VALUE INITIATIVE PROGRAM

390 likes | 561 Vues

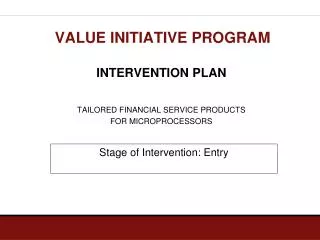

VALUE INITIATIVE PROGRAM. INTERVENTION PLAN TAILORED FINANCIAL SERVICE PRODUCTS FOR MICROPROCESSORS. Stage of Intervention: Entry. INTERVENTION RATIONAL. TAILORED FINANCIAL SERVICE PRODUCTS FOR MEs.

VALUE INITIATIVE PROGRAM

E N D

Presentation Transcript

VALUE INITIATIVE PROGRAM INTERVENTION PLAN TAILORED FINANCIAL SERVICE PRODUCTS FOR MICROPROCESSORS Stage of Intervention: Entry

INTERVENTION RATIONAL • TAILORED FINANCIAL SERVICE PRODUCTS FOR MEs • The financial package for Equipments will contributetowards increased MEs output and sales (enterprise level change), increased ME participation and market output (VCD change) and increased productivity and access to local markets amongst the excluded poor and HIV affected communities in urban areas (social change) . • MICROPROCESSORS/VENDORS ACCESS EQUIPMENT INCREASE IN JUICE OUTPUT AND SALES SOCIAL CHANGE ENTERPRISE LEVEL CHANGE VCD CHANGE

MARKET ANALYSIS • Passion fruit is a very popular fruit in the domestic market either used as fresh fruit or for processing into juices. • Demand in East African markets for fresh and processed fruit products such as passion fruit juice is growing at more than 10% per annum. In Kenya, domestic demand is increasing and current supply is unable to fill the demand. • The leading passion fruit processors in Kenya include Kevian Ltd, Milly processors and FIPS Ltd, Ruaraka.

MARKET ANALYSIS • Extensive juice extraction is also carried out at household and cottage industries. Passion, orange, mango, papaya are the major processed and utilized fruit juices. • At micro-value add level, processing is done manually or by use of juice blenders bought from local supermarkets. • Value addition of passion fruits through micro processing presents an excellent opportunity to create new investment and employment for the poor Ampath clients in urban and peri-urban settings

MARKET ANALYSIS • However, inadequate access to credit for equipment is a generic constraint amongst micro value add enterprises in Kenya , contributing to low production volumes and poor juice quality • In addition entrepreneurs may also not know where to get the processing equipment and better linkages need to be created between the technology providers and users. • Majority of Kenyan consumers may not be aware of nutritional and health benefits of consuming passion fruit products or other natural fruit products as compared to synthetic or imitation products • VIP Ampath through Fintrac has recently launched a detailed market research initiative on the passion fruit value addition to among others study financial markets and potential financing models. (See attached market study plan) • Some preliminary research on financial markets reveals the following …………..

MARKET ANALYSIS Microprocessors Financing Needs – The Demand Side: • Typical amounts ranges from Kes 10, 000 - 200,000 • The rationales for these financing needs are extremely varied. They include: • purchasing equipment and licenses; • building up of working capital; and • hiring and training of personnel

MARKET ANALYSIS Demand side constraints • Lack of adequate information, communication and dissemination of information on availability of SMEs financing • Complex bank procedures that require reading and writing skills • Lack of entrepreneurial skills and management capacity to amongst SMEs • The costs of getting a loan are high, interest rates are very high • Lack of formal collateral • Lack of registered credit history and business records

MARKET ANALYSIS Issues in Accessing Financing by Microprocessors – The Supply Side • Small and short-term loans initially required by small businesses are considered costly and of high risk by formal financial institutions • High loan delinquency amongst SMEs • Need to train most MFIs operational staff and management to appreciate and be able to handle financial services requirements of SMES • Policy and regulatory constraints

MARKET ANALYSIS Issues in Accessing Financing by SMEs – The Supply Side cont’d…. • Absence of credit referencing systems in the country/credit history. • Lack of cost-effective ways to quantify credit risk-most banks limit their risk with the SME market either by not lending at all or by charging high interest • Many SMEs are reluctant to seek credit/loan phobia

MARKET ANALYSIS Sources of financing for SMEs in Kenya: • Banks, MFIs e.g.: K-Rep Bank, Equity Bank, Family Bank, Cooperative Bank and FINA Bank • SACCOs • Rotating and Savings Credit Associations (ROSCAs) • Accumulated Savings and Credit Associations (ASCAs) • Village Banks, friends and family, and informal lenders • Non Governmental Organizations

MARKET ANALYSIS Willingness and ability to pay for Credit Are urban SMEs able and willing to pay for credit? Main categories of urban SMEs that VIP Ampath is targeting: • Microprocessors who are able and willing to pay for credit:- Once exposed to suitable financial service products (e.g. equipment package) from finance institutions, they are enthusiastic about it and willing to pay. • Their sources of repayment include: • Microenterprise income. • Sale of assets • Household members’ salaries and other earned income • Remittances or domestic money transfers

MARKET ANALYSIS (2) Resource poor and vulnerable Ampath clients in urban settings: • These are the very poor and vulnerable of AMPATH clients (PLWAS) without formal bank collateral • VIP Ampath will assist them to graduate to micro-processing via a stepped –up approach [see next slide] • VIP Ampath will negotiate with Equity bank to accept collateral substitutes such as group liability/social guarantee for the clients, household items and or their credit history/reputation with Ampath.

