Download

1 / 5

0 likes | 1 Vues

Your credit score plays a critical role in your financial journey. Whether you're applying for a loan, renting an apartment, or even securing a job, your credit history often speaks before you do. Among the many scoring models out there, FICO Credit Score is the most widely used by lenders and creditors across the United States. But what exactly is a FICO score, and how does it impact your financial life?<br>

E N D

Understanding FICO Credit Score: A Complete Guide Your credit score plays a critical role in your financial journey. Whether you're applying for a loan, renting an apartment, or even securing a job, your credit history often speaks before you do. Among the many scoring models out there, FICO Credit Score is the most widely used by lenders and creditors across the United States. But what exactly is a FICO score, and how does it impact your financial life? This guide offers a deep dive into the FICO credit score, how it's calculated, why it matters, and how you can improve it for better financial outcomes.

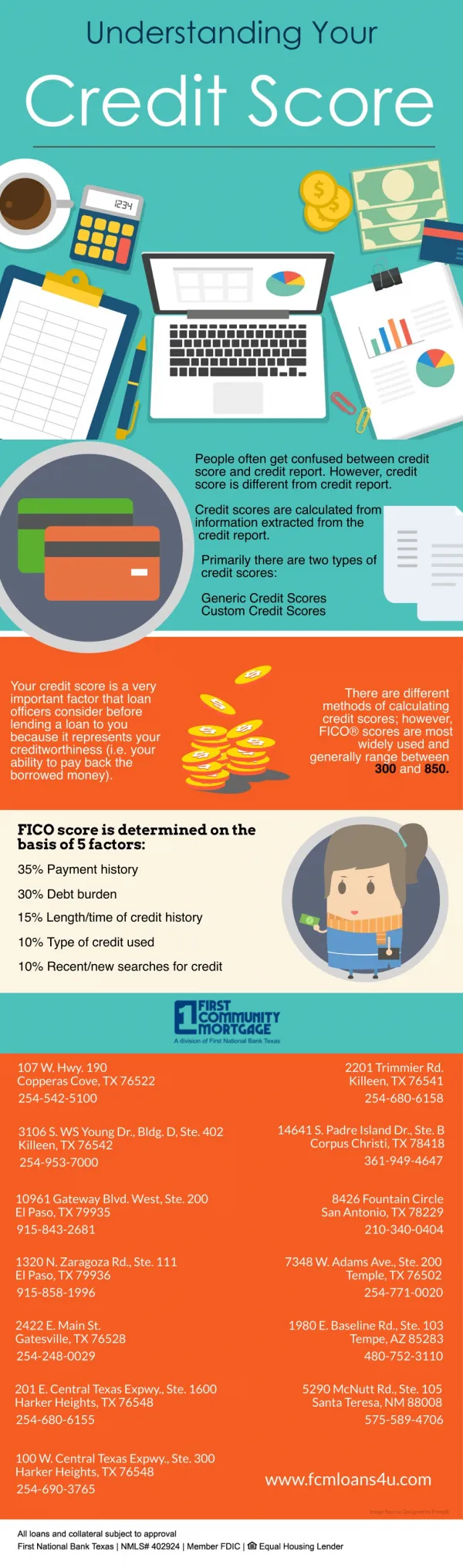

What is a FICO Credit Score? A FICO credit score is a three-digit number, typically ranging from 300 to 850, that summarizes your creditworthiness. Developed by the Fair Isaac Corporation (FICO), it helps lenders evaluate how likely you are to repay a loan based on your credit history. The higher your FICO score, the lower the credit risk you pose to lenders. More than 90% of top lenders in the U.S. use FICO scores when making lending decisions, including banks, mortgage companies, credit card issuers, and auto finance companies. FICO Score Ranges FICO scores fall within the following ranges: ● 300–579: Poor Applicants may be considered high-risk and may not qualify for loans or may face higher interest rates. ● 580–669: Fair Subprime borrowers—some lenders may approve loans, but terms are usually less favorable. ● 670–739: Good This score is considered acceptable and most lenders will approve credit with decent terms. ● 740–799: Very Good Borrowers are considered low risk and typically qualify for better interest rates. ● 800–850: Exceptional Excellent credit profile—borrowers often receive the best available loan terms. Why is Your FICO Score Important? Your FICO credit score influences nearly every major financial decision you make. Here's how: ● Loan Approvals: Higher scores increase your chances of getting approved. ● Interest Rates: A good score can save you thousands of dollars over the life of a loan. ● Credit Card Offers: Better scores often result in higher limits and lower rates. ● Rental Applications: Landlords use FICO scores to screen tenants.

