Payouts from 401(k) Plans

200 likes | 344 Vues

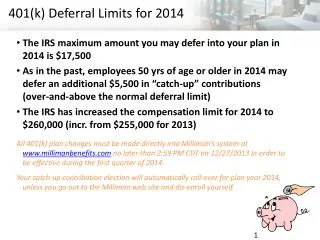

Payouts from 401(k) Plans. September 25, 2007. By the end of this lecture, you should be able to:. Explain payout options from 401(k) plans Discuss the importance of longevity risk in planning retirement withdrawals Explain how life annuities address this risk Why might they be valuable

Payouts from 401(k) Plans

E N D

Presentation Transcript

Payouts from 401(k) Plans September 25, 2007

By the end of this lecture, you should be able to: • Explain payout options from 401(k) plans • Discuss the importance of longevity risk in planning retirement withdrawals • Explain how life annuities address this risk • Why might they be valuable • Why might people not buy them

Accumulation: The “First Half” of 401(k) / Retirement Planning • How much money will individuals have at retirement? • Key issues: • Savings rates • Own contributions • Employer match • Investment choices • Administrative expenses

Payout: The “Second Half” of Retirement Planning • How do individuals convert their wealth into a sustainable stream of retirement income? • Key Issues: • Longevity risk • Inflation-protection • Spousal protection

Individuals are Living Longer • Life expectancy at birth in 1900 was only ___ years for men and ___ for women – it has increased approximately ___ years! • Today’s 65-year old man can expect to live to age ___ • Today’s 65-year old woman can expect to live to age ___

But Uncertainty Remains • Fraction of 65 year olds dying by age 70 Men ____ Women ____ • Fraction of 65 year olds living to age 90+ Men ____ Women ____

Payout Options • Lump sum distribution Rules • Systematic withdrawals • Life annuities/reversionary annuities • Note: All three are covered by minimum distribution requirements

Minimum Distribution Requirements • What is Congress’ objective? • Distributions must begin at retirement or April 1 of year after turn 70 (whichever is later) • Acceptable methods • Life annuities that are non-increasing (except for inflation protection) • Payments made based on (IRS) life expectancy • Anything faster is okay • Google: Minimum Distribution Tables • Problems with these rules?

Why Does Uncertainty about Length of Life Matter? • Retirement financial planning difficult • Trade-off two risks • Longevity Risk • The risk of outliving one’s resources • Under-Consumption Risk • The risk of dying with substantial wealth that could have been used to finance higher consumption levels while living

How Address this Risk? • Life Annuities • Trade a stock of wealth for an income stream that cannot be outlived • Solve the consumer’s retirement wealth allocation problem • Save early & Often: Rich Dad’s Cash Flow Quadrant

Annuity Provider’s Perspective • Companies can pool and share longevity risk across a large number of individuals • In the United States, the primary provider of annuities is the Social Security system, which pools longevity risk across nearly the entire population

Why Are Annuities Valuable? • Individual Perspective • Eliminates risk of outliving one’s resources • Provides higher level of sustainable income than is available without annuities • “Mortality Premium”: the insurer can pay a higher rate of return while living in exchange for loss of principal upon death

Example • 65 year old male in year 2000 • $100,000 of financial wealth • Interest rate = 6% • Inflation = 3% • Compare income from: • Inflation indexed annuity • Nominal annuity • Various “self-annuitization” strategies

What is the cost? • What do you give up when you annuitize???? • Compare & Contrast to an SPDA • Compare & Contrast to a Variable Annuity • www.immediate annuities.com • Tax implications of Annuities

Economic Theory • Economic “life-cycle” theory of savings and consumption indicate that annuities ought to be extremely valuable • Simulations indicate that the ability to access annuities is equivalent to a substantial increase in wealth

Few 401(k) Plans Offer Annuities • In late 1990s, only about ¼ of plans offered life annuities even smaller today • Why? • Demand side: workers do not ask for them • Supply side: some fiduciary responsibility for choice of insurer, OR, company carries the longevity risk itself (if set up as trust)

Consumer View of Annuities • Lack of consumer understanding • Individuals view annuities as a gamble – what if I die the next day? • They are used to insuring against “bad” events, and living a long time is “good” • Already annuitized by Social Security • Want liquidity for unexpected expenses • Want to leave money to kids • Other?

![[❤READ⚡ ✔DOWNLOAD⭐] 401(k) Fiduciary Solutions: Expert Guidance for 401(k) Plan](https://cdn7.slideserve.com/12679080/read-download-401-k-fiduciary-solutions-expert-dt.jpg)