Sequencing for Graduation to Micro-processing for the Poor Ampath Clients in Urban and Peri-urban Areas Stage 2 Vulnerable Graduation Stage 1 Very poor and Vulnerable TRAINING • juice processing technology, hygiene/quality, Biz Management • FACILITATION • KBS certification, municipal biz permit, credit & savings, public health certification • Experienced, rents a room or buys cool box, • savings requirement • . • Increased production capacity, • Increased income • Graduation to a microprocessor and business service markets • . • OUTPUT • 1 glass ready to drink is KES 40 (200ml) or KES 200/liter; aim for revenue of KES 4, 000 /day. Approximately KES 2, 000 /day.

INTERVENTION General StrategyWorking with financial institutions to develop suitable financial packages/products and stimulating demand in the value chain.

BUSINESS MODELS FOR FINANCIAL SERVICE PRODUCTS MICROPROCESSORS • Equipment and Training • Equipment- Such as blenders KIRDI-TECHNOLOGY DEVELOPER & TRAINER • SUPERMARKET • (TECHNOLOGY • DISTRIBUTER) • Loan repayment • Equipment • Loan repayment • Microprocessors • Financial • Package • Microprocessors • Financial • Package 1 2 • FINANCIAL INSTITUTIONS: ROOT SOURCES OF FIINANCE • Financial institution provides Equipment loans to microprocessors via the technology developer. Microprocessors repay the loan directly to the bank • Financial institution provides Equipment loans to microprocessors via the technology distributor Microprocessors repay the loan directly to the bank 1 2

CAUSAL CHAIN FOR TAILORED FINANCIAL SERVICE PRODUCTS FOR MICROPROCESSORS/VENDORS – PILOT PHASE % increase in # of MEs participating in value chain; % increase in market output BUSINESS MODEL # 1 % increase in monthly sales volume/value per vendor/MP MFI provides equipment loans to microprocessors/juice vendors via a technology developer/ training provider. Microprocessors repay the loans directly to the MFI % increase in monthly output of quality Juice # of vendors/MPs accessing and using equipment Equipment and training Equipment Loan INDICATORS Microprocessors/Vendors Technology developer MFI Loan repayment

CAUSAL CHAIN FOR TAILORED FINANCIAL SERVICE PRODUCTS FOR MICROPROCESSORS/VENDORS – MARKET UPTAKE PHASE % increase in # of MEs participating in value chain; % increase in market output BUSINESS MODEL # 1 % increase in monthly sales volume/value per vendor/MP MFI provides equipment loans to microprocessors/juice vendors via a technology developer/ training provider Microprocessors repay the loans directly to the MFI % increase in monthly output of quality Juice # of vendors/MPs accessing and using equipment Equipment and training Equipment Loan INDICATORS Many microprocessors /Vendors Technology developer Many MFIs Loan repayment

CAUSAL CHAIN FOR TAILORED FINANCIAL SERVICE PRODUCTS FOR MICROPROCESSORS/VENDORS – PILOT PHASE % increase in # of MEs participating in value chain; % increase in market output BUSINESS MODEL # 2 % increase in monthly sales volume/value per vendor/MP MFI provides equipment loans to microprocessors/juice vendors via a technology distributer. Microprocessors repay the loans directly to the MFI % increase in monthly output of quality Juice # of vendors/MPs accessing and using equipment Equipment Equipment Loan INDICATORS Microprocessors/Vendors Technology Distributer MFI Loan repayment

CAUSAL CHAIN FOR TAILORED FINANCIAL SERVICE PRODUCTS FOR MICROPROCESSORS/VENDORS - MARKET UPTAKE % increase in # of MEs participating in value chain; % increase in market output BUSINESS MODEL # 2 % increase in monthly sales volume/value per vendor/MP MFI provides equipment loans to microprocessors/juice vendors via a technology distributor. Microprocessors repay the loans directly to the MFI % increase in monthly output of quality Juice # of vendors/MPs accessing and using equipment Equipment and training Equipment Loan INDICATORS Many microprocessors /Vendors Technology distributor Many MFIs Loan repayment

Business Models to be tested • Financial institutions provide Equipment loans to microprocessors via the technology developer. Microprocessors repay the loan directly to the bank • Financial institutions provide Equipment loans to microprocessors via the technology distributor. Microprocessors repay the loan directly to the bank PILOT PHASE

Who will be involved? Core partners: VIP consortium, microprocessors/vendors, technology developer (KIRDI) and distributors (supermarkets) and MFIs. Other development agencies in the piloting areas (e.g. HCDA, FPEAK, KEPHIS, KARI, MOA, NGOs) will be involved in supporting the initiative.

