Asset Classes

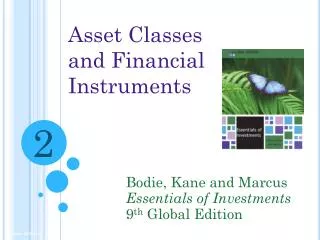

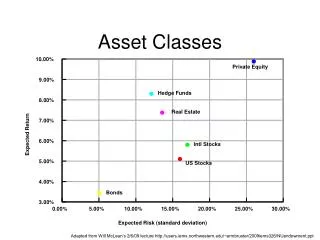

This analysis reviews the expected returns and risk associated with various asset classes, including Private Equity, Hedge Funds, Real Estate, International Stocks, US Stocks, and Bonds. By examining historical data and applying mathematical optimization techniques, we identify optimal portfolio allocations that maximize expected returns while maintaining an acceptable level of risk (standard deviation). The information is derived from Will McLean's lecture and aligns with modern portfolio theory, offering insights into effective investment strategies for better financial outcomes.

Asset Classes

E N D

Presentation Transcript

10.00% Private Equity 9.00% Hedge Funds 8.00% Real Estate 7.00% Expected Return 6.00% Intl Stocks 5.00% US Stocks 4.00% Bonds 3.00% 0.00% 5.00% 10.00% 15.00% 20.00% 25.00% 30.00% Expected Risk (standard deviation) Asset Classes Adapted from Will McLean’s 2/6/09 lecture http://users.iems.northwestern.edu/~armbruster/2009iems326/NUendowment.ppt

Math • ri = expected return of asset class i • C(i,j) = matrix of covariances • xi = % allocation to asset class i • Expected return = xTr • Variance of return = xT C x

Optimization maxx expected return s.t. standard deviation <= 10% maxx xTr s.t. xTCx <= (10%)2 1Tx = 1