Download

1 / 11

110 likes | 413 Vues

Cash Control. Unit 25. Internal Accounting Control. Internal Accounting Control for a business refers to the method and procedures used to: Protect the assets from waste, loss, theft, and fraud Ensure reliable accounting records

E N D

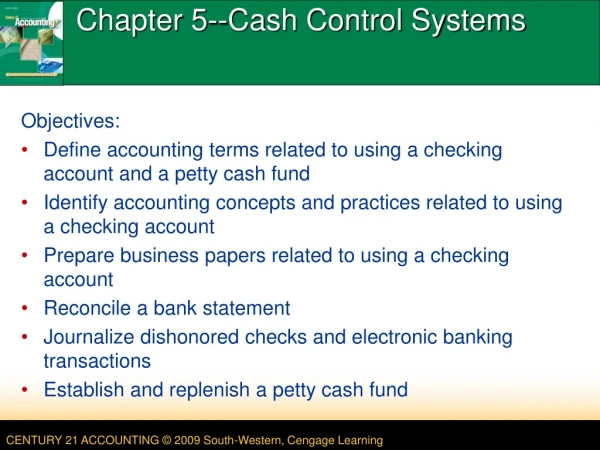

Cash Control Unit 25

Internal Accounting Control • Internal Accounting Control for a business refers to the method and procedures used to: • Protect the assets from waste, loss, theft, and fraud • Ensure reliable accounting records • Ensure accurate and consistent application of the firm’s policies • Evaluate the performance of departments and personnel

Cash Control Procedures • P 1: Separation of Duties • P 2: Immediate Listing of Cash Receipts • P 3: Daily Cash Proof • P 4: Daily Deposit of Cash • P 5: Payment by Cheque • P 6: Periodic Audit • P 7: Monthly Bank Reconciliation

Separation of Duties • Different people should carry out the task of recording cash received and the task of actually handling the cash. • This minimizes the chance of theft.

Immediate Listing of Cash Receipts • All cash should be recorded as soon as it is received. • In a sales setting, the cash register is often the first record of a cash sale. • At the end of the day, the register “tape” is compared to the cash receipts by the manager. • The customer helps prevent sales from being recorded at a lower amount and the sales person pocketing the difference by checking their receipt.

Prenumbered sales slips (source documents from unit 8!!) • Numbering of documents is used to prevent errors and losses due to theft of to the use of false documents • If a mistake is made and a prenumbered document must be voided, the document is marked void and kept with the other documents. This ensures that every document is accounted for.

Cash Received by Mail • The person who opens the mail should prepare a list of the cheques received. • A copy of this list is forwarded to the person responsible. • A second copy is sent to the accounting department. • Sometimes a third copy is kept on file for the future reference of the mail opener.

Daily Cash Proof • A NEW ACCOUNT (for the journal/ledger): • CASH SHORT AND OVER account is used to record shortages and overages of cash. • See p. 533 for examples of the daily cash proof • For those of you who have experience in retail, the daily cash proof is often located on the deposit envelope that goes to the bank. • The daily cash proof is the source document for the journal entry. • Cash shorts are recorded in the debit column (a decrease in owner’s equity). Cash overs are recorded in credit (an increase in owner’s equity).

Daily Deposit of Cash • Every day the cash receipts of a business (cash sales and cheques received) should be deposited in the bank. • NO large amounts of money left on the premises. • Amount of the deposit will be the same as the amount recorded in the cash receipts journal.

Payment by Cheque • All cash payment should be made by cheque. • Cheques are prenumbered and spoiled cheques are marked void. • Each cheque written should be accompanied by an invoice of voucher to provide verification that the payment is being made legitimately.

Petty Cash Procedures • When making a small purchase for a business, sometimes the petty cash is used instead of a prenumbered cheque. • Petty cash is a small amount of cash kept on-hand for a business to use. • An account must be created in the journal and the ledger called “Petty Cash”. • Petty cash vouchers must be filled out when petty cash is used. • Specific guidelines must be followed to replenish or change the amount of the petty cash account.