KENYA INSTITUTE OF RESEARCH AND DEVELOPMENT (KIRDI) • KIRDI is a parastatal established under the Science and Technology Act, Cap 250, 1979 of the laws of Kenya. • Its mandate is to undertake research and development in industrial and allied technologies. • Among its institutional objective is to contribute to the creation of national wealth through development of technologies that are appropriate and accessible to micro and small enterprises in Kenya

KIRDI’s has been instrumental in : • Development/reverse engineering of agro-processing machinery and equipment and disseminating the same to small and medium scale food processors in accordance with vision 2030. Examples of equipment already developed and being piloted by KIRDI include: Fruit pulper, Pasteurizer, Blender and Electric drier • Process and product development • Establishment of pilot plants • Training, capacity building and consultancy services • Business incubation service

KIRDI Roles with VIP Ampath To develop and provide micro-processing equipment directly to the SMES or via existing supermarket chains Training and capacity development of SMEs. Future promotion of the business models NB: KIRDI has well established to undertake the above roles now and in future. Ampath is set to initiate dialogue with KIRDI

Ampath is working with Equity Bank to develop model financial products for its clients • Existing Equity financial products include Fanikisha Imara and Fanikisha Shaba. Aspects that will need to be reviewed are: • Interest rates and transaction fees • Collateral types • Repayment and grace periods • Disbursement/maturity periods • Target clients • Ampath will facilitate business linkages:-Equity-KIRDI -Supermarkets PILOT PHASE: Developing the Service

PILOT PHASE: Stimulating Demand Demand for services during the pilot will be stimulated as follows: • Direct intervention by VIP partners: • FPI/ AMPATH will document the business models • EPC will disseminate the models in workshops, seminars, trade shows and media • Fintrac will establish market linkages:- microprocessors/vendors – MFIs - Technology developers – Distributors • Service providers (MFIs, Technology developers and distributors) marketing own services

PILOT PHASE: Stimulating Demand • VIP will support technology provider, distributors and MFI to market the business models during the pilot stage. NB: KIRDI is already piloting micro processing technologies in some parts of Kenya. • During the piloting phase KIRDI will test the ability of microprocessors/vendors to pay for training. VIP Ampath will support KIRDI in this endeavor • KIRDI training package will include micro processing, entrepreneurship skills and credit management

PILOT PHASE: Target Outreach • Service Providers • Technology developer : 1 ( VIP will work with KIRDI which already involved in developing appropriate technology in micro-processing • Technology distributor: 5 supermarkets • MFI:-1 [Equity bank] • SEs (Microprocessors/vendors): 30 per pilot region x 5 regions = 150 • Pilot regions: Eldoret, Mosoriot, Chulaimbo, Kitale and Webuye

Determining Pilot Success Key determinants of pilot success will include: • Ability to graduate the very poor urban dwellers and vulnerable from dependency to self reliance • Potential for high adoption/market uptake

MARKET UPTAKE – Stimulating Demand • If the outcomes of the pilot tests on future training of microprocessors by KIRDI will be positive, VIP Ampath will conduct market research and/or stakeholder dialogue to develop detailed market uptake strategy. • VIP Ampath will strike a deal with KIRDI to continue providing the business development functions (Developing and providing value adding equipment to microprocessors and training them) on wide scale commercial basis) • VIP Ampath will document the business models for promotion by KIRDI

MARKET UPTAKE – Stimulating Demand Continued……… • VIP will/might provide initial subsidy to KIRDI to market the business development services to other microprocessors/vendors, banks and supermarkets through media campaigns, seminars and marketing materials • VIP will phase out any direct subsidies to enable the partner to operate commercially.

MARKET UPTAKE – Stimulating Demand Continued……….. 2. Ampath will facilitate microprocessors/Vendors to establish networks through which information/knowledge would be transferred. 3. The technology developer and distributors will market themselves to microprocessors/vendors 4. Ampath will collaborate with Equity bank, Government supported agencies and not-for profit organizations to spread awareness on the business models • For example :- KARI-Agriculture information Centre, Export Promotion Council, NGOs

MARKET UPTAKE – Target Outreach • High target outreach due to successful pilot and effective uptake strategies: • Micro-processors/vendors (including graduated Ampath clients = 100 per district x 14 districts = 1400 • Distributors = 2 per district x 8 districts = 80 • Employees = 500 • Sensitized community members = 1000 • TOTAL = 2,980 households equivalent to about 14,900 individuals

EXIT PHASE • Since the intervention will have been geared towards sustainably, the only remaining functions of VIP at exit will be: • Monitoring of market • Estimating the impact of the intervention • Evaluating the intervention to gather lessons learned relevant to the next program intervention.

INTERACTION WITH OTHER INTERVENTIONS • Successful financial service products will be dependent on microprocessors/vendors having adequate business management and technical skills in juice production and quality control. Hence…. * Quality control system, Technical and Business Training provider; and Tailored Financial Service products interventions will be delivered in parallel or as a package