset / Liability Other Balance Sheet 100000 - 199999 Asset / Liability Sponsored 200000 - 499999 Income / Expense Other Income & Expense 500000 - 899999 Income / Expense

A-21 Functional Reporting • The U.S. Office of Management and Budget (OMB) identifies reporting categories that organizations which receive federally sponsored research money must use to track their activities • These categories are listed in the OMB’s Circular A-21 • Each income/expense activity code in the CoA has been assigned an A-21 function code • All expenses – including charges to non-sponsored funds – must be coded to an activity with the correct function

A-21 Functional Categories A01 INSTRUCTION & DEPARTMENTAL RESEARCH A02 ORGANIZED RESEARCH A03 OTHER SPONSORED ACTIVITIES A04 OTHER INSTITUTIONAL ACTIVITIES A04-1 FUNDRAISING / DEVELOPMENT A04-2 AUXILIARIES A05 SERVICE/RECHARGE CENTERS A06 GENERAL ADMINISTRATION & GENERAL EXPENSE A07 DEPARTMENTAL ADMINISTRATION A08 SPONSORED PROJECTS ADMINISTRATION A09 STUDENT ADMINISTRATION & SERVICES A10 FACILITIES OPERATION & MAINTENANCE EXPENSES A11 FACILITIES LIBRARY EXPENSES A12 FACILITIES DEPRECIATION & USE ALLOWANCES A13 FACILITIES INTEREST A14 FRINGE BENEFITS A15 SCHOLARSHIPS & STUDENT AID

Generic A-21 Activity Example Activity Value: 780008 CADM^ (A6) General Admin+General Expense Tub prefix Generic functional description OMB A-21 functional code All operating tubs have a set of generic A-21 functional activities

Specific A-21 Activity Examples Activity 346483 (Sponsored Research) FCOR^ A02 NIH-NIMH Panic & Cognition PSYC A-21 code Sponsor short name Tub prefix Award title Key Word Activity 628350 (Non-Sponsored Expenses) FCOR^ Network Architecture (A04) FASCS Keyword Tub prefix Description of the activity A-21 code

The Segments - Subactivity Sub- activity Subactivity is the sixth segment and has four digits Subactivity values: • Help identify different tasks, phases, or subcategories in an activity • Are dependent on the activity value • Are required for sponsored funds (100010 – 299999) • Contact your tub Chart Administrator if you have questions on setting up a new sub-activity value

Subactivity Example Sub- activity Activity • Activity: CADM^Estate Planning Seminar • Subactivity is used to track expenses by location Activity Subactivity Subactivity Name 7804510000780451^Unspecified 0001780451^Boston 0002780451^New York 0003780451^Washington