● Employment Opportunities: Some employers review credit scores for roles involving financial responsibility. In short, your FICO score can determine the financial opportunities available to you and the cost of those opportunities. What Factors Affect Your FICO Score? FICO calculates your score based on five key credit categories: 1. Payment History (35%) The most critical factor—this reflects whether you’ve paid your credit accounts on time. Late payments, delinquencies, and accounts sent to collections negatively affect this portion. 2. Amounts Owed (30%) This refers to your credit utilization ratio—the amount you owe compared to your total credit limit. Keeping balances below 30% of your limit is considered ideal. 3. Length of Credit History (15%) A longer credit history boosts your score. It takes into account how long your accounts have been open, especially your oldest account. 4. New Credit (10%) Opening too many new credit accounts in a short time can be seen as risky and may lower your score temporarily. 5. Credit Mix (10%) Having a variety of credit types—credit cards, retail accounts, installment loans, mortgage loans—demonstrates your ability to manage different forms of credit. Types of FICO Scores There isn’t just one FICO score; there are multiple versions used for different lending purposes: ● FICO Score 8: Most commonly used model by general lenders. ● FICO Score 9: Includes newer data points like rental payments. ● Industry-specific scores:

○ FICO Auto Score (used by auto lenders) ○ FICO Bankcard Score (used by credit card issuers) These scores may range from 250 to 900. It’s important to note that your score can vary depending on which version is used and from which credit bureau the data is pulled Equifax, Experian, or TransUnion. How to Check Your FICO Score You can obtain your FICO score through: ● Your bank or credit card issuer (many offer it for free). ● Official FICO website (myFICO.com) for detailed reports. ● Credit monitoring services. While checking your credit score using these methods doesn’t affect your score, a hard inquiry—such as one made by a lender during a loan application—may temporarily lower it. Tips to Improve Your FICO Credit Score Boosting your FICO score takes time and discipline. Here are practical ways to improve it: Pay Bills on Time Your payment history makes up 35% of your score. Set reminders or enable auto-pay to avoid missed payments. Reduce Credit Card Balances Aim to use less than 30% of your credit limit and pay off balances in full when possible. Avoid Unnecessary New Credit Applications Only apply for credit when necessary to reduce hard inquiries. Keep Old Accounts Open Even if you no longer use a credit card, keeping it open can help with credit history length and utilization. Diversify Your Credit Mix

If you only have credit cards, consider adding a small personal loan or auto loan to improve your mix. Common FICO Credit Score Myths Myth 1: Checking your credit lowers your score. Truth: Soft inquiries (like checking your own score) do not affect your FICO score. Myth 2: You must carry a balance to build credit. Truth: You don’t need to carry a balance or pay interest to build your credit. Myth 3: Closing old accounts improves your score. Truth: Closing old accounts may shorten your credit history and increase utilization, both of which can hurt your score. Why FICO Over Other Scores? While there are other scoring models like VantageScore, the FICO score remains the industry standard because: ● It's been around since 1989. ● It's used in over 90% of lending decisions. ● It’s trusted by all three major credit bureaus. For consumers, understanding your FICO score is the best way to track and manage your credit health effectively. Conclusion Your FICO credit score is one of the most important indicators of your financial reputation. Maintaining a good score can open doors to low-interest loans, premium credit cards, and even better housing or job opportunities. By understanding the components of your FICO score and taking proactive steps to improve it, you can take full control of your financial future. Start managing your credit responsibly today! For more information call and email us: ?Call Us Now:(321) 613-8418 ?Email: info@ecocreditgroup.com ?Website:https://www.ecocreditgroup.com/ ?Location:3000 Stirling Rd Hollywood, FL 33021